Definition and Meaning

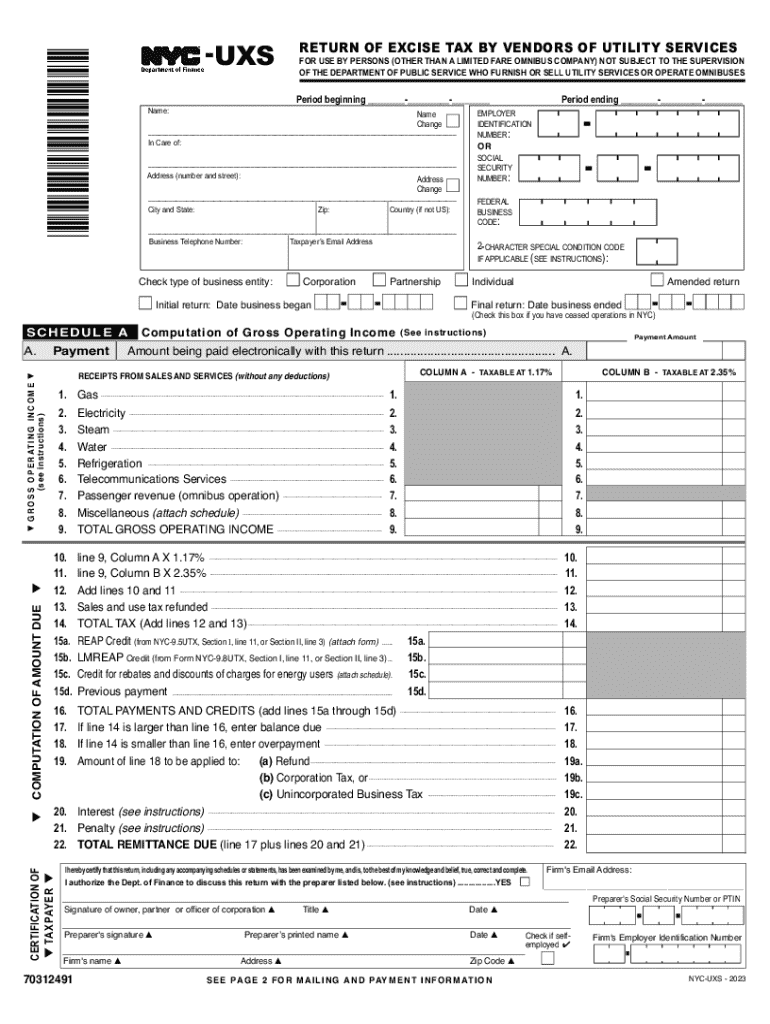

The "-UXRB RETURN OF EXCISE TAX BY UTILITIES * 7 0 2 1 1 6" is a specialized tax return form used by vendors of utility services in New York City (NYC). It is primarily designed to report and pay excise taxes levied on the gross operating income generated from various utility services, including gas, electricity, steam, water, and telecommunications. This form captures essential taxpayer information, calculates tax liabilities, and identifies applicable penalties for late submissions or payments.

Key Elements of the Form

Several critical components make up the UXRB form:

- Taxpayer Information Section: This part requires detailed information about the vendor, including business name, address, and taxpayer identification number (TIN).

- Income Reporting: Vendors must report gross operating income derived from utility services.

- Tax Computation: This section involves calculating the excise tax owed based on reported income, considering permitted deductions where applicable.

- Payment Instructions: Clear guidelines on how to file payments, whether online or via mail.

- Late Filing Penalties: Outlines financial penalties or interest charges applicable for delayed submission or payment.

How to Use the UXRB Form

Utilizing the UXRB form involves understanding its purpose and appropriate completion:

- Gather Required Documentation: Collect all relevant financial records, including gross income details and any supporting documentation for deductions.

- Complete Each Section Accurately: Ensure all sections, from taxpayer information to tax computation, are filled out correctly.

- Verify Calculations: Double-check all entered figures for accuracy, especially tax computations.

- Submission: Follow the guidelines for submitting the completed form within the stated deadlines to avoid penalties.

IRS Guidelines and Compliance

The UXRB form adheres to specific IRS guidelines for the remittance of excise taxes. Vendors must comply with federal mandates regarding the accurate declaration of utility-generated income and subsequent tax payments. Failure to align with these guidelines can result in audits or fines. It's also notable that this form needs to be in congruence with both IRS standards and local NYC tax regulations for complete compliance.

Filing Deadlines and Important Dates

Precise timing is crucial when dealing with the UXRB form:

- Quarterly Filing: Vendors typically need to file quarterly reports, aligning with the standard fiscal quarters.

- Specific Deadlines: Filing deadlines are often set within a month following each fiscal quarter's end, generally by the last working day of the subsequent month.

- Extensions: While rare in cases of excise taxes, extensions can sometimes be requested but require formal approval before the original due date.

Steps to Complete the UXRB Form

Completing the UXRB form involves methodical adherence to each step:

- Review Guidelines: Thoroughly read the accompanying instructions to understand each section’s requirements.

- Input Accurate Information: Carefully enter all business and income data, ensuring correctness.

- Calculate Tax Owed: Using the provided formulas or tax tables, compute the exact tax amount payable.

- Finalize Payment Details: Prepare payment instructions as outlined, whether for checks, online transfers, or other allowed methods.

- Check for Errors: Validate all entries to prevent inaccuracies.

- File and Follow Up: Submit the form within the deadline and retain proof of submission for records.

Who Typically Uses the UXRB Form

The UXRB form is intended for NYC-based utility service vendors, including:

- Electricity Providers: Companies supplying electrical services within New York's jurisdiction.

- Gas Suppliers: Those involved in the distribution and sale of natural gas services.

- Water Utilities and Telecommunications: Entities offering water supply and telecommunications services.

Penalties for Non-Compliance

Non-compliance concerning the UXRB form can attract several repercussions:

- Monetary Penalties: Late filing or underpayment might lead to fines proportional to the overdue amount and period of delay.

- Interest Charges: Accumulated daily interest might be enforced on outstanding tax amounts.

- Legal Actions: Continued non-compliance might trigger legal reviews or additional IRS scrutiny.

Software Compatibility

For those preferring digital management, the UXRB form is compatible with major tax preparation and accounting software like QuickBooks and TurboTax. These platforms support electronic filing and often include in-built prompts to mitigate errors during form completion.

By ensuring a comprehensive understanding of the UXRB form’s requirements and diligent adherence to the procedural steps outlined, vendors can effectively manage their excise tax obligations and avoid unnecessary penalties.