Definition and Meaning

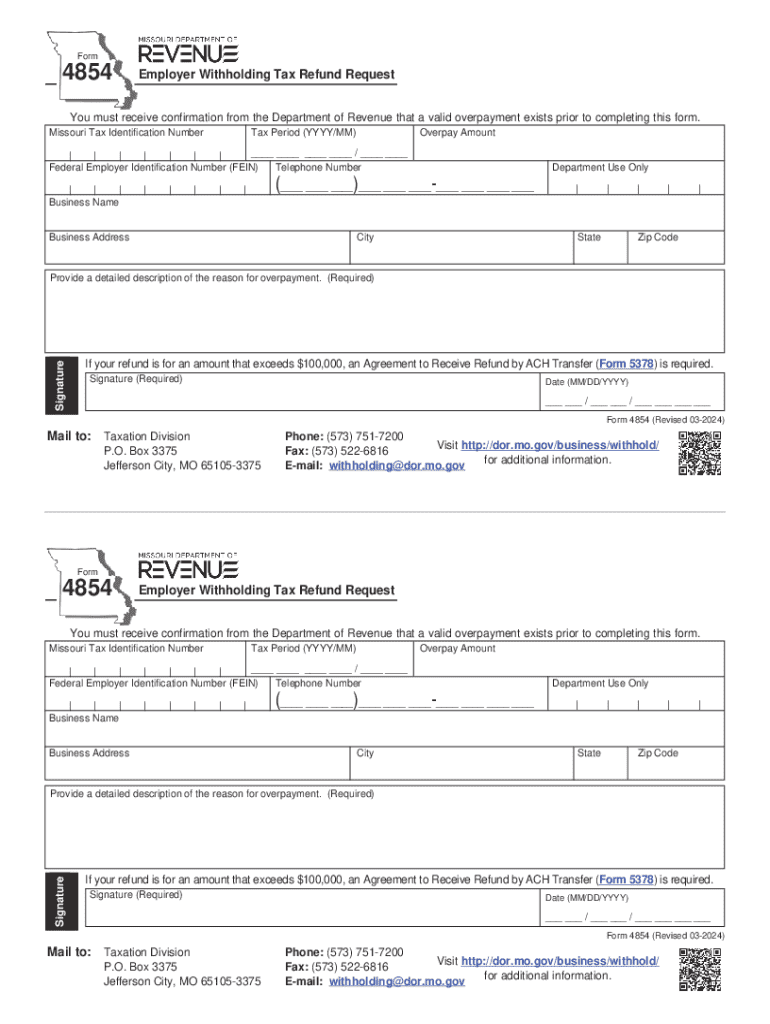

The Employer Withholding Tax Refund Request, identified in Missouri as Form 4854, serves as a formal application used by employers to reclaim overpaid withholding taxes. This refund process requires verification of a valid overpayment by the Department of Revenue, ensuring accuracy and compliance. Employers submit necessary financial details, including the Missouri Tax Identification Number and Federal Employer Identification Number (FEIN), to facilitate the processing of the refund. This form is a critical component for businesses aiming to correct overpayment discrepancies and manage their tax liabilities effectively.

Steps to Complete the Employer Withholding Tax Refund Request

-

Gather Required Information

Before filling out the form, collect all necessary data including the Missouri Tax ID, FEIN, and detailed business information. Prepare a concise explanation of the overpayment, supported by financial records. -

Complete the Basic Information Section

Enter your Missouri Tax ID number, FEIN, and business name as they appear in state records. Accuracy in this section is vital to avoid delays in processing. -

Detail the Overpayment

Clearly outline the reason for the overpayment and the exact amount. If the refund amount exceeds $100,000, you must complete an additional agreement form to accompany the request. -

Sign and Submit

Ensure that the form is signed by an authorized representative of the business. Unsigned forms may be rejected or returned. After signing, submit the form to the appropriate division, either via mail or electronically, as per state guidelines.

Required Documents

- Financial Statements: Provide records that corroborate the overpayment claim.

- Additional Agreement for Large Refunds: If your refund request exceeds $100,000, a supplementary agreement is required.

- Business Identification: Ensure the Missouri Tax ID and FEIN are included with the submission.

- Proof of Payment: Documentation validating the original tax submission prompts an audit trail for the Department’s verification.

Who Typically Uses the Employer Withholding Tax Refund Request

Primarily, Form 4854 is used by businesses that have inadvertently overpaid their withholding taxes to the state of Missouri. This can include a wide range of entities such as corporations, partnerships, and limited liability companies (LLCs). The form provides a method for these businesses to correct errors and recover funds, fostering effective financial management. State tax officers and accountants often assist in this process to ensure compliance with regulatory standards.

Legal Use and Compliance

Employers must adhere to specific legal protocols when pursuing a refund using Form 4854. Missouri law mandates that overpayments must be substantiated before any refund is issued. Misstating refund amounts can lead to audits or penalties, reinforcing the importance of accuracy and honesty in the application process. Additional agreements for significant refunds ensure that both the state and the business have documented understanding and legal backing for large transactions.

State-Specific Rules for the Employer Withholding Tax Refund Request

- Missouri Tax Code Compliance: All applications must align with Missouri's tax regulations. Amendments or recent legislative changes could impact eligibility and procedural requirements.

- Additional Forms for Large Refunds: For refunds above specific thresholds, additional verification documentation is necessary.

- Timely Submission: Ensure that the request is filed within the designated time frame to avoid rejection. Deadlines may vary based on legislative changes or fiscal policies.

Form Submission Methods

- Online Submission: Missouri provides a digital platform for submitting tax forms, streamlining the process and minimizing errors.

- Mail-in Option: Businesses can choose to mail completed forms. This traditional method requires planning for postal delivery times.

- In-Person Submissions: Though less common, some tax offices accept direct submissions for immediate processing.

IRS Guidelines and Interactions

While Form 4854 is specific to Missouri, businesses should maintain awareness of IRS guidelines affecting overall tax reporting. Federal and state tax obligations often intertwine, necessitating precise alignment in filings to prevent discrepancies. Employers should consult with a tax advisor to understand interactions between state refunds and federal obligations.

Penalties for Non-Compliance

Failing to file Form 4854 correctly or within the stipulated timeframe can result in penalties or interest charges on overpaid amounts still deemed payable. Non-compliance might also trigger audits, further emphasizing the need for detailed accuracy in submission. Documentation and reasonable cause assertions can mitigate penalties if errors are due to circumstances beyond control.