Definition and Purpose of Form M11H

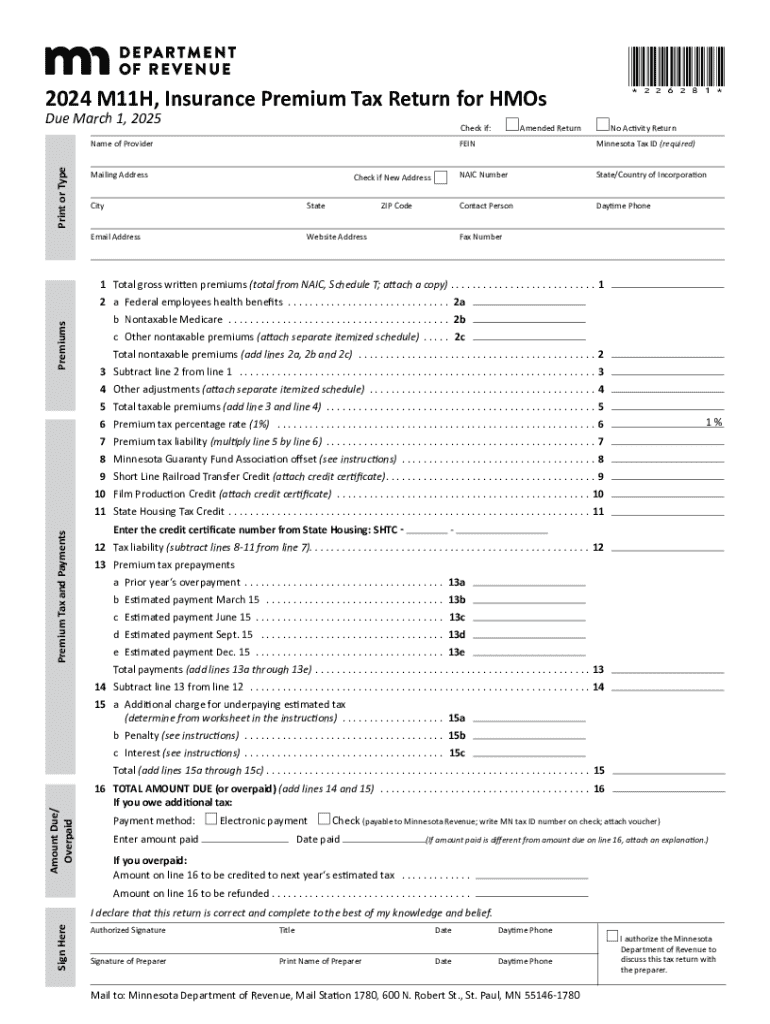

Form M11H, the Insurance Premium Tax Return for Health Maintenance Organizations (HMOs) in Minnesota, is a specialized tax document used by health care providers to report their insurance premium income. This form helps determine the taxable amounts, calculates tax liabilities, and provides mechanisms to adjust non-taxable premiums. By fulfilling these requirements, HMOs ensure compliance with Minnesota's tax regulations for health care entities. The form also includes sections for credits and estimated payments, offering a comprehensive view of a health provider's tax obligations.

Health Maintenance Organizations file this form annually to meet state taxation standards and avoid penalties. These organizations use Form M11H to outline their gross written premiums, providing a clear financial snapshot to the taxation authorities. This structured approach ensures a unified method for calculating and reporting taxes ensuring transparency between providers and the state tax authorities.

How to Obtain Form M11H

Form M11H is available through Minnesota's Department of Revenue. Organizations can visit the department's official website to download the latest version of the form. Alternatively, they may request a paper version by contacting the state's tax office directly. It's crucial for organizations to use the most current version of the form to avoid discrepancies or issues with submission.

Besides online resources, some tax preparation software programs include Form M11H, allowing health care providers to download the document directly through the application's interface. Tax professionals often find these software options helpful as they streamline access and ensure form compatibility while enhancing accuracy in reporting.

Steps to Complete Form M11H

Completing the Form M11H involves several key steps. Here is a detailed breakdown to guide health maintenance organizations through this process effectively:

-

Gather Financial Records: Collect detailed records of all health insurance premiums written during the tax year. This information is foundational for accurately reporting on the form.

-

Calculate Gross Written Premiums: List all premiums collected. These figures serve as the base figures from which taxes are calculated.

-

Determine Non-Taxable Amounts: Identify any premiums exempt from taxation, including those specified in state guidelines, and deduct these from the gross premiums to determine the taxable amount.

-

Apply Applicable Credits: Check for available credits that can offset the taxable amount as instructed on the form.

-

Calculate Total Tax Owed: Using the state's provided tax rate, calculate the total tax liability based on the taxable premiums.

-

Review and Validate: Double-check all entered information for accuracy. Discrepancies could lead to penalties or require a refiling of the document.

-

Submit the Form: Once complete, submit according to Minnesota guidelines, ensuring it is delivered before the March 1 deadline.

Key Elements of Form M11H

Several critical components make up Form M11H:

-

Gross Premium Reporting: The core of the form requires transparent disclosure of income from insurance premiums.

-

Non-Taxable Premiums Section: This provides organizations the space to report non-taxable income accurately.

-

Adjustments and Credits: This section allows health providers to reflect any eligible deductions accurately, ensuring that they are only taxed on what is required.

-

Estimated Payments: Organizations can record any pre-tax year payments made toward their tax liability.

-

Penalties and Interest Calculations: Provides a subsection to calculate any penalties accrued from late filings or payments, ensuring organizations understand their financial liabilities fully.

Filing Deadlines and Important Dates

The deadline for submitting Form M11H is March 1 of each year. This date provides the yearly cut-off for filing the previous year’s insurance premium income. Timely submissions are critical since missing this deadline could result in penalties or interest charges on outstanding taxes.

It's advisable to prepare all necessary documents well ahead of this deadline. Organizations should utilize this timeline to ensure adequate preparation and compliance. Tax preparation software often includes reminders, which can be configured to prompt as the deadline approaches, reducing the risk of late submission.

Important Terms Related to Form M11H

Understanding several key terms is essential when working with Form M11H:

-

Gross Written Premiums: This refers to the total revenue collected by HMOs from policyholders for insurance coverage within the tax year.

-

Non-Taxable Premiums: These are categories of premium income not subject to taxation, often defined by state regulations.

-

Tax Liability: This is the total amount owed in taxes by the organization after deductions and credits are applied.

-

Adjustments and Credits: These mechanisms can lower the overall tax liability when organizations meet specific criteria outlined by the state.

Penalties for Non-Compliance

Filing Form M11H on time is a legal requirement. Minnesota imposes penalties for late submission or non-compliance. These penalties may include monetary fines or accruing interest on unpaid taxes. It’s vital for health maintenance organizations to understand these implications to prevent financial loss.

Organizations that fail to submit by the March 1 deadline or omit information essential to accurate tax reporting may face audit risks. Maintaining compliance not only helps avoid penalties but also ensures that the organization retains a good standing with state authorities.

Submission Methods for Form M11H: Online and Mail

There are two primary methods for submitting Form M11H:

-

Online Submission: Use Minnesota's online portal for a swift and traceable filing method. This approach typically provides immediate confirmation of receipt.

-

Mail Submission: Organizations may also opt to send a paper version by post. For this method, using certified mail or other trackable options is beneficial to ensure the form reaches its destination.

While both methods are available, online submissions offer a faster processing time and a reduced risk of lost documentation. This efficiency makes digital submissions preferable for many organizations.