Definition & Meaning

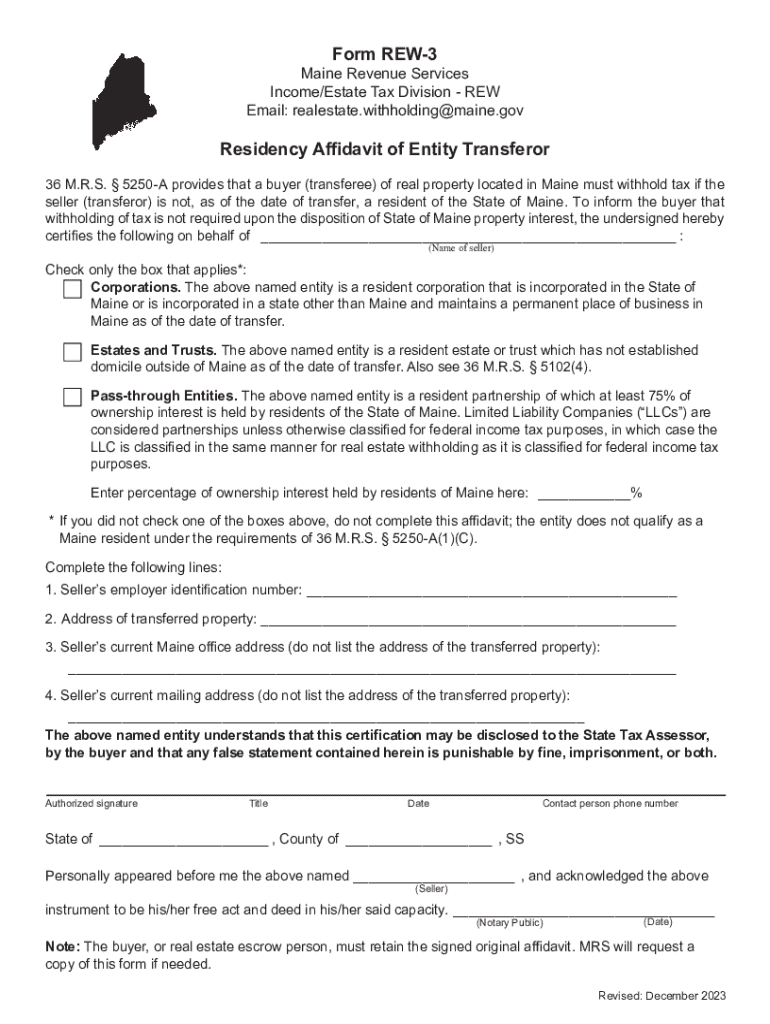

The statement "seller (transferor) is not, as of the date of transfer, a resident of the State of Maine" pertains to a legal stipulation within a Residency Affidavit. This document is typically used in real estate transactions to clarify the residency status of the seller at the time the property is transferred. In this context, "resident" generally refers to an individual or an entity that has a tax obligation within the state of Maine due to prolonged living or business operations.

Importance of This Statement

- Property Sales: This declaration usually influences tax withholding requirements during property sales.

- Tax Implications: Non-residency status may affect certain tax obligations, particularly with state income taxes and capital gains.

Residency Criteria

- Physical Presence: Whether the transferor physically resides in Maine.

- Intent: Transferor's intention to make Maine a permanent home.

- Duration: The length of time the seller spends in Maine yearly.

Steps to Complete the Affidavit

Filling out the Residency Affidavit is crucial for accurate transfer processing in real estate dealings. Here’s a guide through each step:

- Obtain the Form: Access the Residency Affidavit from Maine Revenue Services or the real estate agent managing the sale.

- Complete Personal Information: Enter details such as name, address, and identification number.

- Indicate Property Details: Provide an accurate description of the property being transferred, including its address.

- Declare Residency Status: Clearly check or affirm the non-residency status as of the transfer date.

- Sign the Affidavit: Both seller and buyer must sign to confirm the information is accurate and acknowledged.

- Retain Copies: Keep copies with both parties for potential future reference or audits.

Necessary Documentation

- Current ID or Proof of Address: To verify non-residency.

- Property Papers: Supporting documents regarding the property being transferred.

How to Use the Form

When engaging in a real estate transaction, knowing how and when to use this affidavit effectively safeguards against legal and financial complications. Here's how:

In Real Estate Transactions

- During Closing: Use the affidavit as part of the closing paperwork to certify residency status.

- For Tax Reporting: This form helps clarify tax scenarios for both the seller and the buyer, particularly in relation to Maine state taxes.

Edge Cases & Variations

- Multiple Owners: If there are multiple transferors, each must complete an affidavit.

- International Transferors: Special considerations are required if the seller is not a U.S. resident.

Who Typically Uses This Form

Predominantly used by:

- Property Sellers: Individuals or entities transferring property out of Maine.

- Real Estate Agents: To ensure compliance with regulatory requirements.

- Tax Professionals: For advising on tax implications tied to the transaction.

Various Business Entities

- Corporations: When selling commercial property.

- Trusts & Estates: During the transfer of property as part of an estate settlement.

Legal Use of the Non-Residency Declaration

The affidavit legally serves to inform and confirm tax responsibilities of non-resident sellers within Maine. Ensuring legal compliance is crucial for parties involved in property transfers, thereby preventing potential disputes or financial penalties later.

Legal Nuances

- Verification: Authorities may require additional verification to support the non-residency claim.

- Challenges: At times, residency arguments may arise requiring further examination or documentation.

Penalties for Non-Compliance

Failing to correctly complete this affidavit can lead to significant legal and financial consequences:

- Fines: Penalties may include fines for misinformation or failure to file.

- Legal Action: Non-compliance can expose parties to potential legal disputes.

- Delayed Processing: Incorrect information could result in delays in transfer completion.

State-Specific Rules

Although this form is specific to Maine, understanding the state's tax laws and guidelines is crucial for proper submission:

- Withholding Tax Rates: Maine may have specific percentages or regulations for non-residents.

- Exemptions: Certain exemptions may apply based on the nature of the sale or other stipulations.

Comparison with Other States

Understand that when selling properties in different states, such as New York or California, residency affidavits might have differing requirements.

Examples of Using the Form

For practical comprehension, consider these scenarios:

- John Smith, an out-of-state business owner, sells a Maine commercial property. He declares non-residency to apply different tax regulations applicable for non-residents.

- The Harris Family, residing in New Hampshire, sells a vacation home in Maine. By certifying their non-residency, they potentially manage distinct capital gains tax implications effectively.

Step-by-Step Case Study

- Fill Out Initial Details: Add seller and property information.

- Residency Confirmation: Affirm non-residency status with accompanying documents.

- Finalize Documents with Signatures: Ensure lawful validation by involved parties.

With these comprehensive steps and insights, this guide helps navigate the requirement that a seller (transferor) is not, as of the date of transfer, a resident of the State of Maine, ensuring an effective and compliant property transfer process.