Definition & Meaning

The "Estate Tax FAQMaine Revenue Services" refers to a comprehensive guide provided by the Maine Revenue Services that addresses frequently asked questions regarding estate tax within the state. It serves as an essential resource for individuals and entities involved in managing estates subject to Maine's estate tax laws. This guide is pivotal for understanding the unique requirements, processes, and implications surrounding estate taxation in Maine. As estate tax can significantly impact financial planning and estate management, this guide facilitates a clearer understanding of one's obligations and rights under Maine law.

How to Use the Estate Tax FAQMaine Revenue Services

This FAQ guide is designed to be user-friendly, catering to a range of stakeholders from estate planners to individual taxpayers. To effectively use the guide:

-

Identify Relevant Sections: Start by focusing on sections that pertain directly to your concerns or questions. These might include filing procedures, requirements for exemptions, or payment protocols.

-

Follow Step-by-Step Instructions: The guide typically includes detailed steps for processes such as submitting estate tax returns or requesting exemptions. Follow these meticulously to ensure compliance.

-

Leverage Examples: Utilize any examples provided to contextualize information and illustrate how guidelines apply in real scenarios.

-

Consult Terms and Definitions: Familiarize yourself with any specific terms and legal jargon outlined in the FAQ to fully grasp the content.

Steps to Complete the Estate Tax FAQMaine Revenue Services

Ensuring accurate completion of estate tax documentation requires adherence to the following steps:

-

Gather Necessary Information: Collect all pertinent details regarding the estate, including valuations, debts, and ownership documentation.

-

Read the FAQ Thoroughly: Before filling out any forms, review the entire FAQ to understand the requirements and nuances involved.

-

Complete Required Forms: Fill out relevant estate tax forms as indicated by the guide, ensuring all information is accurate and up-to-date.

-

Seek Clarification When Needed: If any section is unclear, consider consulting a legal or tax professional for advice tailored to your situation.

-

Submit the Form: Follow submission instructions provided in the FAQ, which may include online submissions or mailing physical copies.

Why Should You Use the Estate Tax FAQMaine Revenue Services

Using this FAQ guide is beneficial for several reasons:

-

Compliance: Ensures adherence to Maine's estate tax laws, helping avoid penalties or unnecessary delays.

-

Clarity: Clarifies complex legal and tax concepts, making it easier to address estate tax responsibilities accurately.

-

Resourcefulness: Provides a centralized source for common inquiries, reducing the need to search through multiple documents or resources.

-

Efficiency: Streamlines the estate management process by offering clear instructions and step-by-step guidance.

Important Terms Related to Estate Tax FAQMaine Revenue Services

Understanding key terminology is essential for navigating the estate tax process:

-

Estate Tax: A tax levied on an estate based on the value of assets transferred upon death.

-

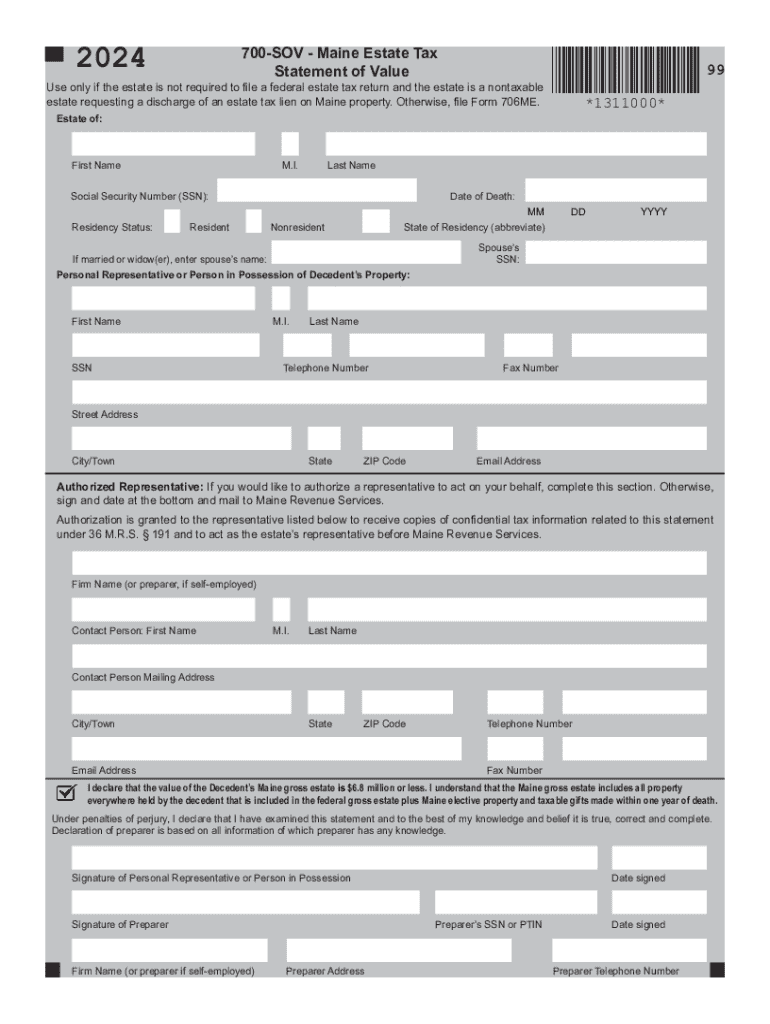

Nontaxable Estate: An estate valued below a certain threshold, exempt from federal estate tax requirements.

-

Discharge of Lien: Refers to releasing an estate's property from a tax lien, provided certain conditions are met.

-

Personal Representative: An individual appointed to administer the estate, often responsible for tax matters.

Filing Deadlines / Important Dates

Timeliness is crucial in estate tax matters:

-

Estate Tax Return Deadline: Generally due within nine months of the decedent's date of death, though extensions might be available.

-

Payment Due Date: Estate tax payments are typically required by the filing deadline to avoid interest and penalties.

-

Extensions: Requesting an extension does not delay tax payment due dates, only the filing deadline.

Required Documents

Several documents are typically necessary:

-

Death Certificate: Confirms the decedent and verifies the date of death.

-

Estate Valuation: Provides an appraisal or equivalent evidence of the estate's total value.

-

Tax Forms: Includes state-specific estate tax forms, like Form 706 for federal purposes and any Maine-specific variants.

Form Submission Methods (Online / Mail / In-Person)

Maine Revenue Services offer several submission methods:

-

Mail: Submissions via postal service should follow specific guidelines regarding addresses and required documentation.

-

Online Portal: Some documents can be submitted through the Maine Tax Portal, offering convenience and instant submission confirmation.

-

In-Person: Direct submission might be available for certain documents or if assistance from the revenue office is needed.

Digital vs. Paper Version

Choosing the appropriate format:

-

Digital Submission: Offers faster processing and confirmation, supported by secure online platforms.

-

Paper Submission: Required when specific original signatures or notarization is necessary, though it may involve longer processing times due to mailing.

Eligibility Criteria

Eligibility to file under Maine estate tax laws includes:

-

Value of Estate: Estates exceeding Maine’s exemption threshold may have tax liabilities.

-

Residency: The decedent must have been a resident of Maine, or the estate must contain real or tangible property located in Maine.

-

Federal Filing Requirement: Estates needing to file a federal return may also trigger state obligations.

By offering maximum content and adhering to the specific features unique to Maine's estate tax guidelines, this format ensures comprehensive coverage and usefulness for readers needing in-depth insights into the "Estate Tax FAQMaine Revenue Services."