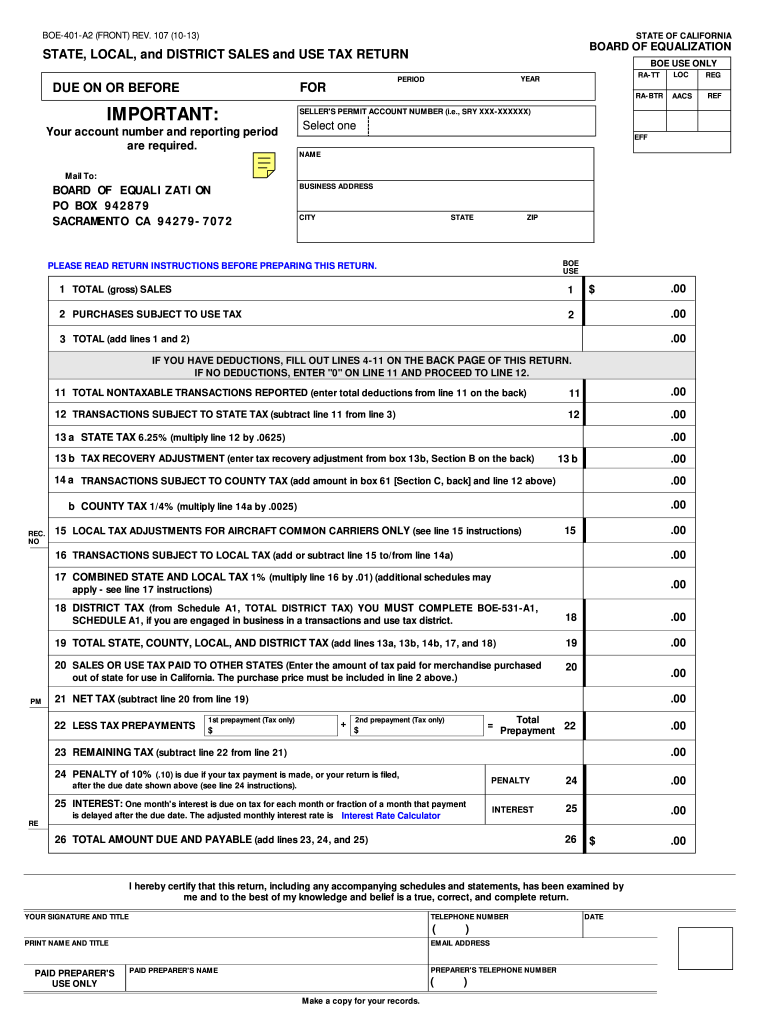

Understanding the California BOE-401-A2 2013 Sales Use Tax Return

The California BOE-401-A2 2013 Sales Use Tax Return is a vital document required for reporting sales and use taxes to the California State Board of Equalization (BOE). This form is designed to assist taxpayers in declaring total sales, detailing use tax liabilities, and calculating the amounts due based on applicable state, local, and district tax rates. Essential for businesses operating in California, this form ensures compliance with tax obligations and aids in the accurate filing of taxes.

How to Use the BOE-401-A2 2013 Form Efficiently

Filling out the BOE-401-A2 form correctly is crucial for accurate tax reporting. Here's a step-by-step guide:

-

Gather Information: Collect your total sales receipts, exempt sales documents, and any other supporting documents related to adjustments or deductions.

-

Enter Sales Data: Start with the total gross sales, then document any applicable deductions to reach the total amount subject to sales tax.

-

Calculate Use Tax: Report all purchases subject to use tax, which typically includes out-of-state, non-taxed purchases imported into California for use.

-

Determine Deductions: Carefully document all legally permissible deductions, such as sales for resale or non-taxable deliveries.

-

Finalize Calculations: Use the form to calculate the net taxes due, applying adjustments for prepayments or credits as needed.

-

Review Entries: Double-check all entries for accuracy to avoid errors or potential penalties.

Steps to Complete the California BOE-401-A2 2013 Form

Completing the BOE-401-A2 involves several detailed steps:

-

Download the Form: Obtain the latest version from the California Department of Tax and Fee Administration website or through authorized tax software.

-

Fill Out Personal and Business Information: This includes name, contact details, taxpayer account number, and reporting period.

-

Document Sales and Purchases: Enter total sales and purchases subject to use tax in the appropriate sections.

-

Include Exemptions and Deductions: Accurately note any deductions, including non-taxable sales, in the provided fields.

-

Calculate Tax: Follow the instructions to determine the amount of tax due, factoring in applicable rates for each jurisdiction.

-

Submit the Form: Use one of the approved submission methods, such as online, mail, or in-person delivery, to complete your filing.

Penalties for Non-Compliance

Failure to file or pay taxes using the BOE-401-A2 form can result in significant penalties:

- Late Filing/Payment Penalties: A percentage of the unpaid tax will accrue as a penalty for each month the return is late.

- Interest on Unpaid Tax: Interest is charged on unpaid balances from the original due date to the date of payment.

- Negligence or Fraud Penalties: Severe penalties apply for underreporting due to negligence or intent to defraud.

Who Issues the California BOE-401-A2 Form

The BOE-401-A2 form is issued by the California Department of Tax and Fee Administration (CDTFA). The department oversees tax collection, processing, and enforcement within California, ensuring compliance with applicable state and local tax laws.

Filing Methods for the BOE-401-A2

Businesses and individuals can file the BOE-401-A2 form through various methods:

-

Online Filing: The easiest and most efficient option, enabling real-time submissions and immediate confirmation.

-

Mail: Traditional mail submissions are still accepted, although they may take longer to process.

-

In-person: Some prefer to submit forms directly at a CDTFA field office for immediate assistance and verification.

Required Documents for Accurate Filing

To complete the BOE-401-A2 form accurately, gather the following:

-

Sales Records: Detailed records of all sales transactions within the reporting period.

-

Purchase Invoices: Documentation for all purchases, particularly those that were subject to use tax.

-

Resale Certificates: If applicable, to validate non-taxable sales.

-

Exemption Certificates: For reporting exempt sales or deductions.

Important Dates and Deadlines

Timely filing is critical. The BOE-401-A2 form must be submitted by the due date specified for each reporting period. Typically, quarterly filings are due by the last day of the month following the previous quarter, although specific deadlines can vary based on business activity and CDTFA requirements. Missing these deadlines can result in penalties and interest on unpaid taxes.

Key Elements of the Form

Key components of the BOE-401-A2 form include:

-

Total Sales and Use Tax Calculation: Details the process of aggregating all sales and purchases subject to use tax.

-

Adjustment Entries: Areas for entries related to prepayments or credits to appropriately adjust tax liability.

-

Signature and Declaration: Requires taxpayer affirmation of accuracy, reinforcing the legally binding nature of the submission.

Business Types that Benefit from Using the BOE-401-A2

The BOE-401-A2 form is crucial for:

- Retail Businesses: Regularly interacting with sales tax due to high transaction volumes.

- Manufacturers and Suppliers: Managing both sales and use tax obligations across jurisdictions.

- Service Providers: Those selling tangible goods alongside their services.

Using the BOE-401-A2 ensures these businesses correctly calculate and report their tax liabilities, maintaining compliance with state laws.