Definition & Meaning

The "Annualized Estimated Tax Worksheet - Oklahoma Digital Prairie" is a tool specifically designed for taxpayers with fluctuating income throughout the year. It helps Oklahoma residents calculate their estimated tax payments by accounting for adjusted gross income, deductions, and credits over defined time periods. This structured form allows for the allocation of income and deductions into different periods, effectively aiding in calculating the correct quarterly estimated tax payments and ensuring compliance with state tax laws.

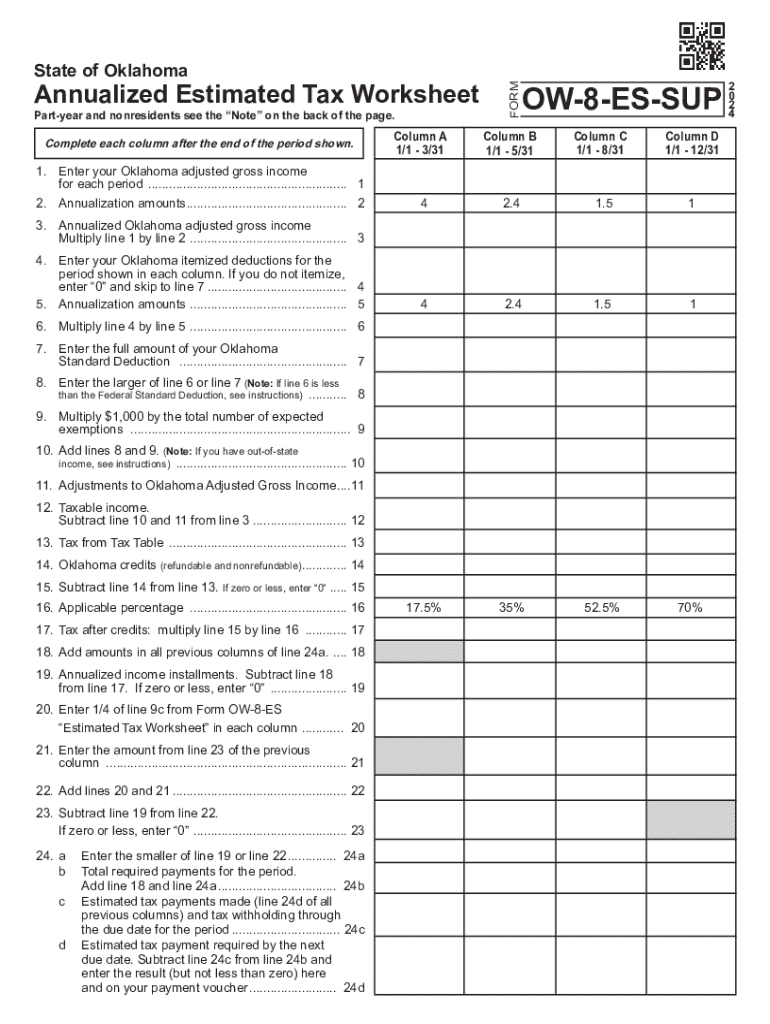

How to Use the Annualized Estimated Tax Worksheet

Using the Annualized Estimated Tax Worksheet involves a series of steps to accurately determine the individual’s tax liability. To begin, taxpayers should gather all relevant financial information, including income statements, deductions, and credits applicable for the tax year. The worksheet is completed by addressing each section, which typically includes:

- Income: Enter all sources of income received during each period.

- Deductions: List allowable deductions applicable to each income period.

- Tax Calculation: Use the instructions to determine the taxable income and apply the state tax rates to compute the estimated tax.

This process provides a clear view of the tax due for each period, preventing underpayment penalties.

Important Terms Related to the Worksheet

Understanding key terms is crucial for accurate completion of the worksheet. Some important terms include:

- Adjusted Gross Income (AGI): Total income minus specific deductions.

- Quarterly Periods: The year is divided into specific periods for tax purposes, often three months each.

- Estimated Tax Payment: Payments made periodically to cover expected tax liability.

- Withholding: Amount automatically deducted from wages or other income.

These terms ensure taxpayers understand which amounts to report and how they affect final tax calculations.

Steps to Complete the Worksheet

Completing the Annualized Estimated Tax Worksheet involves a precise sequence of actions:

- Review Instructions: Carefully read the worksheet instructions to understand the requirements for each section.

- Gather Documentation: Collect all necessary financial documents including W-2s, 1099s, and deduction records.

- Calculate Income for Each Period: Determine total income received, broken down by each specified period.

- Apply Deductions and Credits: Deduct eligible amounts from income for each period.

- Compute Tax Liability: Calculate the estimated tax based on taxable income for each period.

Accurately following these steps ensures that taxpayers meet their estimated tax obligations.

Filing Deadlines / Important Dates

Key deadlines for estimated tax payments must be adhered to avoid penalties. Generally, estimated tax payments are due quarterly:

- First Quarter: April 15

- Second Quarter: June 15

- Third Quarter: September 15

- Fourth Quarter: January 15 of the following year

Adhering to these dates is essential for avoiding interest and penalties from late payments.

IRS Guidelines and State-Specific Rules

Both the IRS and Oklahoma's state tax authority have guidelines for using the Annualized Estimated Tax Worksheet effectively. Federal regulations emphasize paying through a pay-as-you-go system, and state-specific rules may provide additional credits or deductions tailored for Oklahoma residents. Ensuring compliance with both sets of guidelines prevents underpayment and ensures that taxpayers are taking advantage of all available tax relief options.

Required Documents

To complete the worksheet effectively, several documents are necessary:

- Income Statements: Such as W-2, 1099 forms.

- Deduction Documentation: Proof for any claims of deductions.

- Previous Tax Returns: Useful for estimating current deductions and credits.

Maintaining a comprehensive record of these documents is vital for accurate reporting.

Penalties for Non-Compliance

Failure to properly fill out or submit the Annualized Estimated Tax Worksheet on time can result in penalties. The state may impose financial penalties for both underpayment and late payment. Interest charges can accrue from the due date of the taxpayer’s return, adding to the financial burden. Understanding these penalties underscores the importance of accurate and timely filing.