Definition and Meaning

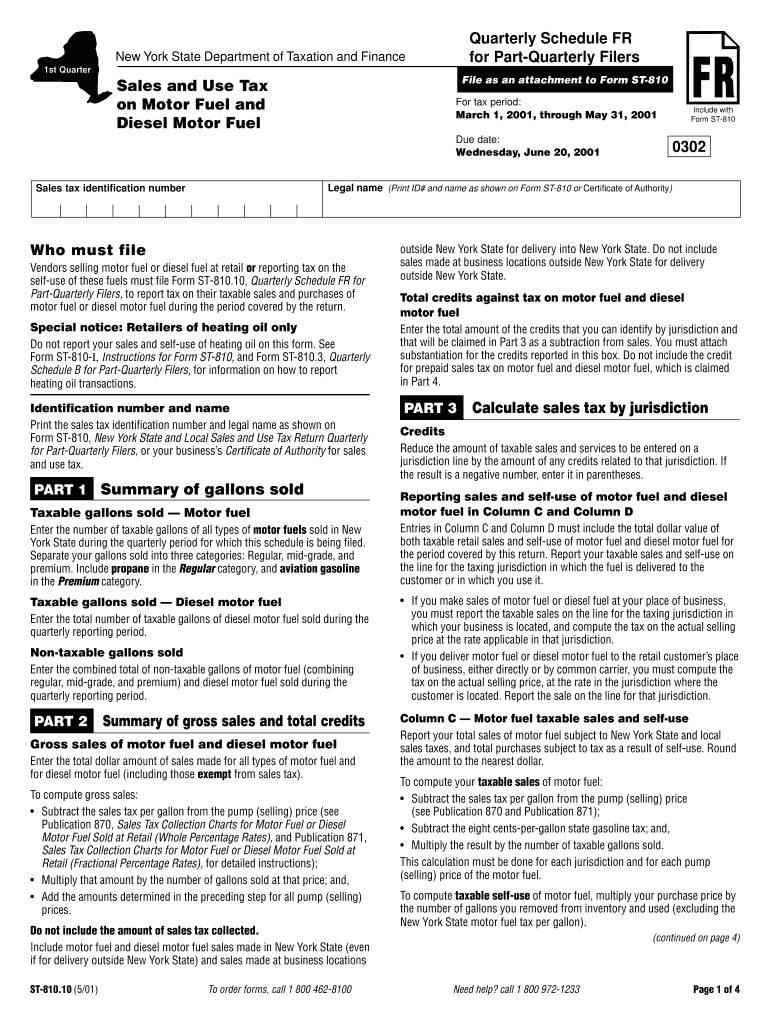

Form ST-810.10, titled "Sales and Use Tax on Motor Fuel and - tax ny," is an essential document used in New York State for tax reporting purposes. Specifically, it is used for reporting sales and use tax related to motor fuel and diesel fuel. The form is a critical tool for vendors within the state as it provides a structured way to calculate and report taxable sales and purchases of these fuels, ensuring compliance with the state's tax regulations.

Purpose of the Form

- Tax Reporting: It enables vendors to report their quarterly sales and use tax obligations accurately.

- Compliance: Helps businesses comply with New York State tax requirements for motor fuel sales.

Target Users

- Vendors dealing in motor and diesel fuel within New York State.

- Businesses required to file quarterly sales tax returns related to fuel.

How to Use Form ST-810.10

Using Form ST-810.10 requires a step-by-step approach to ensure accuracy and compliance. Vendors must follow the outlined steps to complete the form correctly.

Steps for Proper Usage

- Identify the Reporting Period: Determine the quarterly period for which you are reporting sales and use tax.

- Gather Required Data: Collect all necessary information about your motor fuel sales and purchases.

- Complete the Form: Fill in the required sections with accurate data, ensuring you calculate the tax correctly.

- Submit the Form: Submit the completed form by the due date to avoid penalties.

Practical Tips

- Ensure all data is up-to-date and includes corrections for any previous errors.

- Use official guidance from the New York State Department of Taxation and Finance for specific calculations.

Steps to Complete Form ST-810.10

Completing Form ST-810.10 involves several critical steps to ensure all relevant data is included. Here is a detailed breakdown of each step:

Step-by-Step Process

- Begin with Basic Information: Enter your business’s identifying information, such as the legal business name, address, and sales tax ID number.

- Detail Sales and Purchases: Report total quantities of motor fuel sold and purchased, categorized accordingly.

- Calculate Gross Sales: Use the form’s instructions to accurately determine the gross sales amount for the reporting period.

- Deduct Applicable Credits: Identify and apply any eligible credits that reduce the total taxable amount.

- Determine Tax Due: Calculate the total tax owed based on sales minus credits.

- Review and Double-Check Entries: Ensure all entered information is correct and consistent with your records.

Tips for Accurate Completion

- Keep detailed records of all sales and purchases to support the figures reported.

- Review previous submissions for consistency and correctness.

Key Elements of Form ST-810.10

Certain elements are crucial to accurately report and calculate sales and use tax on Form ST-810.10. Key components include:

Sections of the Form

- Business Information Section: Captures essential details about the vendor filing the form.

- Sales and Purchases Section: Detailed reporting of quantities of fuel sold and purchased.

- Tax Calculation Section: Outlines the steps for determining the final tax owed.

Important Fields

- Gross Sales: Total sales before deductions.

- Credits: Reductions applicable for previously paid taxes or other eligible credits.

- Net Tax Due: Total tax after applying any credits.

State-Specific Rules for Form ST-810.10

New York State has specific rules and guidelines that apply to the filing of Form ST-810.10. Understanding these regulations ensures compliance and avoids errors.

Key Regulations

- Quarterly Filing Requirement: The form is required to be filed each quarter by vendors registered in New York.

- Jurisdictional Reporting: Taxes must be reported according to the specific regions within New York where sales occurred.

- Exemptions and Deductions: Certain sales may be exempt or subject to deductions based on New York State laws.

Compliance Tips

- Regularly review updates from the New York State Department of Taxation and Finance.

- Engage with a tax professional if complex transactions or sales situations are involved.

Penalties for Non-Compliance

Failure to comply with the requirements for filing Form ST-810.10 can lead to severe consequences for vendors.

Common Penalties

- Late Filing Fees: Additional charges incurred for not submitting the form by the due date.

- Interest on Unpaid Taxes: Accumulating interest on any taxes not paid in a timely manner.

- Additional Fines: Penalties for incorrect reporting or neglecting to file the form altogether.

Preventative Measures

- Mark calendars with important filing dates and set reminders.

- Utilize automated systems where possible to track sales and calculate taxes accurately.

Digital vs. Paper Version

Vendors have the option to file Form ST-810.10 both in paper form and digitally. Each method has its advantages that cater to different business needs.

Digital Filing Benefits

- Efficiency: Faster processing and immediate confirmation of receipt.

- Accuracy: Automated calculations reduce chances of human error.

- Convenience: Ability to file from anywhere with internet access.

Paper Filing Benefits

- Traditional Approach: Some businesses may prefer the tangible nature of paper forms.

- Record Keeping: Physical copies can be easier to manage for businesses not yet equipped for digital filing.

Required Documents

To complete Form ST-810.10 accurately, specific documentation is necessary to support the numbers you report.

Essential Documents

- Sales Receipts: Detailed records of all sales during the reporting period.

- Purchase Invoices: Documentation of all fuel purchases to support claims on the form.

- Previous Filings: Copies of prior submissions may be needed for reference and consistency.

Maintaining Records

- Keep organized records of all financial documents related to motor fuel transactions.

- Regularly update records to reflect any changes or corrections.