Definition and Purpose of the 11 Monthly Schedule CT

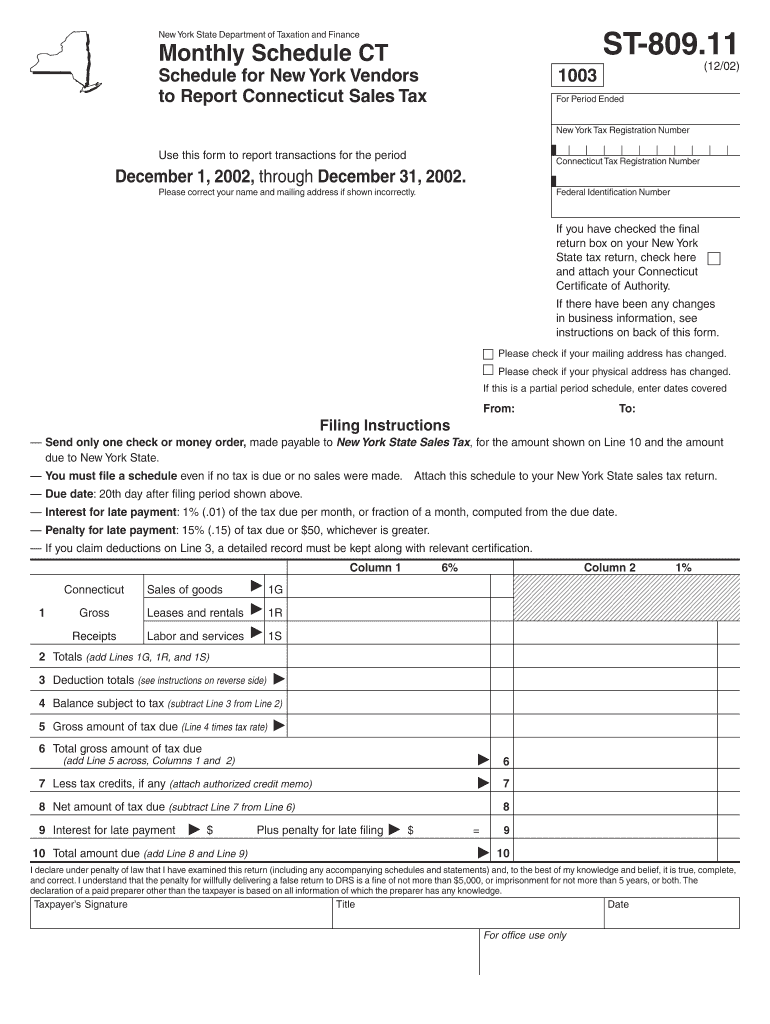

The 11 Monthly Schedule CT Schedule is a form used by New York vendors to report Connecticut sales tax, specifically for the period ending in December 2002. This document serves to detail sales transactions and applicable taxes that must be reported and remitted to Connecticut by vendors operating from New York. The schedule requires information on sales to consumers within Connecticut, including the amount of sales tax collected during the specified timeframe.

Key Elements of the Form

- Vendor Information: Includes the vendor's tax identification number, business name, and address.

- Sales Report: Details total sales amounts and sales tax collected.

- Exemptions and Deductions: Lists applicable exemptions that can reduce the tax liability.

- Signature: Requires a declaration signed by the vendor or authorized representative.

How to Use the 11 Monthly Schedule CT

Step-by-Step Completion

- Gather Required Information: Collect all sales records for the reporting period with amounts and corresponding tax.

- Fill Out Vendor Information: Complete sections with your business details and tax registration number.

- Report Sales Data: Enter total sales and taxable transactions.

- Calculate Tax Due: Use the form to determine the total tax amount owed after deductions.

- Review and Sign: Verify all information is complete and accurate, then sign the document.

Important Considerations

- Accuracy: Ensure figures reported are true to avoid penalties.

- Record Keeping: Maintain documentation supporting entries for auditing purposes.

Steps to Obtain the Form

Access Methods

- Online: Download the form from official tax agency websites.

- By Mail: Request a physical copy from the Connecticut Department of Revenue Services.

- Local Offices: Pick up at designated Department of Revenue locations.

Validation and Updates

Verify that you have the latest version of the form to ensure compliance with current regulations. Outdated forms may result in processing delays.

Submission and Compliance

Filing Deadlines and Methods

- Deadline: Typically due by the end of January following the reporting period.

- Submission Options:

- Online Filing: Submit electronically through authorized tax portals.

- Mail: Send completed forms to the designated tax office address.

- In-Person: Deliver directly to local Department of Revenue offices.

Penalties for Non-Compliance

Failure to file or late submission can result in penalties and interest charges. It is crucial to adhere to deadlines and verify all entries for completeness.

Who Issues the 11 Monthly Schedule CT

The form is issued by the New York State Department of Taxation and Finance. It facilitates report generation for cross-state sales tax purposes, ensuring taxes collected from Connecticut sales are accurately recorded and transmitted to the correct jurisdiction.

Form Variants and Alternatives

Historical and Related Versions

- Older Versions: Previous iterations may have different reporting requirements.

- Alternative Forms: Depending on business specifics, other tax forms may be necessary to fully comply with multi-state tax obligations. Ensure you are using the correct document for your situation.

Digital vs. Paper Versions

- Digital Advantages: Enables faster submission and reduces the risk of clerical errors.

- Paper Submissions: May require more time for delivery and processing but can be preferable for businesses lacking digital resources.

Important Terms Related to the 11 Monthly Schedule CT

- Sales Tax: A tax imposed on sales of goods and services, remitted to the state where the sale occurs.

- Tax Deductions: Allowable subtractions from total sales tax liability, often involving legally exempt transactions.

- Audit Trail: A comprehensive record of all transactions supporting the entries made on the form.

Applicable Business Types

Various businesses, especially those maintaining physical or economic presence in both New York and Connecticut, are required to file this form. It is particularly relevant to retailers, wholesalers, and distributors conducting cross-state transactions.

Eligibility Criteria

Businesses must adhere to Connecticut retail sales guidelines to determine requirement for filing this specific form. Seek clarification if operations span multiple jurisdictions to prevent administrative errors.