Definition & Overview of Tax Free Cash and Income - LV

The "Tax Free Cash and Income - LV" form pertains to the withdrawal of tax-free cash or income from an LV= Pension Plan. This document guides individuals through the process of accessing these funds legally and efficiently. Tax-free cash refers to the portion of a pension fund that can be withdrawn without incurring tax liabilities, typically up to 25% of the total pension pot. The form ensures that applicants understand their withdrawal options, potential tax implications, and have considered seeking financial advice.

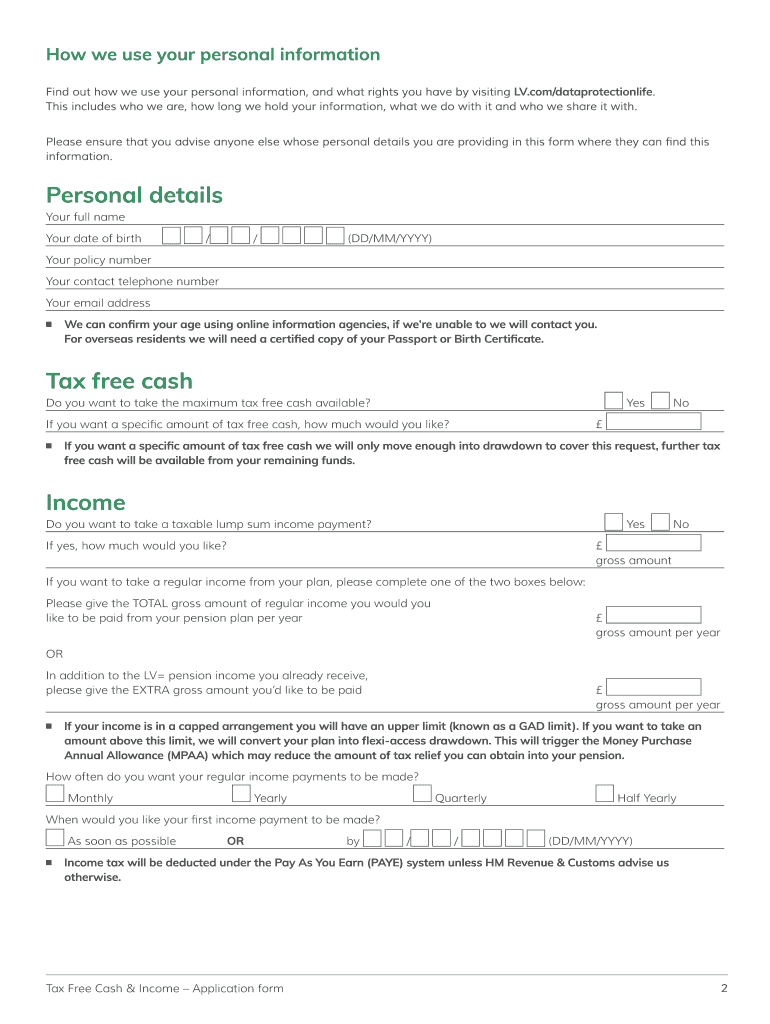

Key Components of the Form

- Personal Details: Captures essential information such as name, address, and pension plan details.

- Tax-Free Cash Request: Enables the applicant to specify the desired amount of tax-free cash.

- Income Request: Allows for the specification of income withdrawals in addition to tax-free cash.

- Payment Options: Details various methods for receiving the requested funds.

- Lifetime Allowance: Involves sections evaluating if withdrawals exceed the individual’s lifetime allowance.

How to Use the Tax Free Cash and Income - LV

Utilizing the form requires careful consideration of each section to ensure accurate and compliant submissions. Users should:

-

Gather Required Information:

- Personal identification and contact details.

- Specific pension plan information.

-

Complete Necessary Sections:

- Indicate desired tax-free cash amount and income.

- Select preferred payment methods.

-

Review and Acknowledge:

- Consider potential risks and implications.

- Confirm understanding of the importance of financial advice.

Practical Example

A 60-year-old retiree with an LV= Pension Plan wants to access a portion of their savings. They can use this form to withdraw 25% of their pension tax-free, ensuring compliance with financial regulations while continuing to draw regular income from the remaining pot.

Steps to Complete the Tax Free Cash and Income - LV

Filling out the "Tax Free Cash and Income - LV" form involves a systematic approach to ensure no details are overlooked.

-

Provide Personal Information:

- Fill in the name, address, and contact details.

-

Indicate Withdrawal Preferences:

- Specify amounts for tax-free cash and any additional income required.

-

Payment Method Selection:

- Choose how you wish to receive funds, such as direct bank transfers.

-

Confirm Financial Advice and Risks Consideration:

- Acknowledge that financial advice has been sought or bypassed at the applicant's discretion.

-

Sign the Declaration:

- Verify all information is correct and sign to complete the form submission.

Step-by-Step Guide

- Step 1: Gather your pension statements and personal details.

- Step 2: Calculate your desired tax-free cash amount.

- Step 3: Decide on income needs beyond tax-free limits.

- Step 4: Select safe and convenient payment methods.

Legal Use of the Tax Free Cash and Income - LV

The form's legal compliance is aligned with regulatory frameworks to ensure proper handling of pension plans.

Compliance Obligations

- Adheres to regulations concerning tax-free pension withdrawals.

- Requires acknowledgment of potential tax obligations and lifetime allowance implications.

Considerations for Legal Use

- Validity: Ensure that all information provided adheres to legal standards.

- Approval: Submissions must be reviewed and approved by relevant financial advisors to prevent non-compliance with tax laws.

Important Terms Related to Tax Free Cash and Income - LV

Understanding essential terminology is vital for correctly completing the form and grasping its implications.

Key Terms

- Tax-Free Cash: The portion of your pension you can withdraw without tax obligations.

- Lifetime Allowance: The cap on the amount of pension savings you can withdraw without incurring tax charges.

- Financial Advice: Guidance from a qualified financial planner or advisor regarding pension withdrawals.

IRS Guidelines on Pension Withdrawals

For U.S.-based individuals, adhering to IRS regulations is crucial when dealing with pension plans.

Relevant IRS Guidelines

- Tax Implications: Any income beyond the tax-free cash limit might be taxable.

- Documentation: Keep thorough records of all communications and submissions regarding your pension withdrawals.

Compliance Examples

- A retiree adhering to IRS withdrawal limits avoids unnecessary tax liabilities, ensuring compliance and fiscal prudence.

Penalties for Non-Compliance

Failing to comply with regulations surrounding the "Tax Free Cash and Income - LV" form can result in financial penalties.

Potential Penalties

- Exceeding Lifetime Allowance: Incurs tax charges on excess amounts.

- Inaccurate Information: Submitting incorrect information could result in fines or legal consequences.

Examples

- A non-compliant withdrawal leading to penalties, highlighting the importance of understanding withdrawal limits and legal obligations.

Required Documents

Proper documentation is crucial for a seamless pension withdrawal process.

Essential Documents

- Personal identification (e.g., driver's license, passport).

- Current pension statements and relevant financial documents.

Document Preparation

- Ensure all documents are up-to-date and accurate to prevent delays or legal issues.

These comprehensive guidelines are designed to assist applicants in properly navigating the complexities of accessing tax-free cash and income from their LV= Pension Plan, ensuring a secure and legally compliant withdrawal process.