Definition & Meaning

The income tax declaration form is a critical document used by employees and individuals in the United States to provide detailed information regarding their financial circumstances to accurately determine income tax obligations. This form aids in the reporting of various income sources, deductions, and tax liabilities for the fiscal year. Its primary purpose is to ensure accurate tax calculation and compliance with the Internal Revenue Service (IRS) regulations. By declaring relevant financial data, individuals can also potentially benefit from eligible deductions and exemptions, ultimately reducing their taxable income. Understanding the implications and requirements of the income tax declaration is essential for effective financial planning.

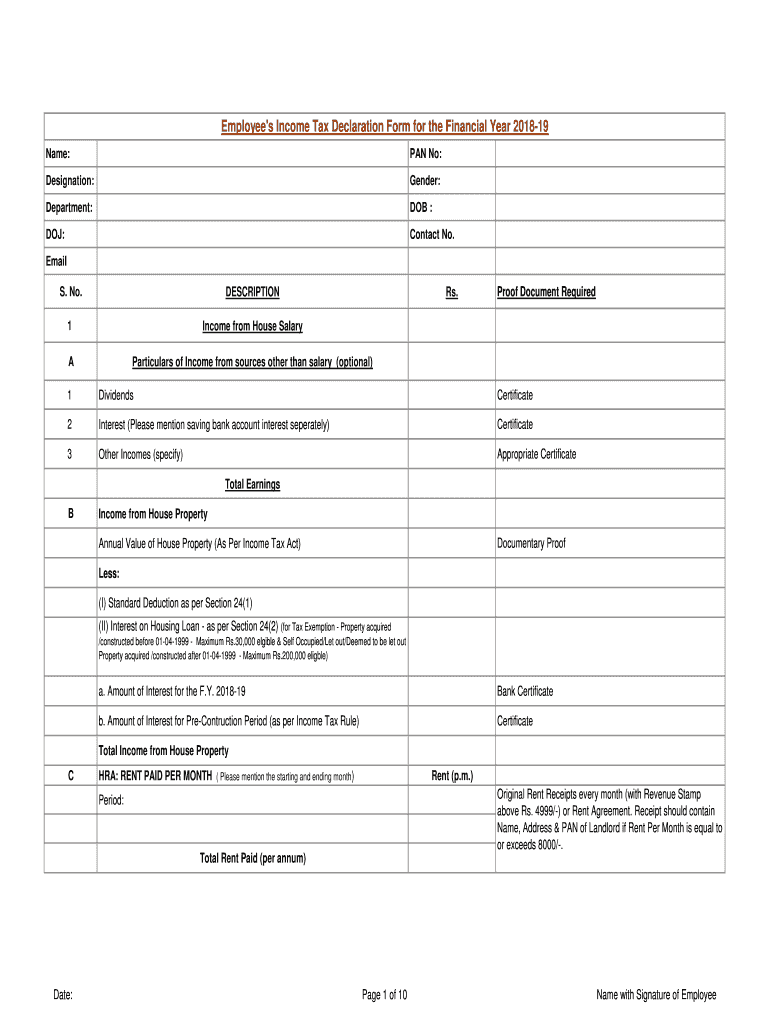

Key Elements of the Income Tax Declaration

The income tax declaration form consists of several essential components that must be filled out accurately:

- Personal Information: Includes name, address, Social Security number, and filing status.

- Income Sources: Detailed reporting of wages, salaries, interest, dividends, and other income forms.

- Deductions and Exemptions: Allows taxpayers to list qualified deductions under IRS rules, contributing to potential tax savings.

- Investment Information: Details about capital gains or losses, interests, and dividends from investments.

- Previous Employment Records: If applicable, details regarding earnings from prior employment during the tax year.

- Tax Credits: Information on eligible tax credits that may apply based on specific circumstances.

These elements ensure comprehensive reporting, facilitating the IRS's accurate assessment of tax liability.

How to Use the Income Tax Declaration

Using the income tax declaration form requires careful attention to detail:

- Gather Necessary Documents: Collect all financial records, such as W-2 forms, 1099 forms, and receipts for deductible expenses.

- Start with Personal Information: Accurately complete the personal details section to ensure the IRS can identify your tax records.

- List Income Sources: Include all forms of income, ensuring no sources are omitted to avoid future discrepancies.

- Demonstrate Deductions: Clearly outline all qualifying deductions, retaining proof of each claim for records and potential audits.

- Complete Investment sections: Ensure all investment-related earnings are accurately depicted.

- Review and Submit: Double-check the completed form for accuracy before submitting it to the IRS via your chosen method (online, mail, or in-person).

The accuracy of the information provided directly impacts your tax outcomes.

Steps to Complete the Income Tax Declaration

Completing the income tax declaration involves the following step-by-step procedure:

- Filing Status Selection: Determine your filing status (e.g., single, married, head of household) as it affects your tax bracket and deduction eligibility.

- Income Documentation: Source all relevant documents indicating earned and unearned income.

- Deduction Calculation: Identify standard and itemized deductions applicable to your situation.

- Credit Application: Determine which tax credits you qualify for based on your financial activities during the tax year.

- Proof of Payment: Include any records of tax prepayments, such as federal withholding amounts.

- Submission: Submit your completed form along with any payment due by the deadline.

Being methodical during this process ensures compliance and accuracy in your tax filing.

Important Terms Related to Income Tax Declaration

Understanding key terms associated with income tax declarations is crucial for navigating the form:

- Adjusted Gross Income (AGI): Your gross income minus specific adjustments, influencing your tax rate and deductions.

- Tax Bracket: The rate of income tax applied based on your income level.

- Exemptions: Specific allowances that reduce taxable income, such as dependent exemptions.

- Credits: Amounts that reduce your overall tax bill, applicable under certain eligibility criteria.

- Withholding: Amounts deducted from wages by an employer for prepayment of taxes.

Knowing these terms aids in accurately interpreting and completing your tax documents.

Who Typically Uses the Income Tax Declaration

The income tax declaration form is commonly utilized by:

- Employees: Required to declare their income and deductions to properly calculate tax liabilities.

- Self-Employed Individuals: Must report income from all business activities, including freelance and contract work.

- Investors: People with investment income to report dividends or interest.

- Retirees: Seniors receiving pension or retirement benefits may use the form for tax purposes.

- Homeowners and Landlords: Reporting earnings or losses related to real estate.

Each group has unique reporting requirements and possibilities for deductions and credits.

IRS Guidelines

Adhering to IRS guidelines when filling out the income tax declaration is paramount:

- Timely Filing: Submit your form by April 15th, unless an extension is granted.

- Accuracy: Complete the form accurately to avoid penalties for errors or omissions.

- Record-Keeping: Maintain copies of all submitted forms and documentation for at least three years.

- Audit Compliance: Be prepared to supply additional documentation if the IRS selects your return for audit.

Following these guidelines minimizes the risk of penalties and audit issues.

Filing Deadlines / Important Dates

Awareness of critical dates related to income tax declarations is essential:

- Filing Deadline: Generally April 15th of each year for the previous tax year.

- Extension Deadline: October 15th for those who have applied for a filing extension.

- Estimated Tax Payments: Quarterly payment dates throughout the tax year for self-employed individuals.

- Amendment Deadline: Up to three years from the original filing date for filing adjustments or amendments.

Respecting these dates ensures compliance and prevents unnecessary fines or interest charges.