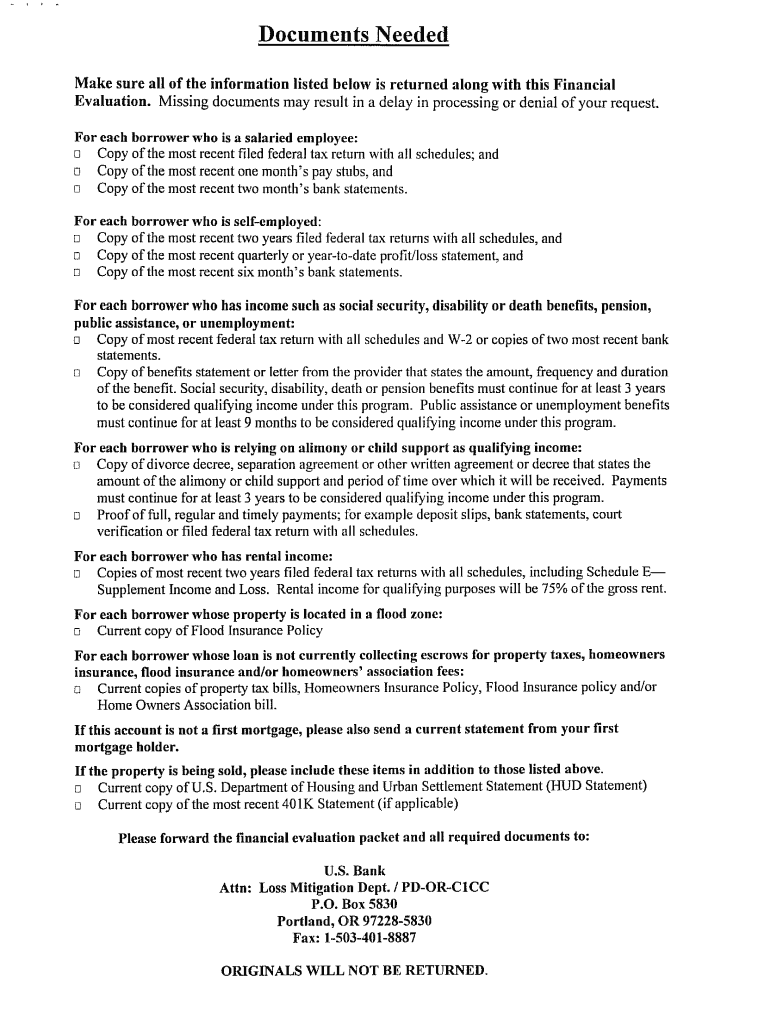

Understanding the U.S. Bank Short Sale Package

The U.S. Bank short sale package is a collection of documents required for homeowners to initiate a short sale on their property. It is particularly vital for individuals facing financial difficulties, as it allows them to sell their home for less than what they owe on their mortgage. This section will explore the essential components and steps involved in the short sale process.

Key Components of the Short Sale Package

A well-prepared short sale package is crucial for a successful transaction. Key components typically include:

- Hardship Letter: This document outlines the homeowner's current financial situation and the reasons for requesting a short sale. It should be concise yet detailed enough to convey the urgency and necessity of the sale.

- Financial Statement: A comprehensive financial statement gives lenders insight into the homeowner’s income and expenses. This document should specify all sources of income and detail monthly expenses to demonstrate the inability to keep the property.

- Bank Statements: The most recent two months of bank statements will be required, showing the homeowner's financial activity. This is used to verify the information provided in the financial statement.

- Listing Agreement: This agreement confirms that a real estate agent is helping in the sale of the property. It should detail the agreed sale price and the terms of the listing.

- Purchase Agreement: Once a buyer is identified, the purchase agreement is submitted, outlining the terms under which the buyer will purchase the home.

Steps to Complete the U.S. Bank Short Sale Application

- Prepare Documentation: Collect all necessary documents, including the hardship letter, financial statement, bank statements, and agreements.

- Submit the Application: Send the short sale package to U.S. Bank along with any required forms. Ensure that all documents are complete and accurately filled out to avoid delays.

- Communicate with Your Agent: Keep in contact with your real estate agent and U.S. Bank, informing them of any changes in your situation or new offers received.

- Await Bank Review: After submission, U.S. Bank will review the application. This process can take several weeks, during which additional information may be requested.

- Respond to Requests: Be prepared to provide any further documentation or clarification as requested by U.S. Bank to expedite the review process.

Eligibility Criteria for Short Sale Approval

Not all homeowners may qualify for a short sale. U.S. Bank typically requires that:

- You Experience Financial Hardship: Applicants must demonstrate a significant adverse financial condition, such as job loss, medical bills, or divorce.

- Property Value Declines: The home's market value must be less than the total remaining balance of the mortgage. This is validated through Comparative Market Analysis (CMA).

- Loan Type: Different types of loans may have specific requirements or exceptions, so it is essential to clarify the type of mortgage when applying.

Benefits of a Short Sale

Choosing a short sale over foreclosure can provide several advantages:

- Less Negative Impact on Credit Scores: A short sale may result in a less severe impact on credit scores compared to a foreclosure.

- Potential Debt Forgiveness: In some cases, lenders may forgive the remaining debt after the sale, relieving the homeowner of further financial burdens.

- Control Over the Sale: Homeowners retain some control over the sales process and can continue living in the home until the sale is finalized.

Common Challenges in the Short Sale Process

Navigating a short sale can be complex and may involve several challenges:

- Bank Approval Delays: U.S. Bank may take time to review the short sale package, causing frustration for sellers eager to close.

- Low Offers from Buyers: The bank often requires an appraisal for approval, which may not align with the homeowner’s expectations or offers received.

- Multiple Lender Situations: If there are multiple liens on the property, coordinating with all lenders can complicate the process, as each may need to agree before the short sale can proceed.

Gathering Documentation for Submission

When preparing a U.S. Bank short sale package, ensure all documents are current and well organized, as this speeds up the approval process. Here's a checklist to consider:

- Recent bank statements (two months)

- Completed hardship letter

- Complete financial statement detailing income and expenses

- Signed listing agreement with the real estate agent

- Purchase agreement from the potential buyer

Conclusion and Next Steps

Homeowners looking to engage in a short sale with U.S. Bank must be prepared with the necessary documentation and an understanding of the process. Navigating the complexities with an experienced real estate agent can greatly enhance the likelihood of a successful outcome. By understanding the components of the short sale package and meticulously preparing for submission, homeowners can effectively manage their financial recovery through this option.