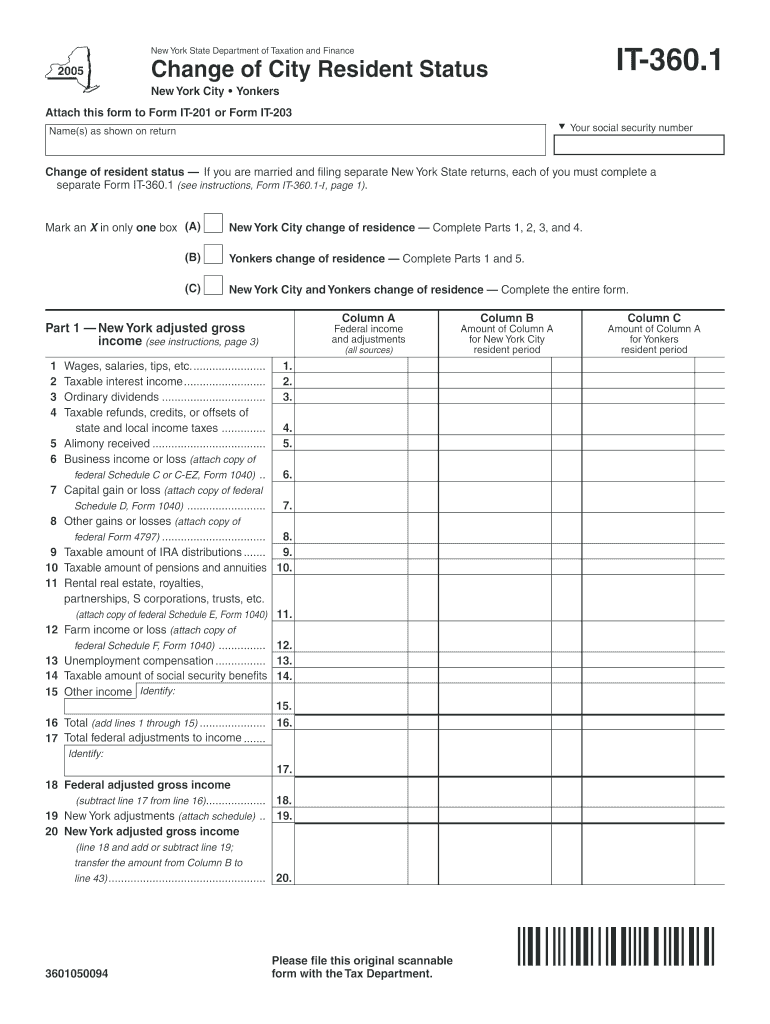

With DocHub, making adjustments to your documentation requires only a few simple clicks. Follow these quick steps to modify the PDF New York State Department of Taxation and Finance Change of City Resident Status New York City Yonke online for free:

Our editor is very easy to use and effective. Try it now!