Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out Can NY Residents Claim Tax Credits for Connecticut PET? with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the Can NY Residents Claim Tax Credits for Connecticut PET? in the editor.

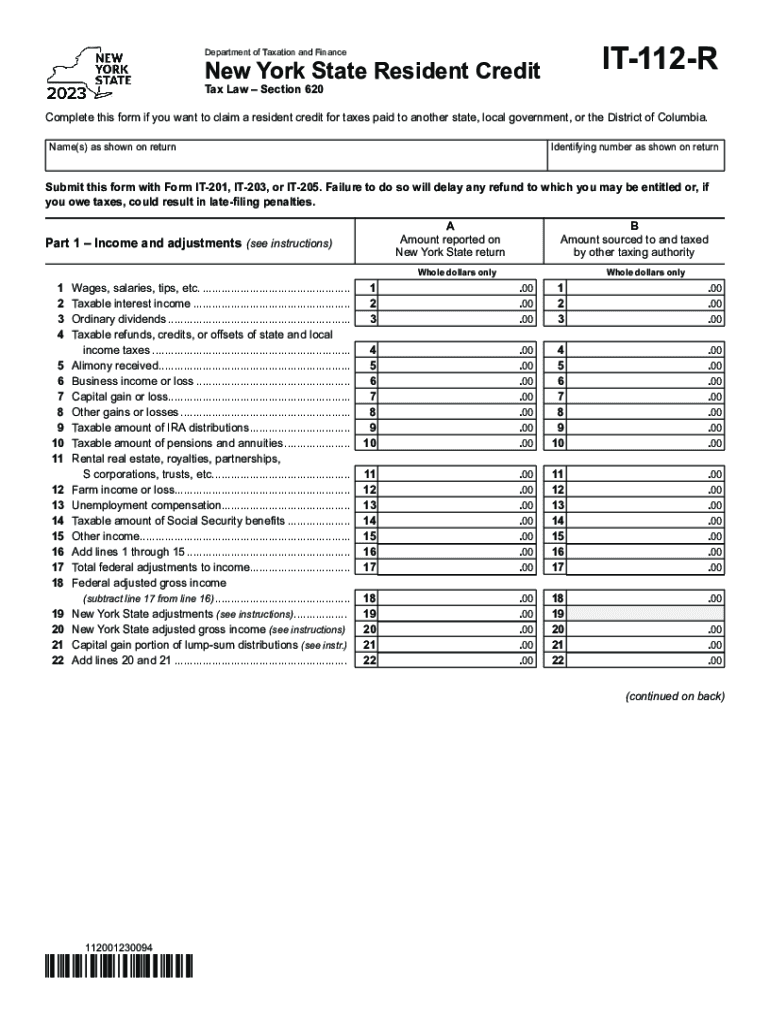

Begin by entering your name(s) and identifying number as shown on your tax return at the top of the form.

In Part 1, provide your income details. Fill in each line from wages to other income, ensuring you only enter whole dollars.

Proceed to Part 2 to compute your resident credit. Enter the two-letter abbreviation of the state where taxes were paid and the corresponding locality name if applicable.

Complete lines 24 through 30, detailing tax amounts imposed and calculating your credit based on instructions provided.

Finally, review Part 4 for any additional information required from your return filed with another state, ensuring all fields are accurately filled before submission.

Start using our platform today to fill out your tax forms online for free!

Fill out Can NY Residents Claim Tax Credits for Connecticut PET? online It's free

See more Can NY Residents Claim Tax Credits for Connecticut PET? versions

We've got more versions of the Can NY Residents Claim Tax Credits for Connecticut PET? form. Select the right Can NY Residents Claim Tax Credits for Connecticut PET? version from the list and start editing it straight away!

by DJ Hemel 2023 Cited by 5 PET promoters claim that the combi- nation of entity- level taxes and offsetting personal income tax benefits will allow passthrough owners to circumvent theRead more

The PE must first complete either federal Form 1065, U.S. Return of Partnership Income, or federal Form 1120S, U.S. Income Tax Return for an S Corporation.Read more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.