Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out 671 (Exemptions) with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the 671 (Exemptions) document in the editor.

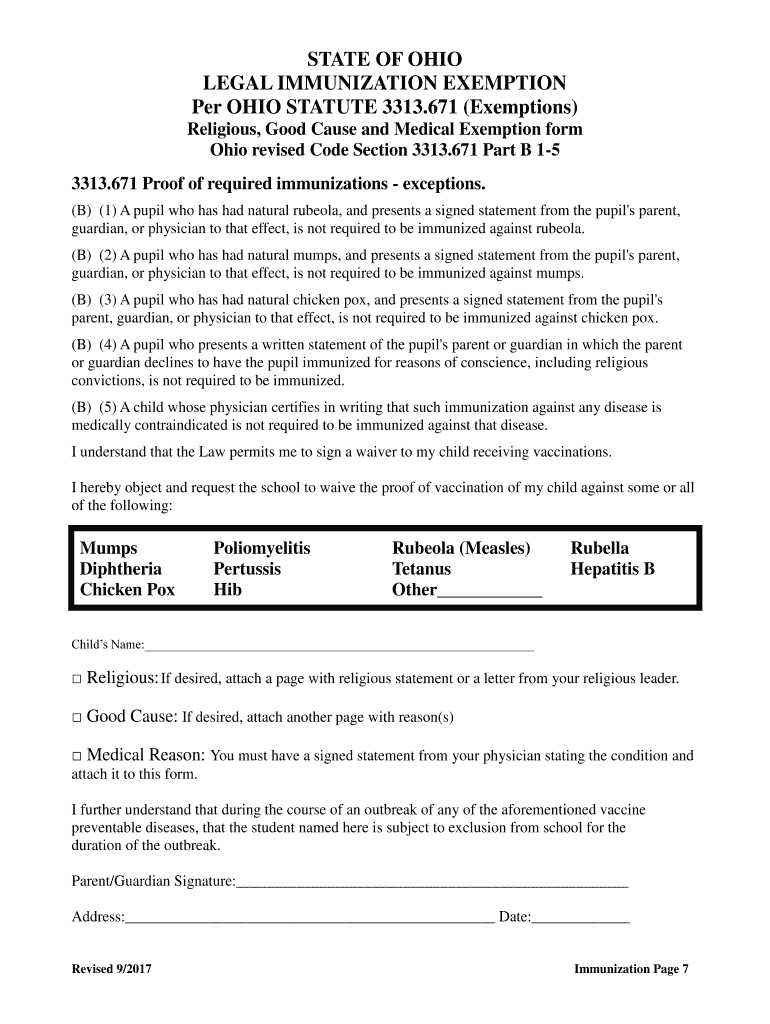

Begin by entering your child’s name in the designated field at the top of the form.

Select the applicable exemption type: Religious, Good Cause, or Medical. If you choose Religious, consider attaching a statement from your religious leader.

For Good Cause exemptions, provide a brief explanation in the space provided or attach an additional page if necessary.

If opting for a Medical exemption, ensure you have a signed statement from your physician detailing the medical condition and attach it to this form.

Indicate which vaccinations you are requesting an exemption for by checking the appropriate boxes listed on the form.

Finally, sign and date the form at the bottom as a parent or guardian before submitting it to your school.

Start using our platform today to easily complete and manage your forms online for free!

What is a $12,000 property tax exemptionFile Homestead exemption onlineWhat is homestead exemption texasHomestead exemption bexar county onlineHomestead exemption San AntonioWhen will my homestead exemption kick inHomestead exemption formHomestead exemption deadline 2026

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

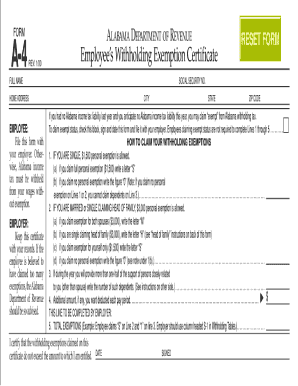

Form IT-2104-E Certificate of Exemption from Withholding

qualify for exemption from withholding of New York State income tax under Tax Law 671(a)(3) or under the SCRA. This certificate will expire on April 30, 2027.

A continuing writ of garnishment is similarly available to collect a debtors non-exempt wages, provided the debtor is not considered the head of household..Read more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.