Definition and Meaning of HMRC VAT 68

The HMRC VAT 68 form is an official document used in the process of transferring a Value Added Tax (VAT) registration number from a previous business owner to a new one when a business is sold or transferred as a going concern. This transfer ensures continuity in tax reporting and compliance with HMRC regulations. When using this form, both parties involved in the transfer must meet specific criteria set by HMRC to validate the change in ownership officially.

How to Obtain the HMRC VAT 68

To acquire the HMRC VAT 68 form, you can visit the official HMRC website, where it is available for download. This ensures you access the most up-to-date version of the form. It is also possible to request a copy directly from HMRC, either by phone or by mailing a written request to the appropriate department. Be sure to provide accurate business details when requesting to avoid any delays in receiving the form.

Steps to Complete the HMRC VAT 68

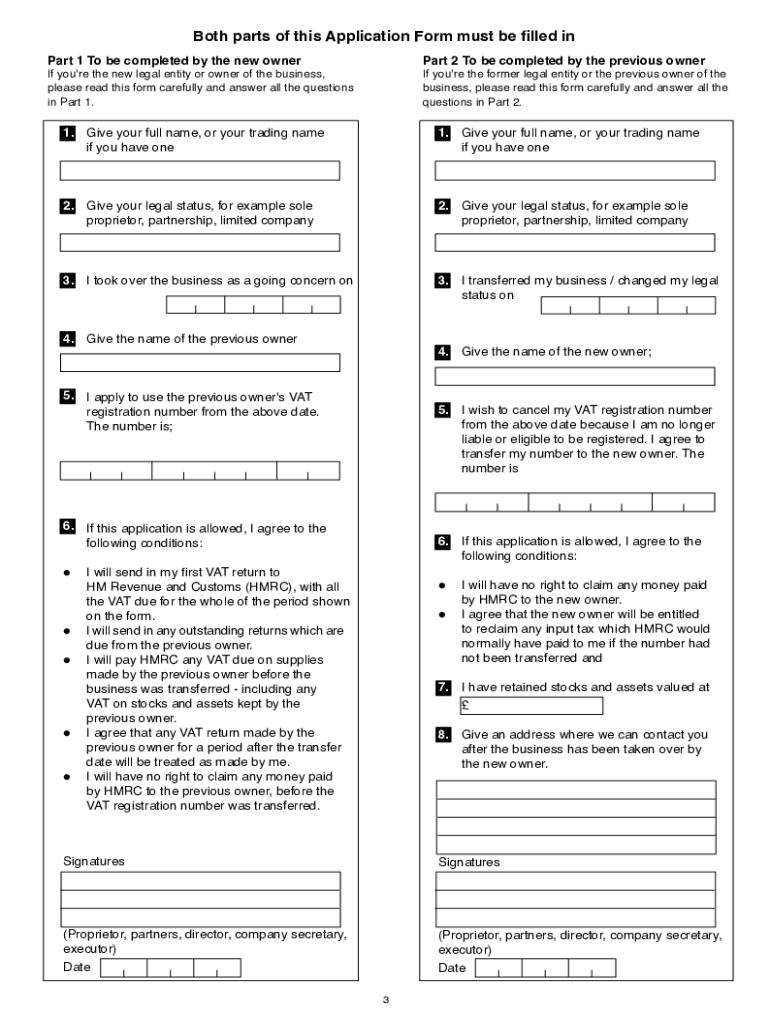

- Identification Information: Begin by entering the details of both the original and new business owners, including names, addresses, and contact information.

- VAT Details: Provide the VAT registration number to be transferred along with details about the effective date of the business transfer.

- Agreement Confirmation: Both parties must sign the form to confirm their agreement to the terms of the transfer.

- Submit the Form: Once completed, submit the form to HMRC for processing. This can be done through mail or electronically, depending on HMRC's submission preferences.

Key Elements of the HMRC VAT 68

- Ownership Details: Essential for identifying both the outgoing and incoming business owners.

- VAT Registration Number: The central focus of the form, indicating which number is to be transferred.

- Effective Date: The official date when the new ownership is acknowledged to take place.

- Signatures: Signatures from both parties involved in the transfer to validate the agreement.

Eligibility Criteria for Using the HMRC VAT 68

Eligibility to use the HMRC VAT 68 form hinges on certain business-specific conditions, such as the business being transferred as a going concern. This means the business must remain operational and meet HMRC's guidelines for such transfers. Both parties must possess a valid VAT registration, and the appropriate transfer agreement should be in place.

Legal Use of the HMRC VAT 68

The legal use of this form requires adherence to HMRC's guidelines, ensuring that all declarations, agreements, and submissions comply with the regulatory framework in place. Misuse or incorrect completion can lead to penalties or the rejection of the transfer application by HMRC. Thus, familiarity with VAT laws and accurate form completion is critical.

Required Documents for HMRC VAT 68 Submission

- Business Agreements: Relevant documentation showing legal transfer agreements between the old and new owner.

- Identification Proofs: Valid identification documents for both parties involved.

- VAT Registration Certificates: Proof of current VAT registration for both parties.

Ensure all supporting documents are accurate and complete to facilitate a smooth verification process by HMRC.

Penalties for Non-Compliance

Failure to comply with the requirements for submitting and completing the HMRC VAT 68 form may result in substantial penalties, including fines and potential audits by HMRC. It's crucial for businesses to adhere to all procedural and regulatory guidelines to avoid such repercussions. In addition, an invalid transfer can disrupt continuity in VAT processing, impacting the financial operations of the business.

These sections provide an in-depth understanding of the HMRC VAT 68 form, covering its definitions, acquisition methods, completion steps, and legal frameworks, ensuring comprehensive guidance for users involved in such business transfers.