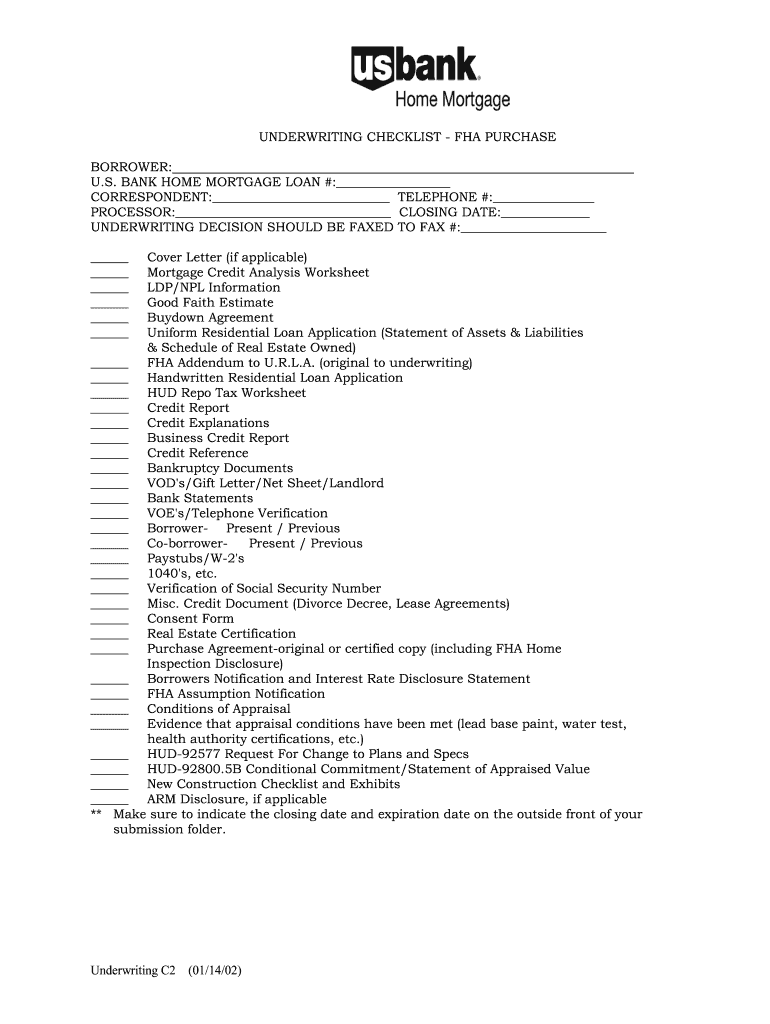

Definition and Meaning of the Mortgage Underwriting Checklist Template

A mortgage underwriting checklist template serves as a structured guide that outlines the essential documents and information required during the mortgage underwriting process. This checklist is crucial for lenders and borrowers alike, ensuring that all necessary documentation is collected and reviewed to assess the borrower's creditworthiness and the property's value. The underwriting process determines the risk of lending and plays a significant role in finalizing loan approvals.

This template typically includes sections for personal, financial, and property-related information, assisting in maintaining a comprehensive view of the borrower's situation. The inclusion of essential items such as income verification, credit history, and asset documentation ensures that no critical information is overlooked, thus expediting the approval process.

Key Elements of the Mortgage Underwriting Checklist Template

An effective mortgage underwriting checklist template is designed to capture all relevant information needed for a thorough review. Key elements include:

- Borrower Information: Full name, contact details, and social security number.

- Income Documentation: Recent pay stubs, tax returns, and W-2 forms for employment verification.

- Credit Reports: Recent credit history and scores must be pulled to evaluate risk.

- Asset Documentation: Bank statements, investment accounts, and any other proof of assets contributing to financial stability.

- Property Information: Details about the property in question, including purchase agreement, appraisal report, and title information.

These elements provide a comprehensive understanding of the borrower's financial health, enabling the underwriter to make informed decisions.

Steps to Complete the Mortgage Underwriting Checklist Template

The process of completing a mortgage underwriting checklist template involves several steps. These steps ensure all necessary documentation is gathered and organized:

- Collect Personal Information: Gather all identifying information about the borrower and co-borrower, if applicable.

- Compile Financial Documents: Assemble income verification documents, including pay stubs, tax returns, and bank statements. Ensure all documents are current, typically within the last few months.

- Request Credit Reports: Obtain the borrower's credit report from appropriate credit reporting agencies. A good score can facilitate loan approval.

- Review Property Documentation: Collect the purchase agreement and any appraisal reports reflecting the property's market value.

- Verify All Information: Cross-check each document and piece of information to ensure accuracy and completeness.

Completing these steps can streamline the underwriting process and prevent delays in loan approvals.

Important Terms Related to the Mortgage Underwriting Checklist Template

Understanding terminology in mortgage underwriting is essential for effective communication within the process. Here are several important terms:

- Debt-to-Income Ratio (DTI): A ratio used to evaluate a borrower’s ability to manage monthly payments and repay debts.

- Loan-to-Value (LTV): This ratio indicates the amount of loan compared to the appraised value of the property, impacting risk assessment.

- Pre-approval: A lender's commitment to providing a loan, often based on initial information provided by the borrower.

- Underwriting Guidelines: The criteria set by the lender that must be adhered to during the underwriting process.

Familiarity with these terms enhances understanding and ensures clarity in mortgage-related discussions.

Examples of Using the Mortgage Underwriting Checklist Template

Real-world scenarios illustrate the practical application of a mortgage underwriting checklist template, leading to successful loan processing. Here are two examples:

-

A first-time homebuyer seeking approval for an FHA loan can utilize the checklist to ensure they include necessary documentation like credit reports, proof of income, and an appraisal. By following the checklist, the buyer submits all documents in one go, reducing processing time and minimizing the chance of additional requests.

-

A real estate agent assisting a client with a conventional mortgage can leverage the checklist to track the required documentation for multiple properties. This organization helps maintain clarity and efficiency, ensuring all necessary information is readily available for the underwriters' review.

These examples reflect how employing the checklist facilitates a smoother mortgage process.

Who Typically Uses the Mortgage Underwriting Checklist Template

The mortgage underwriting checklist template is primarily used by several key players in the mortgage industry, including:

- Mortgage Underwriters: Professionals responsible for evaluating loan applications and deciding on risk.

- Lenders: Banks and financial institutions that provide the mortgage, ensuring they follow guidelines for approval.

- Loan Officers: Individuals who guide borrowers through the mortgage process and assist in documentation collection.

- Real Estate Agents: They often help clients understand what documentation is required for successful mortgage applications.

These stakeholders benefit from the uniformity the checklist provides, ensuring consistent data collection and review.

Required Documents for the Mortgage Underwriting Checklist Template

The mortgage underwriting checklist template outlines specific documents required for compliance and thorough evaluation. Commonly required documents include:

- Identification: Valid photo ID and Social Security card.

- Income Verification: Recent pay stubs, W-2 forms, and if self-employed, profit and loss statements and business tax returns.

- Credit History: Recent credit reports from recognized agencies that provide an overview of the borrower’s credit status.

- Asset Proof: Bank statements, retirement account statements, and other proof of liquid assets.

- Property Documents: Purchase offer, property appraisal, and title documents to validate property value and ownership.

Gathering these documents helps ensure accuracy and comprehensive evaluation during the underwriting process.