Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out 2018 Form 1041-T - Internal Revenue Service with DocHub

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open it in the editor.

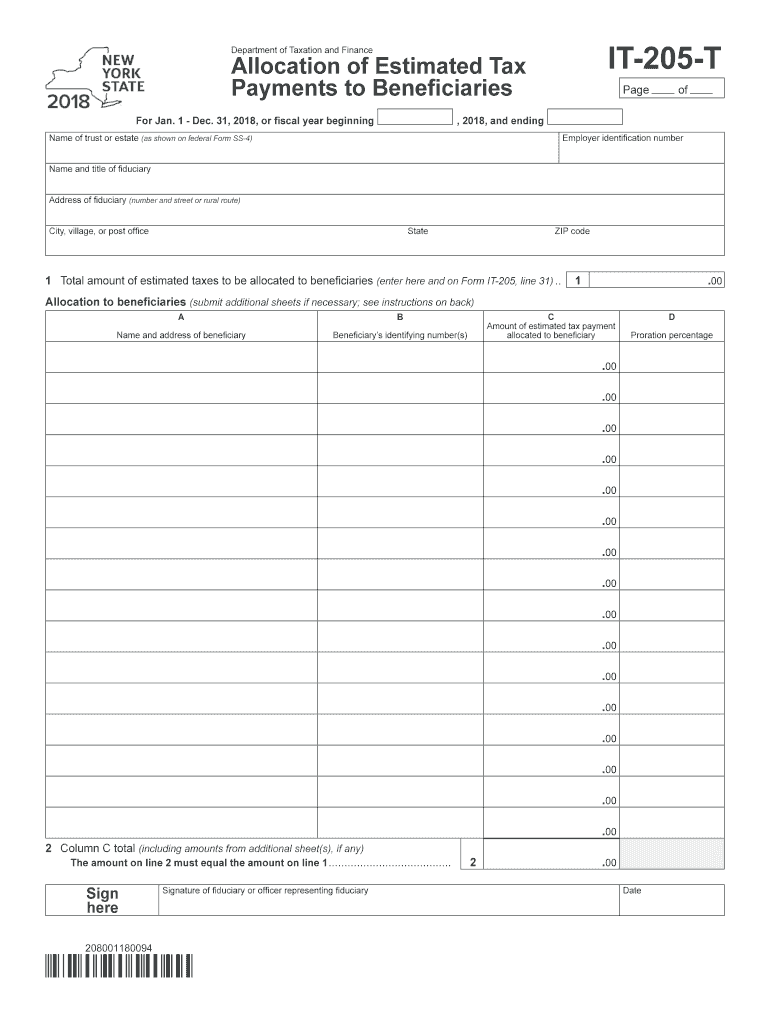

Begin by entering the name of the trust or estate as shown on federal Form SS-4, along with the employer identification number and fiduciary details.

In line 1, input the total amount of estimated taxes to be allocated to beneficiaries. This is crucial for accurate tax reporting.

For each beneficiary, list their name and address in Column A, followed by their identifying number(s) in Column B.

In Column C, specify the amount of estimated tax payment allocated to each beneficiary. Ensure that this total matches the amount entered in line 1.

Calculate the proration percentage for each beneficiary in Column D by dividing the amount in Column C by the total from line 1, rounding to four decimal places.

Finally, sign and date the form where indicated before submitting it as per filing instructions.

Start using our platform today to simplify your form completion process for free!

Fill out 2018 Form 1041-T - Internal Revenue Service online It's free

See more 2018 Form 1041-T - Internal Revenue Service versions

We've got more versions of the 2018 Form 1041-T - Internal Revenue Service form. Select the right 2018 Form 1041-T - Internal Revenue Service version from the list and start editing it straight away!

2018 form 1041 t internal revenue service pdf2018 form 1041 t internal revenue service instructionsIRS Form 1041 for 2025 PDF downloadIRS Form 1041 for 20242018 form 1041 t internal revenue service downloadForm 1041 instructionsIRS Form 1041 instructions 2025IRS Form 1041 for 2024 PDF download

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

Purpose of Form. A trust or, for its final tax year, a decedents estate may elect under section 643(g) to have any part of its estimated tax payments (butRead more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.