Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out tdai 2423 with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the tdai 2423 in the editor.

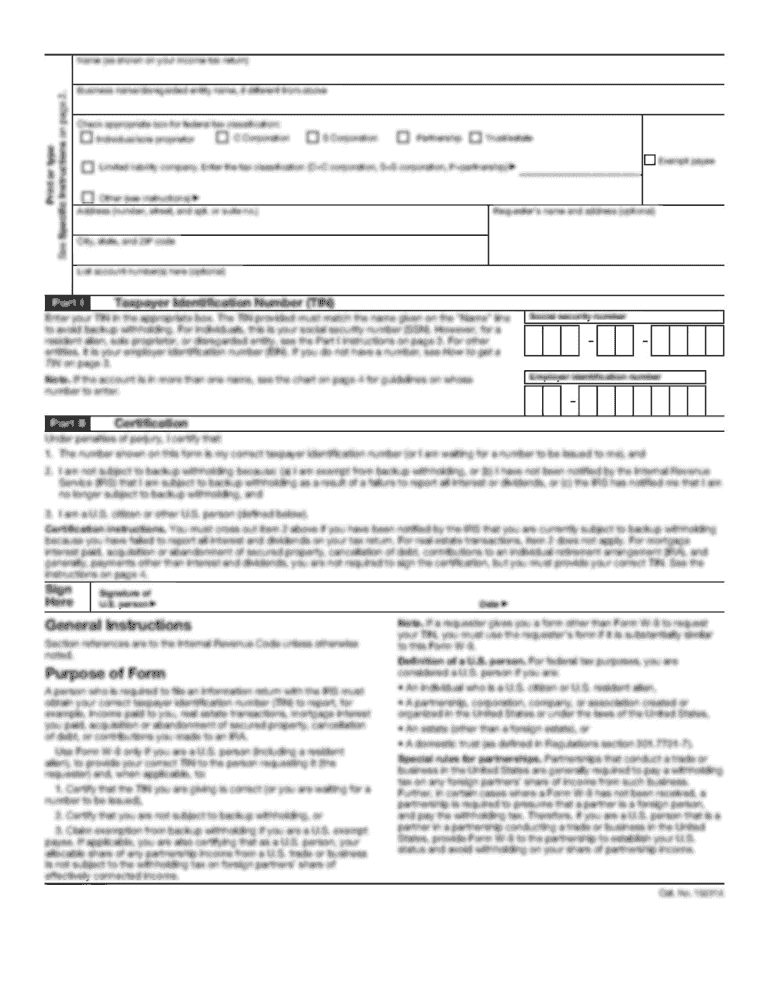

Begin by filling out the Account Owner Information section. Enter your name, Social Security Number, and contact details accurately.

In the Type of Distribution section, select the reason for your distribution by checking the appropriate box. Ensure you understand each option before making a selection.

Proceed to Payment Amount. Indicate whether you want a partial or full distribution and specify the amount or securities if applicable.

Select your Method of Payment. Choose how you would like to receive your funds, ensuring all necessary details are filled in correctly.

Complete the Tax Withholding Election section by indicating your preferences for federal and state tax withholding.

Finally, sign and date the form in the Account Owner Authorization section to certify that all information is accurate.

Start using our platform today to complete your tdai 2423 form easily and for free!

How much federal tax should I withhold from an IRA withdrawal?

Unless you instruct us not to withhold taxes, the IRS requires us to withhold at least 10% of your withdrawals from traditional IRAs, SEP-IRAs, and SIMPLE IRAs for federal income taxes. When you request a distribution online, by phone, or by mail, you can: Let us automatically withhold 10% of the distribution.

Is 20% withholding mandatory on IRA distributions?

Retirement plans: A retirement plan distribution paid to you is subject to mandatory withholding of 20%, even if you intend to roll it over later. Withholding does not apply if you roll over the amount directly to another retirement plan or to an IRA.

What states have mandatory withholding on IRA distributions?

AR, CA, CT, DE, IA, KS, MA, ME, MI, MN, NC, OK, OR, VT MANDATORY STATE INCOME TAX WITHHOLDING If state withholding applies, it will be calculated based on your states applicable minimum withholding requirement as specified below.

What percentage tax should be withheld from IRA withdrawal?

In most cases, IRA cash distributions are subject to a default 10% federal withholding rate. However, the 10% rate may not be suitable for your tax situation. In that case, you have the option of choosing to have a higher rate withheld or to waive withholding altogether.

How much tax should I withhold from inherited IRA distribution?

Withdrawals of contributions from an inherited Roth are tax free. Most withdrawals of earnings from an inherited Roth IRA account are also tax-free. However, withdrawals of earnings may be subject to income tax if the Roth account is less than 5-years old at the time of the withdrawal.

Related Searches

Tdai 2423 reviewsTdai osuTdai affiliateTdai workshopTdai eventsTdai fall forumMaster of translational data analyticsOhio state university computer science faculty

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

Oct 7, 1998 tdaI of eight (8) houre. ThIs 100 Toch Prop program. Studonls 2423 Organic Chemistry I (4). (This Is a common course number. FormerRead more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.