Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

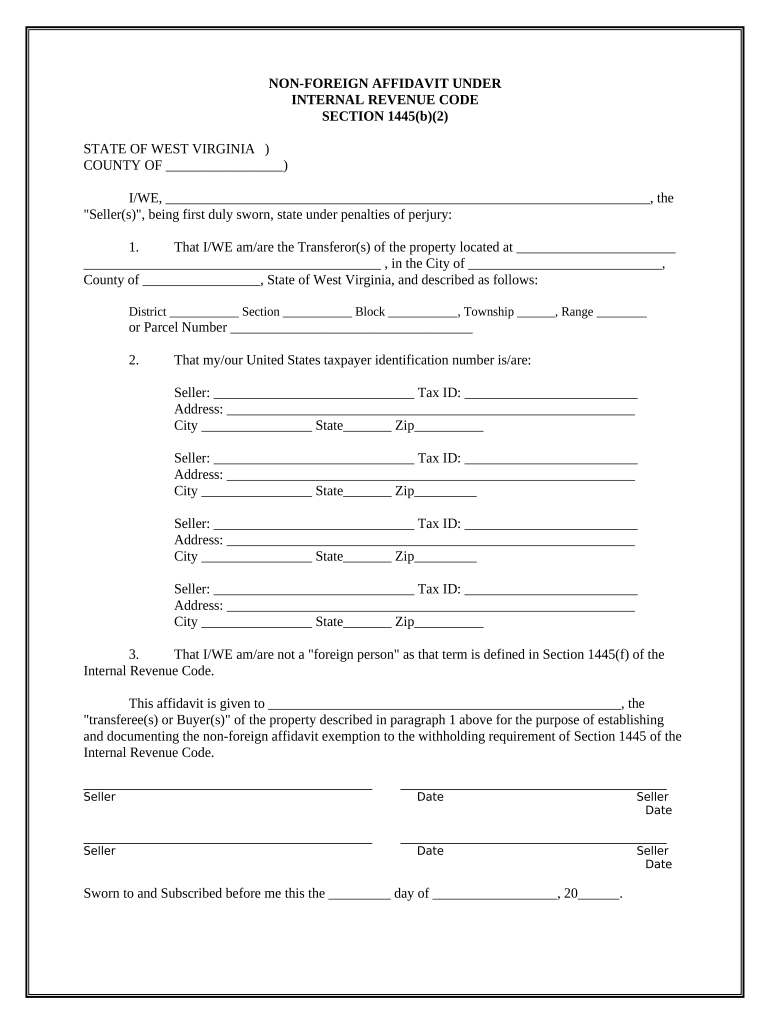

How to use or fill out Non-Foreign Affidavit Under IRC 1445 - West Virginia with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the Non-Foreign Affidavit Under IRC 1445 in the editor.

Begin by entering the names of the sellers in the designated field at the top of the form. Ensure that all sellers are accurately listed.

In Section 1, provide the complete address of the property being transferred, including city, county, and state. Fill in any additional details such as district and parcel number as required.

For Section 2, input each seller's taxpayer identification number along with their corresponding addresses. Make sure to double-check for accuracy.

In Section 3, confirm that you are not a 'foreign person' as defined by Section 1445(f) of the Internal Revenue Code by checking the appropriate box or providing a statement if necessary.

Finally, have all sellers sign and date the affidavit at the bottom. Ensure that a notary public is present to witness and notarize your signatures.

Start using our platform today to easily fill out your Non-Foreign Affidavit for free!

Fill out Non-Foreign Affidavit Under IRC 1445 - West Virginia online It's free

Non foreign affidavit under irc 1445 west virginia templateNon foreign affidavit under irc 1445 west virginia sampleNon foreign affidavit under irc 1445 west virginia formNon foreign affidavit under irc 1445 west virginia exampleFIRPTA affidavitFIRPTA Non foreign affidavitFIRPTA for dummiesFIRPTA certificate

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

Advising Foreign Investment in U.S. Real Estate, or How to

by ML Camp 1997 III. TELL YOUR CLIENT. A. Costs. B. Federal and State Laws on Foreign Ownership. 1. State Restrictions. 2. Federal Restrictions.Read more

3.21.261 Foreign Investment in Real Property Tax Act

In general, a copy of Form 8288-A stamped by the IRS must be attached to the transferors (sellers) return to establish the amount withheld under IRC 1445(a)Read more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.