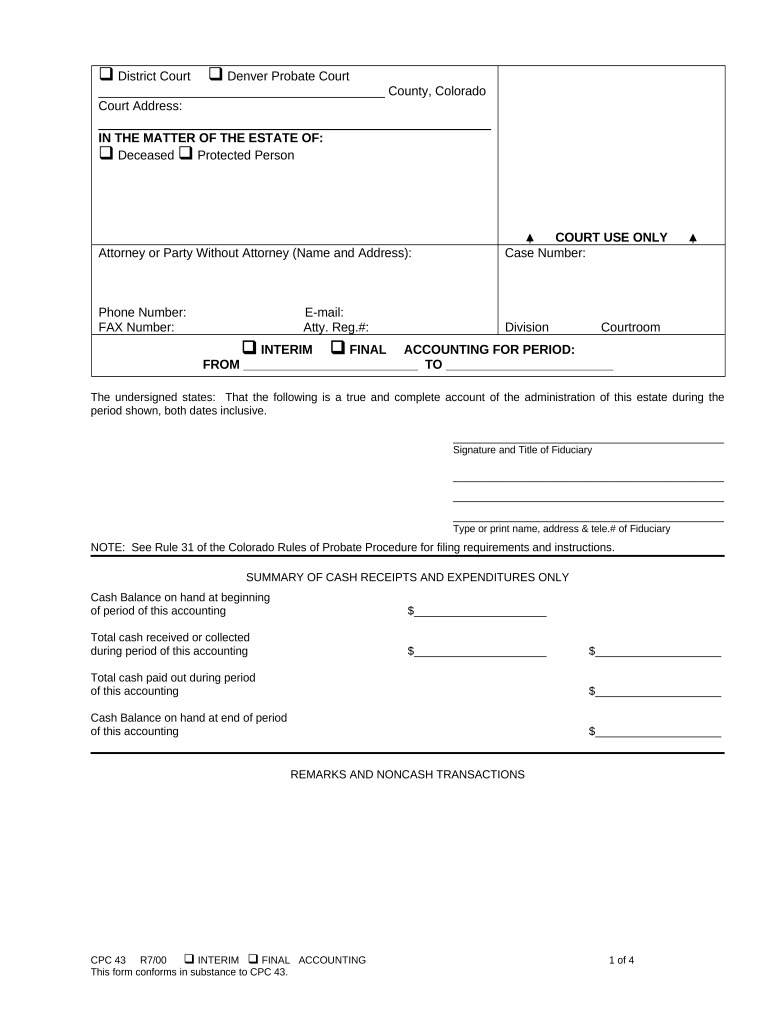

Definition and Meaning of the Final Accounting Form

The final accounting form is a document used primarily in the context of estate administration, particularly during the probate process. This form comprehensively captures all financial transactions that occurred during the administration of a decedent's estate. It typically includes sections for reporting cash receipts, expenditures, distributions to beneficiaries, and a statement of remaining assets. The purpose of the final accounting form is to provide an accurate and transparent financial report to the probate court, ensuring that all parties involved can verify that the estate has been managed according to legal and fiduciary standards.

Key features of the final accounting form include:

- Detailed itemization of all estate transactions: This includes income generated by the estate, expenses incurred, and how assets were distributed.

- Clear timelines: The form typically covers a specific period, often concluding with the date that the estate is finally settled.

- Final accounting report requirements: The form must comply with local probate court rules, which can vary significantly between jurisdictions.

Steps to Complete the Final Accounting Form

Completing the final accounting form accurately is crucial for legal compliance and transparency. Here’s a structured approach:

-

Gather Documentation: Collect all financial records related to the estate, including bank statements, invoices, receipts for expenses, and records of asset valuations.

-

Prepare a Cash Receipts Section: Detail all income received by the estate, such as rental income, interest, or proceeds from the sale of assets. Each entry should include the date, source, and total amount.

-

Itemize Expenditures: Document all expenses incurred in the process of managing the estate. This includes funeral costs, taxes, property maintenance, and legal fees. Again, provide dates and amounts for each entry.

-

List Distributions: If any distributions have been made to heirs or beneficiaries, clearly outline the amounts and dates of these transactions. This section should show how the estate's assets have been shared.

-

Include a Statement of Remaining Assets: Report all remaining assets at the conclusion of the accounting period. This might include cash accounts, real estate, and personal property. Each asset should be clearly described.

-

Review and Sign: After compiling all information, review the form for accuracy. Once confirmed, the personal representative or executor must sign the document to validate it.

Completing these steps requires attention to detail, as any inaccuracies or omissions can lead to complications during the probate process.

Important Terms Related to Final Accounting Form

Understanding specific terminology related to the final accounting form is essential for proper completion. Here are key terms to know:

- Executor: The individual named in a will or appointed by the court to manage a decedent's estate.

- Beneficiary: A person or entity entitled to receive a portion of the estate as outlined in the will or determined by law.

- Probate Court: The judicial body that oversees the probate process, including the validation of wills, appointment of executors, and approval of accountings.

- Asset Valuation: The process of estimating the worth of an asset at a given time, necessary for reporting on the final accounting form.

Familiarity with these terms helps ensure that the form is filled out correctly and in compliance with legal requirements.

Examples of Using the Final Accounting Form

Various scenarios may necessitate the completion of a final accounting form, illustrating its practical application:

-

Estate of a Deceased Relative: When settling an estate for a parent or sibling, the executor will need to document all income and expenses related to the estate's administration. This includes collecting income from rental properties, paying off debts, and distributing inheritance to heirs.

-

Trust Administration: For an estate held in a trust, trustees are required to provide a final accounting to beneficiaries. This includes detailing how trust income was managed and how principal was distributed.

-

Court Supervised Estate: In situations where the probate court has jurisdiction over the estate, the final accounting is submitted for approval. Judges review these documents to ensure transparency and proper fiduciary conduct.

These examples reflect the diverse contexts in which the final accounting form is utilized, each requiring thorough documentation and compliance with legal standards.

Legal Use of the Final Accounting Form

The legal implications of the final accounting form are significant. When filed in probate court, this form serves multiple legal functions:

-

Accountability: The final accounting acts as a formal record of the personal representative’s management of the estate. It holds the executor responsible for all financial transactions and decisions made during the probate process.

-

Court Approval: Many jurisdictions require that the final accounting form be approved by the probate court before distributing any remaining assets to beneficiaries. This step ensures that all claims against the estate have been settled and all debts accounted for.

-

Dispute Resolution: If beneficiaries or creditors contest the management of the estate, the final accounting serves as a critical piece of evidence. It can be used in mediation or court to clarify any misunderstandings related to financial transactions.

As such, accuracy and completeness in preparing this document are essential for legal protection and compliance.