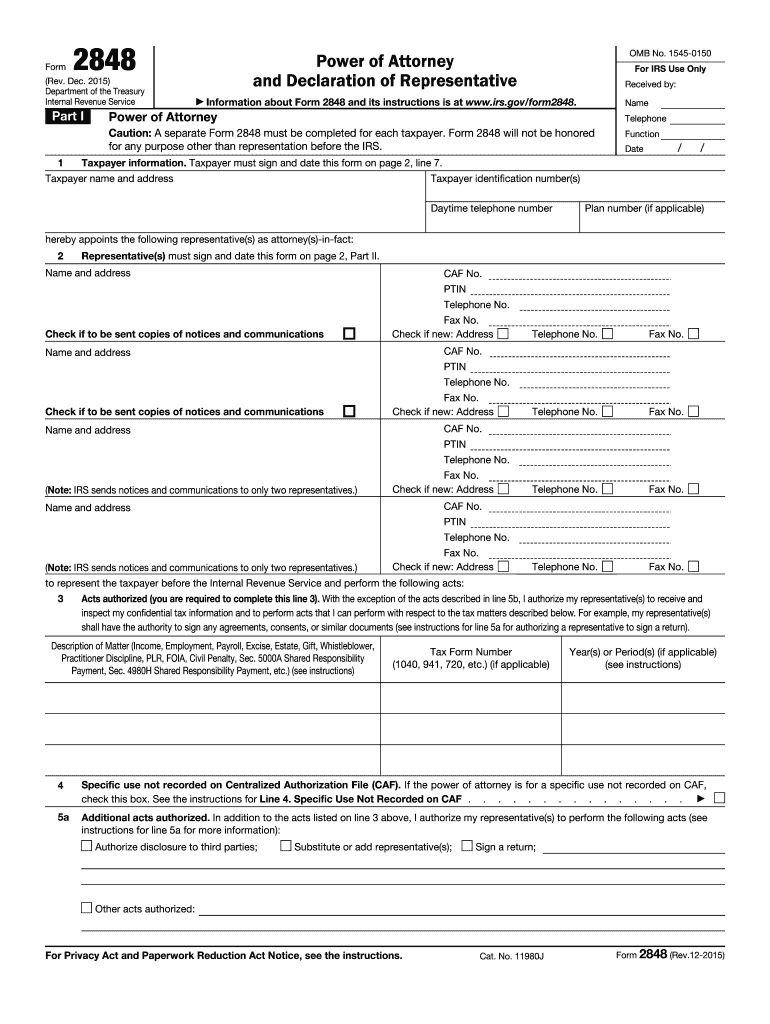

Definition and Purpose of IRS Form 2848

Form 2848, also known as the Power of Attorney and Declaration of Representative, is an official document used by taxpayers to authorize an individual to represent them before the Internal Revenue Service (IRS). This form is critical for those who require assistance with their tax matters and wish to grant someone access to their tax information or to perform acts on their behalf. The document includes sections that outline taxpayer information, details of the representatives appointed, and explicitly specifies the acts the representative is authorized to carry out, ensuring clear communication with the IRS.

Key Elements of Form 2848

Understanding the components of Form 2848 is essential to complete it accurately. Key sections include:

- Taxpayer Information: Personal details such as name, address, and taxpayer identification number.

- Representative’s Details: Information on the appointed representative(s), including their designation and contact details.

- Acts Authorized: Specifics of what the representative can do, like receiving and inspecting tax returns.

- Revocation Option: Instructions on how taxpayers can revoke previously granted powers.

- Declaration of Representative: Certification by the representative confirming their qualifications to practice before the IRS, adhering to eligibility requirements.

How to Obtain Form 2848

Form 2848 can be accessed through several methods to accommodate different preferences and technology accesses:

- Online: The form is available for download on the IRS official website, ensuring easy access for most users.

- By Mail: Requesting a physical copy from the IRS office may be an alternative for those who prefer or require paper forms.

- Professional Services: Tax professionals often have copies and can provide them during consultation or representation agreements.

Steps to Complete Form 2848

Filling out Form 2848 accurately is crucial. Follow these detailed steps:

- Enter Personal Information: Provide your name, mailing address, social security number, and daytime phone number.

- Designate a Representative: Fill in the details of the individual(s) you are authorizing, including their name, address, and Centralized Authorization File (CAF) number.

- Determine Specific Authorizations: Specify the types of tax matters and periods the representative can handle.

- Sign and Date the Form: Ensure both the taxpayer and representative sign and date the document where designated.

- Submit: File the completed form with the IRS, choosing an appropriate submission method: fax, mail, or electronic submission.

Legal Use and Compliance

Form 2848 is legally binding and must be used in compliance with IRS regulations. It grants significant authority to the representative but is strictly limited to the powers granted within the form. Misuse or failure to comply with IRS guidelines may lead to revocation or penalties. Users must ensure all details are correct and up-to-date to avoid legal complications.

Penalties for Non-Compliance

Failure to properly execute or misuse Form 2848 can lead to several consequences:

- Revocation of Authorization: Incorrect usage can result in the immediate withdrawal of the representative’s authority.

- Potential Fines: Engaging in unauthorized acts or making false declarations may incur fines or additional penalties from the IRS.

- Legal Consequences: Deliberate misuse can result in legal action, emphasizing the importance of understanding and complying with all form requirements.

Form Submission Methods

Taxpayers can submit Form 2848 through various methods, ensuring flexibility and convenience:

- Online Submission: Using the IRS website or authorized e-services to upload the form directly.

- Mail: Sending physical copies to designated IRS addresses.

- Facsimile: Faxing the form to the IRS, which is often the fastest for urgent authorizations.

Who Typically Uses Form 2848

Form 2848 is primarily used by taxpayers who face complex tax situations or need someone to manage their IRS interactions. Common users include:

- Individuals: Those seeking assistance with personal tax issues.

- Businesses: Entities appointing representatives for audit-related or ongoing tax matters.

- Tax Professionals: Accountants or legal advisors needing official authorization to act on behalf of their clients.

This variety of users reflects the broad applicability of the form across different tax scenarios.