Definition and Purpose of Form 5472

Form 5472 is a critical document utilized by the Internal Revenue Service (IRS) to gather information from U.S. corporations with at least 25% foreign ownership or foreign corporations engaged in a U.S. trade or business. It is an information return that primarily captures details about reportable transactions between the reporting corporation and its foreign or domestic related parties during the tax year. By ensuring compliance with sections 6038A and 6038C of the Internal Revenue Code, the form provides transparency in cross-border financial transactions and helps in assessing potential tax liabilities.

How to Use the Form 5472 Instructions 2011

The "Form 5472 Instructions 2011" guide provides detailed steps for accurately completing and filing Form 5472. Taxpayers must adhere to these instructions to ensure accurate reporting of transactions and ownership details. The instructions clarify who must file, how to report specific types of transactions, and which financial details are necessary, thus facilitating compliance. They highlight fields to be filled, which are crucial for minimizing errors that could lead to penalties.

Steps to Complete Form 5472

- Identify Required Parties: Determine if the corporation is obligated to file Form 5472 by confirming foreign ownership levels or engagement in U.S. business activities.

- Gather Transaction Information: Collect data on all reportable transactions such as sales, rents, royalties, and more between the reporting corporation and related entities.

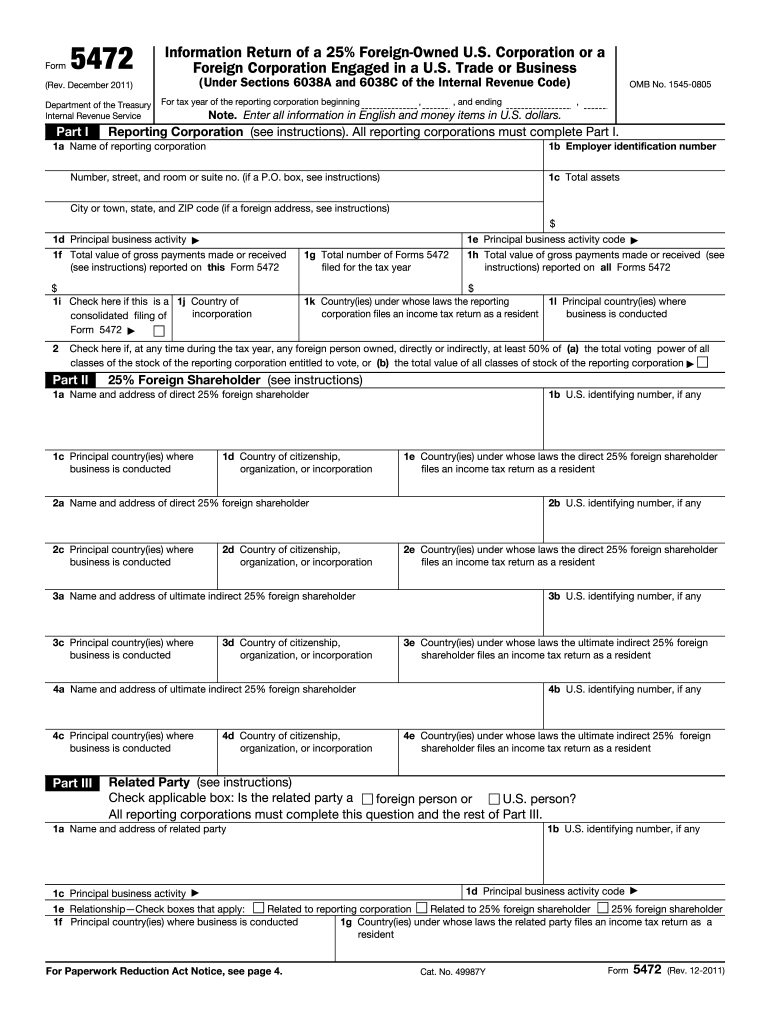

- Complete Part IV and V for Related Parties: Accurately list each foreign owner and related party, including their names and addresses, in Parts IV and V.

- Record Financial Information: Report total amounts of sales, purchases, and other financial exchanges in Part VI. This section is critical for disclosing the financial interactions regulated under the form.

- Submit Alongside Form 1120: Form 5472 must be submitted with the corporate income tax return, Form 1120, to the IRS.

- Maintain Records: Keep detailed records of all reported transactions and related documentation, as the IRS requires proof of records upon request.

Who Typically Uses Form 5472 Instructions 2011

Primarily, Form 5472 is used by U.S. corporations with substantial foreign ownership and foreign corporations conducting business in the U.S. These entities must comply with IRS regulations to report financial transactions and maintain transparency. Accountants and tax professionals commonly refer to these instructions to guide corporations through the completion and filing process, ensuring all legal requirements are met.

Penalties for Non-Compliance

Failure to file Form 5472 accurately and timely can result in substantial penalties. An initial fine of $25,000 may be imposed for failing to file or inaccurate filing, with additional penalties accumulating if the issue is not corrected promptly. These penalties underscore the significance of following the specific guidelines in the form's instructions to avoid costly repercussions.

Filing Deadlines and Important Dates

Form 5472 is due when the corporation's tax return, Form 1120, is due, including extensions. Typically, this means the form is due by the 15th day of the fourth month following the close of the corporation's fiscal year. For calendar year corporations, this is usually April 15. However, if foreign ownership is involved, it might require additional consideration for extensions and timing adjustments.

Key Elements of Form 5472

Form 5472 comprises several critical sections, including:

- Part I: Identifying Information - Contains the basic information about the reporting corporation.

- Part II: Principal Business Activity Codes - These codes help categorize the type of business operations performed.

- Part IV: Related Party Information - Lists and details each related party engaged in reportable transactions.

- Part VI: Financial Information - Records the financial details of transactions that transpired between the corporation and related parties, making it pivotal for assessment.

IRS Guidelines and Compliance

The IRS guidelines for Form 5472 ensure corporations report accurately to maintain compliance and avoid penalties. These guidelines stipulate precise definitions of reportable transactions and related parties, providing clarity on the mandatory disclosure of these financial interactions. Compliance with these guidelines is vital to prevent disputes and legal issues related to cross-border financial transactions.