Definition & Meaning

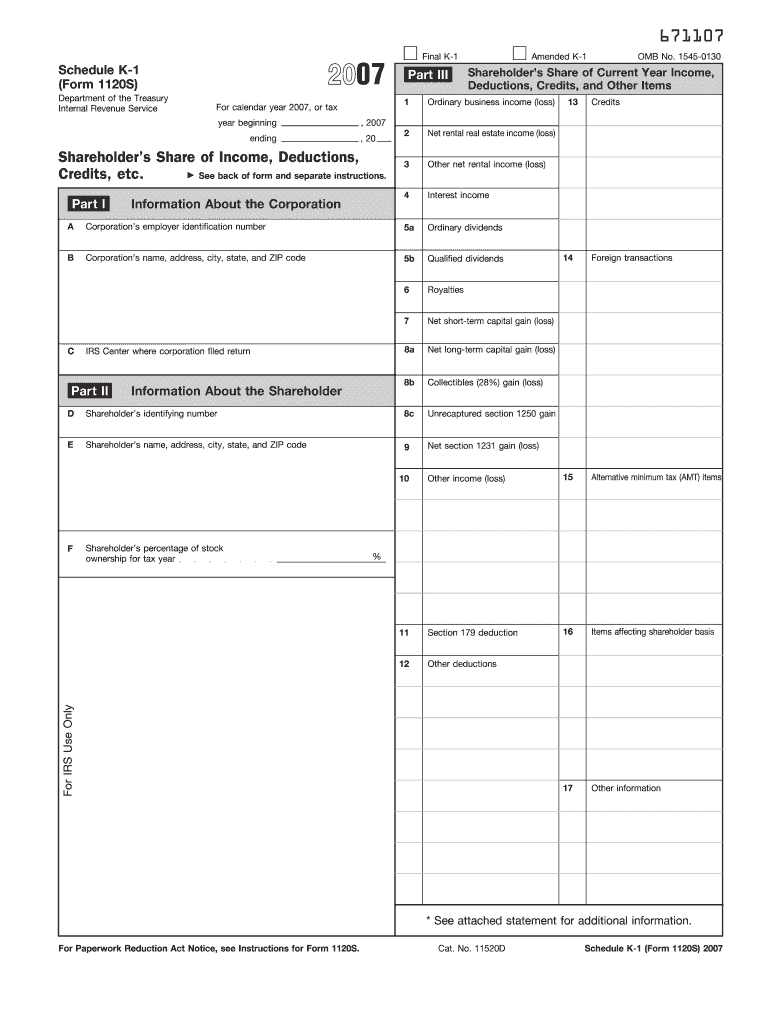

The Schedule K-1 (Form 1120S) for 2007 is a form used by S corporations to report each shareholder's share of the corporation's income, deductions, and other financial information. This form is integral for shareholders as it aids in preparing their individual income tax returns. The 2007 version specifically reflects financial transactions and allocations for the tax year 2007, detailing elements such as ordinary business income and dividends.

Key Components

- Ordinary Business Income: Reflects the net income from normal business operations.

- Dividends and Capital Gains: Includes income from investments and sales of assets.

- Deductions: Covers deductible expenses that can lower taxable income.

- Credits: Details tax credits allocated to shareholders for tax reduction.

How to Use the 2007 Form 1120S K-1

Shareholders use the details on Schedule K-1 (Form 1120S) to complete their personal tax returns, incorporating their allocated shares of the corporation’s income and deductions. This helps ensure accurate reporting of earned income and corresponding tax liabilities.

Steps for Utilizing the Form

- Review Allocated Items: Confirm the income, deductions, and credits assigned to you.

- Incorporate Into Tax Returns: Use the information to populate relevant sections of IRS Form 1040.

- Verify Accuracy: Double-check entries to ensure no discrepancies exist, which could lead to issues with the IRS.

Practical Scenarios

- Shareholders in different states may need to adjust entries for state-specific tax rules.

- If the corporation has foreign transactions, additional forms such as Form 1116 might be required.

How to Obtain the 2007 Form 1120S K-1

Typically, the S corporation is responsible for issuing the Schedule K-1 to its shareholders. It should be provided once the corporation has completed its tax return for the year.

Acquisition Process

- Direct Distribution: The corporation sends the K-1 directly to each shareholder, either via mail or electronically.

- Request from Corporation: If not received, shareholders can contact the corporation for a copy.

Steps to Complete the 2007 Form 1120S K-1

While the corporation completes the form itself, understanding the process is vital for shareholders.

- Compilation of Financial Data: Gather financial outcomes for the corporation's tax year.

- Determining Shareholder Allocations: Based on ownership percentage, calculate each shareholder's portion.

- Filling the Form: Document all financial data, ensuring accuracy in each category.

- Distribution of Form to Shareholders: Provide completed forms to each shareholder for tax filing purposes.

Key Elements of the 2007 Form 1120S K-1

Schedule K-1's structure is designed to capture comprehensive financial data related to an S corporation's taxable activities.

Major Sections

- Income Items: Include ordinary business income, interest income, and dividend income.

- Deductions and Losses: Encompass business expense deductions and operating losses.

- Credits and Withholdings: Document any tax credits and withholdings applicable to shareholders.

Legal Use of the 2007 Form 1120S K-1

The form serves as a legal document representing the shareholder's right to specific segments of the corporation's financial activities. Accurate completion is crucial to prevent legal complications or discrepancies in tax filings.

Compliance Guidelines

- IRS Requirements: Ensure all IRS guidelines are strictly followed to maintain compliance.

- Accuracy and Authenticity: Verify all entries against corporate ledgers and accounting records.

IRS Guidelines

The IRS provides in-depth instructions for both corporations and individual shareholders on accurately reporting the details contained within Schedule K-1.

Reporting Instructions

- Use of Form 1040: Incorporate K-1 data into the appropriate sections of the Form 1040.

- Record Keeping: Maintain copies of the K-1 for at least three years beyond the date the tax return was filed.

Filing Deadlines / Important Dates

Awareness of deadlines is critical to ensure compliance and avoid penalties.

Key Dates

- S Corporation Filing Deadline: Typically due on March 15 following the end of the tax year.

- Shareholder's Tax Return Deadline: Generally, April 15, aligned with individual tax filing deadlines, though extensions can be sought.

Who Typically Uses the 2007 Form 1120S K-1

This form is primarily used by individuals who are shareholders in an S corporation. These users are responsible for reporting their share of income, losses, and other pertinent details provided by the corporation.

Eligible Users

- S Corporation Shareholders: Individuals invested in the corporation.

- Tax Preparers: Professionals assisting individuals with their tax returns.

Understanding these aspects surrounding the 2007 Schedule K-1 (Form 1120S) ensures shareholders are well-equipped to manage their tax responsibilities with precision and compliance.