Definition and Meaning

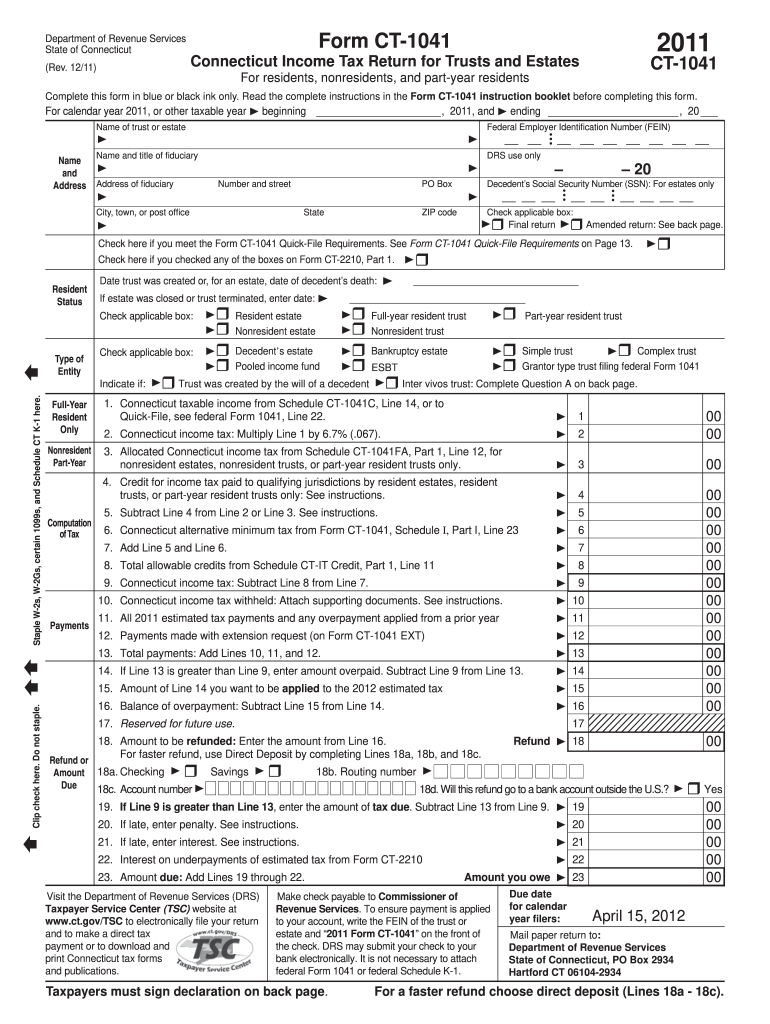

Trust and estate forms from CT.gov, such as the Connecticut Income Tax Return for Trusts and Estates (Form CT-1041), are essential documents used to report income tax for trusts and estates in Connecticut. These forms include sections for taxpayer information, income computation, tax calculations, payments, refunds, and required attachments. The purpose is to ensure accurate tax reporting and compliance with Connecticut tax laws for entities managing a deceased person's estate or functioning for the benefit of beneficiaries. Trust and estate forms are typically submitted by fiduciaries, including executors or administrators handling estate affairs.

Steps to Complete Trust and Estate Forms

-

Obtain the correct form: Start by downloading the Connecticut Trust and Estate forms, such as Form CT-1041, from the official CT.gov website. Ensure it is the latest version for the relevant tax year.

-

Fill in taxpayer details: Enter the trust or estate’s name, federal employer identification number (FEIN), and any other relevant contact information on the designated sections.

-

Compute income: Calculate all taxable income the trust or estate earned during the year. This could include dividends, interest, or other income types specified in the form instructions.

-

Determine deductions: Review applicable deductions and credits, and fill in these sections to reduce taxable income. Common deductions may include administrative expenses or fees related to managing the estate.

-

Calculate taxes due: Use the form instructions to compute the estate or trust's tax liability based on taxable income and deductions.

-

Attach necessary documentation: Include relevant documentation such as attachment schedules or supporting evidence required to substantiate claims on income or deductions.

-

Sign and submit: Ensure the form is signed by the fiduciary and submit it by the April 15 deadline, mid-April. Forms can be mailed or submitted electronically, depending on CT.gov's available submission methods.

How to Obtain Trust and Estate Forms

Forms like the CT-1041 can be accessed directly from the Connecticut Department of Revenue Services' website. You can download the forms as fillable PDFs or request a paper form by mail if preferred. Ensure you're using the version applicable to the specific tax year you're reporting for, as requirements may change annually.

- Online: Visit the official CT.gov site where digital versions are readily available.

- By mail: Request forms through the Department of Revenue Services; they will mail physical copies as necessary.

- Local offices: Forms may also be obtainable at designated government offices throughout Connecticut.

Important Terms Related to Trust and Estate Forms

- Fiduciary: An individual charged with managing assets for another party's benefit. In the context of estates or trusts, this often means the executor or trustee.

- FEIN: Federal Employer Identification Number required for trusts and estates when filing tax returns.

- Executor: A person appointed to administer the deceased person's estate according to a will or state laws.

- Beneficiary: An individual entitled to receive a part of an estate or trust proceeds.

State-Specific Rules for Trust and Estate Forms

Connecticut's tax laws and regulations may differ from other states. Fiduciaries must ensure familiarity with specific state requirements that govern how trust and estate income is reported:

- Residency rules: Determine whether the trust is considered resident or non-resident for Connecticut tax purposes.

- State deductions and credits: Familiarize yourself with Connecticut-specific modifications such as credits for taxes paid to other jurisdictions.

- Filing requirements: Connecticut may have different thresholds for filing, compared to federal requirements, especially concerning income levels or beneficiary types.

Filing Deadlines and Important Dates

Connecticut's rules stipulate April 15 as the deadline for filing returns like the CT-1041. If this date falls on a weekend or public holiday, the due date may be extended to the next business day. Extensions may also be requested if additional time is needed to file returns, though any taxes owed must still be paid by the original deadline to avoid penalties.

- Filing period: January 1 through April 15.

- Extension requests: Typically must be filed by the original deadline.

- Payment dates: Taxes remain due by April 15, even with an extension.

Penalties for Non-Compliance

Failure to comply with filing requirements or deadlines can result in significant penalties:

- Late filing: Additional charges are applied based on the tax due and the delay length.

- Late payment: Interest accrues on unpaid taxes from the original due date to the payment date.

- Inaccurate reporting: Penalties may also apply to inaccuracies or fraudulent information provided within the forms.

Understanding these implications underscores the importance of timely and accurate form submissions.