Definition and Purpose of Form 5304-SIMPLE 2008

Form 5304-SIMPLE is designed for use by small employers in the United States who wish to offer a SIMPLE Individual Retirement Account (IRA) plan to their employees. This form serves as a model Savings Incentive Match Plan for Employees of Small Employers (SIMPLE), allowing employers to establish a retirement savings plan without the complexity of more extensive retirement plans. The document outlines the terms under which the SIMPLE IRA plan operates, including employee eligibility, contribution limits, and administrative procedures. This form enables businesses to set up a simple yet effective retirement savings option that complies with IRS regulations and benefits eligible employees.

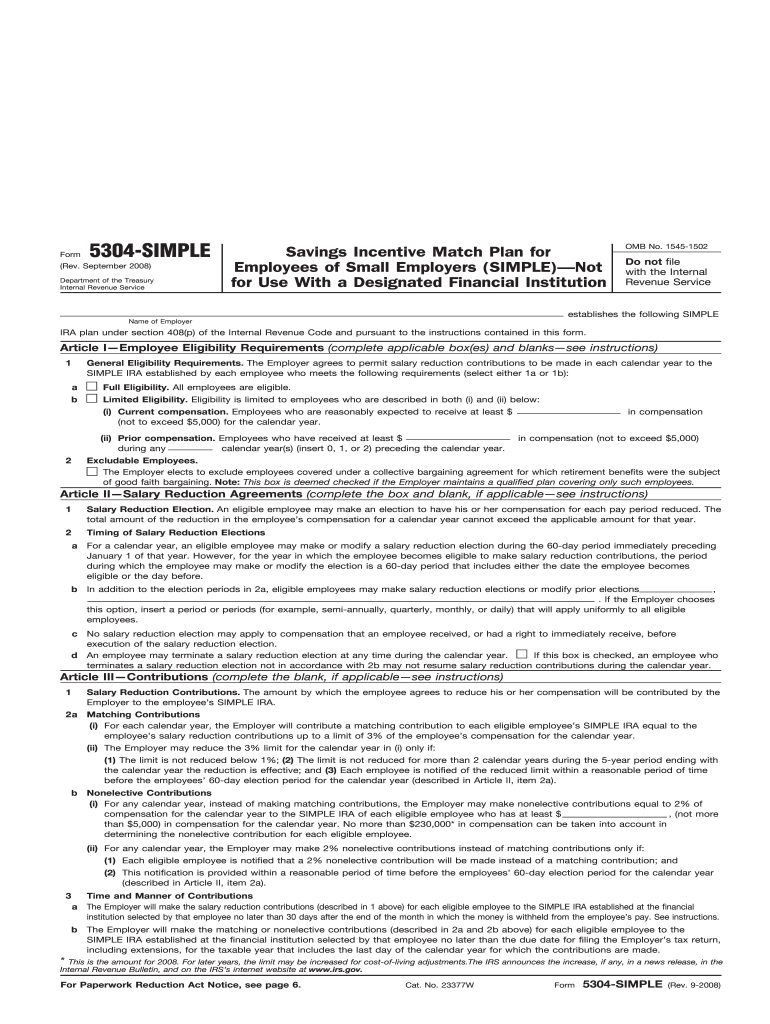

How to Utilize Form 5304-SIMPLE 2008

Employers should follow a specific process to effectively use Form 5304-SIMPLE. Initially, verify that your business qualifies as a "small employer" under IRS guidelines, typically defined as having 100 or fewer employees who earned $5,000 or more in the preceding year. Once eligibility is confirmed, employers should distribute the form to eligible employees, explaining the plan terms and any options available to them. Employers should then collect completed forms and manage contributions according to the instructions provided, ensuring compliance with the regulations outlined in the form.

Steps to Fill Out Form 5304-SIMPLE 2008

- Download the Form: Obtain the form from the IRS website or another reliable source.

- Complete Employer Information: Enter your business name, address, and Employer Identification Number (EIN) in the designated fields.

- Determine Employee Eligibility: Specify the eligibility criteria for your plan, which can include age and service requirements.

- Choose Contribution Method: Decide whether to match employee contributions or make nonelective contributions, specifying the percentage if applicable.

- Distribute Form to Employees: Provide copies to all eligible employees, explaining how they can participate in the SIMPLE IRA plan.

- Collect Completed Forms: Gather forms from employees who wish to participate and maintain records as required by your plan.

Key Components of Form 5304-SIMPLE 2008

Form 5304-SIMPLE includes several critical components that employers must understand to administer the plan properly:

- Eligibility Rules: Defines which employees are eligible to participate in the plan, generally based on age and length of service.

- Contribution Details: Outlines whether the employer will match employee contributions or make a flat percentage nonelective contribution.

- Employee Notifications: Details the information that must be provided to employees regarding their rights and responsibilities in the plan.

- Recordkeeping Standards: Establishes the requirements for maintaining and submitting necessary documentation related to the plan.

Legal Use of Form 5304-SIMPLE 2008

The legal use of Form 5304-SIMPLE involves ensuring compliance with IRS regulations regarding retirement savings plans. Employers must adhere to contribution limits, eligibility requirements, and notification procedures as stipulated by the form. Additionally, the form must be used in good faith, providing a fair and transparent retirement savings vehicle for all eligible employees. Employers should consult with a tax professional to ensure that all legal requirements are met and to maintain compliance with any updates to IRS regulations.

IRS Guidelines for Form 5304-SIMPLE 2008

The IRS provides specific guidelines concerning the establishment and operation of SIMPLE IRA plans using Form 5304-SIMPLE. These guidelines cover:

- Contribution Limits: Establishes the annual contribution maximums for both employers and employees.

- Tax Implications: Explains how contributions are taxed, both immediately and upon withdrawal.

- Filing Requirements: Although Form 5304-SIMPLE isn’t filed with the IRS, maintaining compliance-ready records is critical in case of audits.

Who Typically Utilizes Form 5304-SIMPLE 2008

Small employers across various industries utilize Form 5304-SIMPLE as an efficient way to offer retirement benefits. Companies with limited administrative resources find this form beneficial as it simplifies the process of establishing a compliant retirement plan. It's particularly useful for businesses in sectors like retail, hospitality, or regional services where employee turnover and seasonal employment are common.

Filing Deadlines and Important Dates for Form 5304-SIMPLE 2008

To ensure a compliant and successful SIMPLE IRA plan, adhere to key deadlines:

- Implementation Deadline: Employers must establish the plan before October 1st of the calendar year unless the business is newly formed after October 1st.

- Contribution Deadline: Deposits for each calendar year should be made within 30 days post-year-end or coinciding with the business's tax return filing deadline, including extensions.

Penalties for Non-Compliance

Failure to follow the requirements associated with Form 5304-SIMPLE can result in significant penalties. This includes potential disqualification of the plan, leading to immediate taxation of contributions and additional tax under IRC Section 4972. To avoid such penalties, employers must ensure proper execution and maintenance of the SIMPLE IRA plan while keeping abreast of any regulatory changes or updates from the IRS.