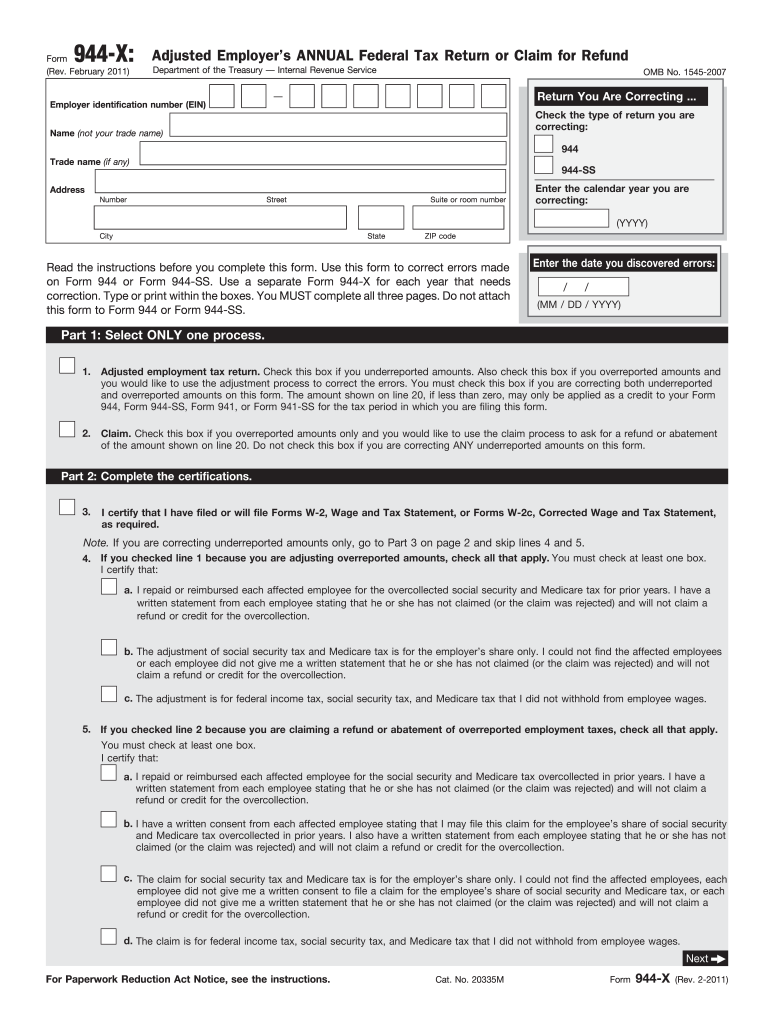

Definition and Purpose of Form 944-X

The Form 944-X, titled "Adjusted Employer's Annual Federal Tax Return or Claim for Refund," is specifically designed for employers in the United States who need to correct errors made on their annual federal tax return, specifically Form 944, related to employment taxes. This adjustment form is used to report both underreported and overreported amounts, providing employers with a structured process for making necessary corrections. It’s crucial to include an explanation of the corrections and obtain the required certifications to submit a valid adjustment or refund claim.

Steps to Complete Form 944-X

-

Enter Employer Information: Start by filling in your employer identification number (EIN), business name, and contact information. Accurate details are essential to ensure proper processing by the IRS.

-

Correcting Tax Categories: Identify which tax categories need adjustments by reviewing your initial Form 944. Adjustments could relate to social security wages and tips, Medicare wages and tips, or federal income tax withheld.

-

Detailing Adjustments: For each adjustment, provide a detailed explanation outlining the nature of the error. This should include how the error occurred and what corrections have been made. Ensure clarity to aid IRS understanding.

-

Certify Changes Made: Signing the form certifies that the information provided is accurate. The individual signing must be authorized to do so on behalf of the employer, often necessitating a corporate officer's signature or equivalent.

-

Calculate Adjusted Amounts: Complete the sections that require the calculation of the new correct amounts for each tax category. Ensure accuracy to avoid further discrepancies.

-

Submit for IRS Review: Once completed, submit the Form 944-X to the IRS. Follow the IRS instructions regarding submission location and keep a copy for your records.

Who Typically Uses Form 944-X

Form 944-X is employed primarily by small businesses or employers who initially filed Form 944. It's often used when:

- Errors are detected after filing Form 944, necessitating corrections.

- A refund is due because taxes were overpaid.

- Adjustments are needed because more information has become available after the initial submission.

Employers must stay vigilant in their bookkeeping practices to identify any discrepancies that necessitate filing this adjustment form.

Key Elements of the Form

-

Form Identification Information: Basic organizational details, including the EIN and business name, must be correctly filled out to ensure proper processing.

-

Adjusted Figures: The form requires entry of both the initially reported amounts and the corrected amounts in affected categories, facilitating transparent comparison and error rectification.

-

Explanatory Statement: An essential component where the filer must articulate reasons for the adjustments. The explanation must be detailed enough to address potential IRS queries.

-

Signature and Date: Official certification by an authorized person, confirming the adjustments’ accuracy and completeness.

IRS Guidelines

The IRS provides extensive instructions designed to help employers accurately complete Form 944-X. These guidelines cover:

- How to identify errors on the initial Form 944.

- Instructions for accurately entering corrections and ensuring all required fields are complete.

- Processes for determining any necessary payments or potential refunds.

It is highly recommended that employers closely adhere to these guidelines to ensure the proper handling of the corrective process.

Filing Deadlines and Important Dates

While Form 944-X does not have a strict deadline, it’s crucial to file it promptly upon discovering any errors to avoid potential penalties. Filing within three years of the original return's filing date or within two years of paying the tax, whichever is later, is often required for refund eligibility.

Form Submission Methods

-

Mail: Completed forms can be mailed to the address specified in the IRS instructions for Form 944-X. This remains a reliable method especially suited for businesses dealing with hard copy documents.

-

Electronic Filing: Although currently limited, some e-filing options might be available depending on software integrations used by the business.

Choosing the correct submission method can impact the processing time, and businesses should confirm receipt with the IRS.

Penalties for Non-Compliance

Failure to submit Form 944-X accurately can result in penalties. These can include:

- Accuracy-related Penalties: Applied if the corrected amounts are still inaccurate due to negligence.

- Late Filing Penalties: Imposed if the adjustment is not made within the IRS-specified timeframes after the original error is discovered.

Maintaining accurate records and promptly addressing discrepancies serve as preventive measures against such penalties.

Variants or Alternatives to Form 944-X

While Form 944-X specifically pertains to corrections on Form 944, other forms such as 941-X exist for correcting errors on different tax returns like the Form 941 series. Employers should use the form corresponding to the original return they filed and ensure they are addressing the right category of corrections needed for their situation.