Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send iht403 form pdf via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out iht403 download 2010 form with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the iht403 download 2010 form in the editor.

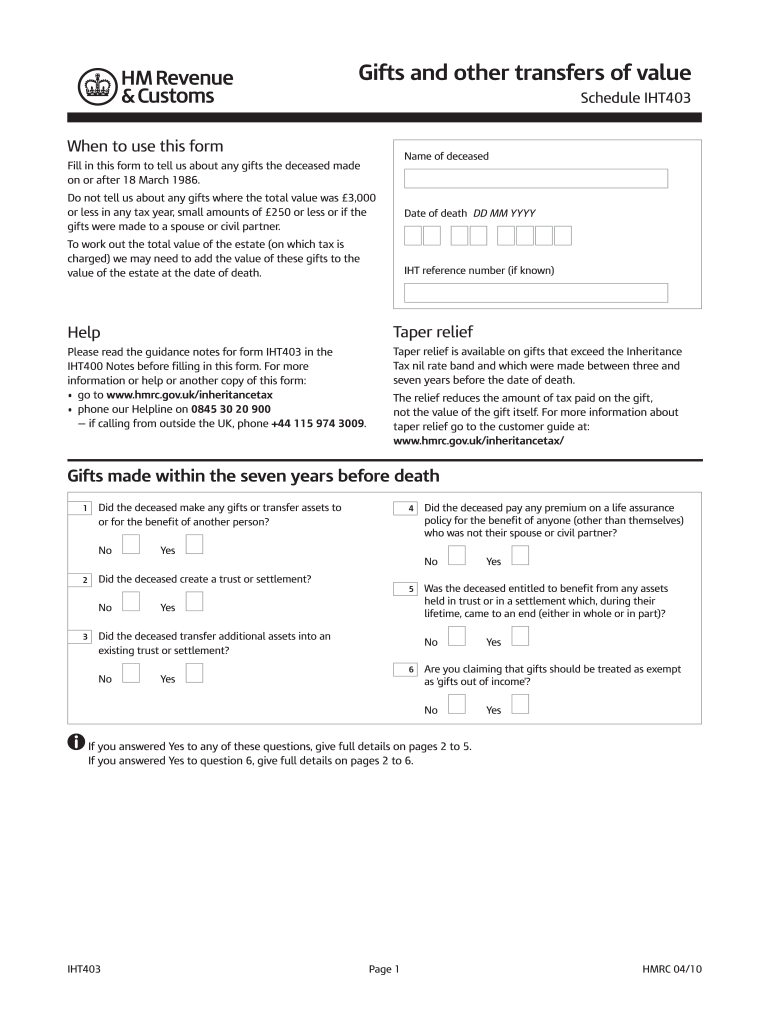

Begin by entering the name of the deceased and the date of death in the designated fields. Ensure accuracy as this information is crucial for processing.

Proceed to answer questions regarding gifts made by the deceased since March 18, 1986. For each gift, indicate whether it was made and provide details such as the recipient's name and relationship.

In sections regarding gifts with reservations, specify if any assets were transferred without full possession being granted. This includes answering questions about rights to benefit from those assets.

Complete any additional sections related to pre-owned assets or earlier transfers, ensuring all values are accurately calculated after exemptions or reliefs.

Review all entries for completeness and accuracy before saving your work. Utilize our platform’s features to easily edit or adjust any information as needed.

Start filling out your iht403 download 2010 form today for free using our platform!

Fill out iht403 download 2010 form online It's free

We've got more versions of the iht403 download 2010 form form. Select the right iht403 download 2010 form version from the list and start editing it straight away!

Iht403 download 2010 form pdf downloadIht403 download 2010 form pdfIht403 download 2010 form onlineIht403 download 2010 form freeIht403 download 2010 form excelIHT405IHT 400 formForm for gifting money

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.