Definition and Meaning of the W-8BEN Form for a UK Charity

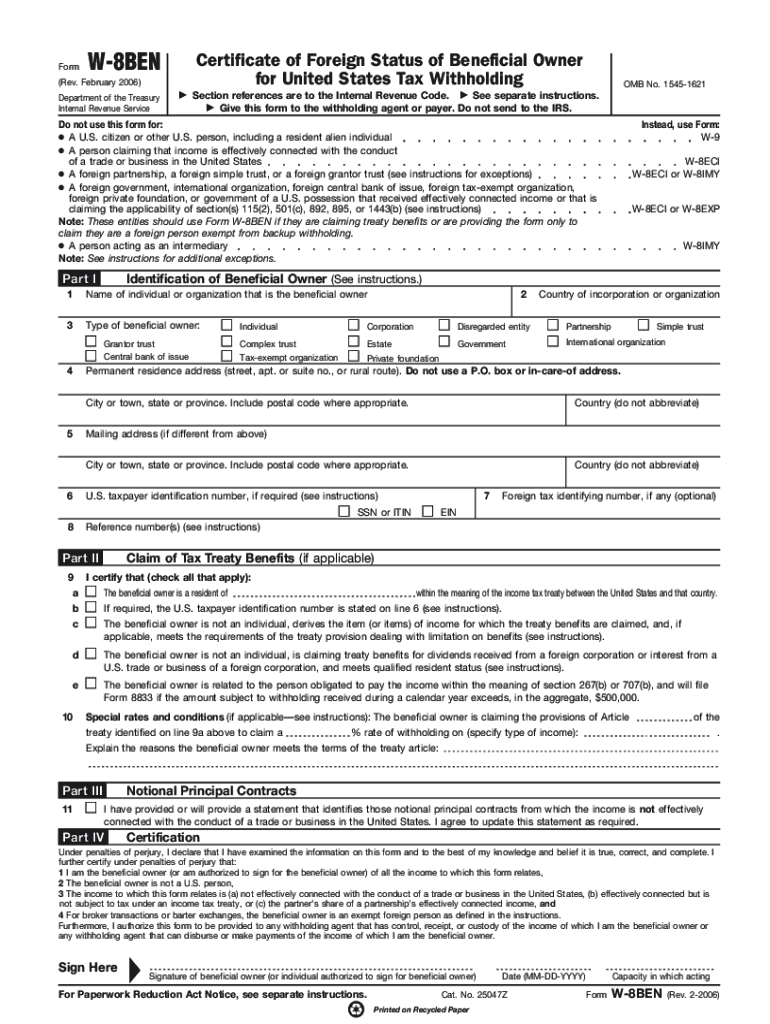

The W-8BEN form, officially known as the "Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals)," is a crucial document for UK charities conducting financial activities with U.S. institutions. Although primarily for individuals, charitable organizations use it to establish their foreign status and claim any applicable tax treaty benefits. This helps in reducing or eliminating U.S. withholding tax on income such as dividends or royalties.

How to Use the W-8BEN Form for a UK Charity

UK charities use the W-8BEN form to demonstrate their non-U.S. status and claim benefits provided under the U.S.-UK tax treaty. By submitting this form, charities can potentially exempt themselves from the default 30% withholding tax on U.S.-sourced income. Correct completion and submission of this form ensure the charity does not overpay taxes and complies with IRS requirements.

How to Obtain the W-8BEN Form for a UK Charity

The W-8BEN form can be obtained from the Internal Revenue Service (IRS) website. Charities can download it directly as a PDF, ensuring they have the latest version. Forms should be filled out accurately and kept on file in case of an IRS audit or when opening an account with a U.S. financial institution.

Steps to Complete the W-8BEN Form for a UK Charity

-

Identify Information: Enter the name of the charity and its institution type.

-

Permanent Address: Provide the charity's permanent UK address, confirming its foreign status.

-

Claim of Tax Treaty Benefits: Check the appropriate box to indicate the claim under the U.S.-UK tax treaty and specify the type of income that applies.

-

Sign and Date the Form: A responsible individual from the charity must sign the form, acknowledging the accuracy of the provided information.

Make sure each section is filled precisely to avoid processing delays or compliance issues.

Key Elements of the W-8BEN Form for a UK Charity

-

Identifying Information: Includes the charity's legal name and structure.

-

Country of Citizenship: Reaffirms the charity's non-U.S. status.

-

Type of Income: Specifics about income claimed for reduced withholding under the treaty.

-

Declaration: Certification that the charity is eligible for tax treaty benefits.

Each element must be completed to validate the exemption or reduction claim.

Legal Use of the W-8BEN Form for a UK Charity

The W-8BEN form must adhere to IRS guidelines, used strictly to claim treaty benefits that align with U.S. tax laws. False declarations might result in penalties or revocation of tax benefits, making legal compliance essential. The form is valid for three years from the date signed unless there is a change in circumstances that affects the information provided.

IRS Guidelines for the W-8BEN Form

According to IRS guidelines, UK charities must use the W-8BEN form to claim reduced tax withholding. The guidelines highlight specific sections relevant to charities, ensuring compliance with U.S. tax laws when dealing with U.S. income sources. The IRS periodically updates the form and instructions, so always refer to the latest version.

Filing Deadlines and Important Dates

While the W-8BEN form has no formal filing deadline, it should be submitted before the U.S. income is received to ensure the appropriate tax treatment. The form is typically updated every three years unless the charity's details or tax treaty benefits change sooner.

Required Documents for Completing the W-8BEN Form

While completing the W-8BEN form, the charity should have:

- Official Charity Registration Documents: To confirm legal status.

- U.S. Tax Identification Number (if applicable): Though not mandatory for all, it may support the tax treaty claim.

- Documentation of Eligible Income: Proof of income types claimed for treaty benefits.

Accurate documentation supports compliance and prevents disputes.

Penalties for Non-Compliance with the W-8BEN Form

Non-compliance, such as failing to submit or inaccurately completing the W-8BEN form, can lead to a default 30% withholding rate on U.S. income. Repeated non-compliance might lead to the IRS imposing fines or revoking treaty benefits. Charities should ensure accurate and timely submission to avoid these consequences.

Form Submission Methods

The completed W-8BEN form can be submitted directly to the payor or the financial institution responsible for managing the U.S.-sourced income. There is no need to send it directly to the IRS. Charities should follow the institution's specific instructions regarding submission, whether online, by mail, or in person.