Definition and Meaning

The 2012 Form 1098-E, or the Student Loan Interest Statement, is a tax document that reports the amount of student loan interest paid by borrowers in a given tax year. This form is crucial for individuals paying off student loans, as it may qualify them for a tax deduction. This typically applies to interest payments on federally backed student loans or other qualifying loans used to pay for higher education expenses. The 1098-E provides detailed information about the amount of interest paid, helping taxpayers determine their eligibility for a student loan interest deduction, which can reduce their taxable income.

How to Use the 2012 Form 1098-E

Understanding how to use the 2012 Form 1098-E effectively is essential for maximizing tax benefits. Taxpayers should carefully review the form to ensure accuracy of reported interest payments. If you have multiple loans, you might receive more than one 1098-E; ensure to consolidate the interest amounts accurately. After summarizing the interest paid, this amount is often transferred to the IRS Form 1040, specifically on line 33, as an "adjustment to income." However, everything must be verified against the current tax guidelines, since deduction rules can change.

Steps to Complete the 2012 Form 1098-E

- Receive the Form: Lenders typically send out the 1098-E by January 31. Ensure you receive this from every lender you’ve paid at least $600 in student loan interest.

- Review Information: Check that the borrower’s name, address, and other details are correct. Confirm the interest amount reported is what you paid during the year.

- Consolidate Interest Amounts: If you have multiple 1098-E forms, aggregate the interest amounts to determine your total interest paid.

- Report on Tax Return: Transfer the total interest amount to the appropriate section on your tax return, aligning with the IRS guidelines for student loan interest deduction.

- Maintain Records: Keep copies of all 1098-E forms and related documents as part of your tax records in case of audits or discrepancies.

Filing Deadlines and Important Dates

To ensure compliance, it’s imperative to keep track of important dates. Typically, lenders must furnish the 1098-E by January 31. Taxpayers should aim to file their tax returns by April 15 unless an extension is requested. Missing deadlines can lead to penalties or the omission of potential deductions, impacting your tax obligations. It’s advisable to confirm these timelines annually, as IRS deadlines can occasionally shift due to weekends or holidays.

Legal Use of the 2012 Form 1098-E

The 1098-E serves a legal purpose for documenting student loan interest paid for tax deduction. Taxpayers should use this form accurately to comply with IRS regulations. Altering or misrepresenting information on this form for tax benefits can lead to legal penalties, including fines or charges of tax fraud. Understanding the scope of this form is crucial for maintaining tax compliance while optimizing your tax return outcomes.

Key Elements and Components

Notable elements on the 2012 Form 1098-E include:

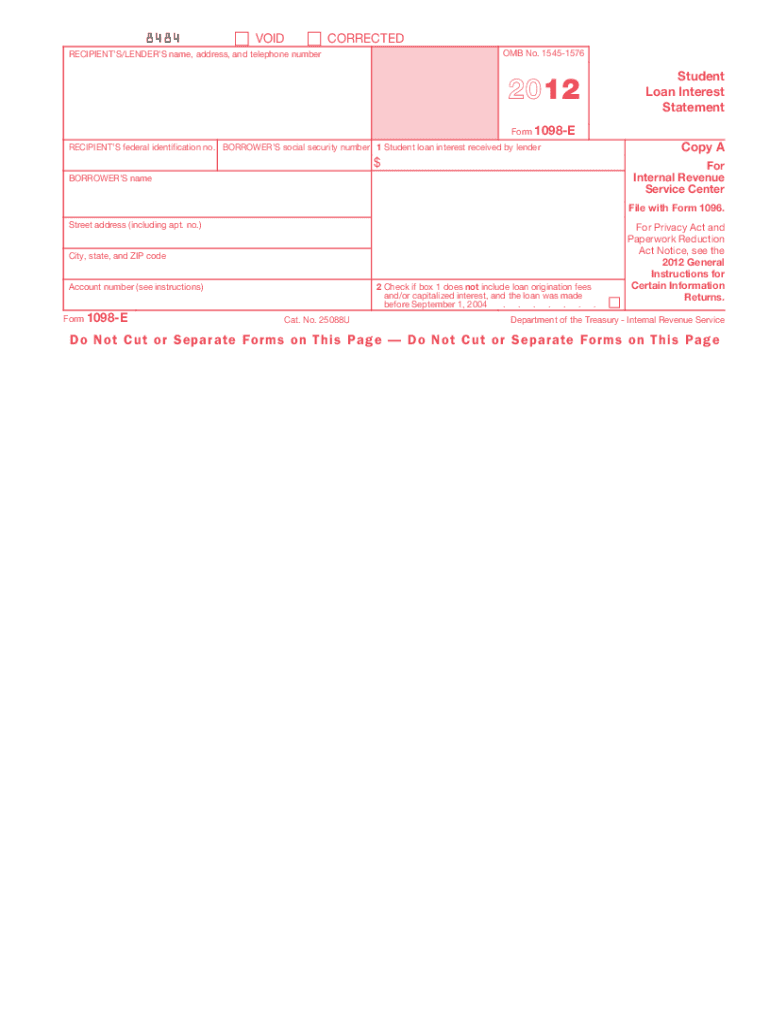

- Box 1, Student Loan Interest Received: This critical box reports the total interest received by the lender from the borrower during the tax year. It’s the primary figure used to determine the deduction.

- Borrower Information: Comprising the name and address of the individual who made the payments.

- Lender Information: Details about the lender or financial institution processing the loan.

These components are integral for any cross-referencing and future communications with tax consultants or the IRS.

Who Issues the Form

Typically, the lender or financial institution that services the student loan is responsible for issuing the 1098-E. These entities might include banks, credit unions, or dedicated student loan companies. They must provide this form to borrowers who have paid $600 or more in interest over the tax period. Should you not receive the form from your lender by the end of January, it’s crucial to follow up promptly to ensure you can meet your tax filing requirements.

Penalties for Non-Compliance

Non-compliance with 1098-E requirements can lead to significant repercussions. For lenders, failure to furnish the form to borrowers on time can result in penalties, while for borrowers, inaccuracies or failure to report the information correctly might result in the denial of deductions. Continuous misreporting or fraud could escalate to more severe penalties, including audits and legal action. Maintaining accurate records and compliance with IRS filing standards are essential for mitigating any potential risks associated with non-compliance.