Definition and Meaning of 1099-C 2013 Form

The 1099-C form is specifically designed for reporting canceled debts to the Internal Revenue Service (IRS). Issued by creditors, this form documents instances where a portion or all of a debt has been forgiven. For the 2013 tax year, the 1099-C encompasses various types of debt cancelations, including loans and credit card balances. Several events trigger the issuance of this form, such as a creditor deciding to stop attempting to collect on a debt or having a debt discharged through bankruptcy.

How to Use the 1099-C 2013 Form

The primary purpose of the 1099-C form is for taxpayers to report canceled debts on their tax returns. Upon receiving the form, individuals should verify the accuracy of the information, including the amount of canceled debt, as it is considered taxable income. This form typically accompanies the taxpayer's annual tax return and is used to ensure that all income, including forgiven debt, is properly declared.

Steps to Complete the 1099-C 2013 Form

- Verify Personal Information: Ensure that details such as name, address, and taxpayer identification number are correct.

- Review Creditor Information: Confirm the accuracy of the lender's details and the reported amount of debt canceled.

- Check for Specifics: Examine any additional information boxes for details about the nature of the debt cancelation.

- Report on Tax Return: Include the forgiven debt as income on your annual tax return using this form as a reference.

IRS Guidelines for the 1099-C 2013 Form

The IRS requires that the 1099-C form be issued for debts of $600 or more that have been canceled. However, there are exceptions to this rule, such as debts discharged in bankruptcy or insolvency. Taxpayers need to follow the IRS Publication 4681 for comprehensive guidance on canceled debts, as it explains how to report these amounts accurately and any potential exclusions.

Legal Use and Compliance

Form 1099-C must be used in accordance with IRS regulations for reporting canceled debt. Failing to report a debt cancelation can result in penalties or audits. It is crucial for both creditors and debtors to adhere to these guidelines to avoid legal complications. For legal purposes, retaining copies of correspondence related to the 1099-C and any supporting documentation for a minimum of three years is recommended.

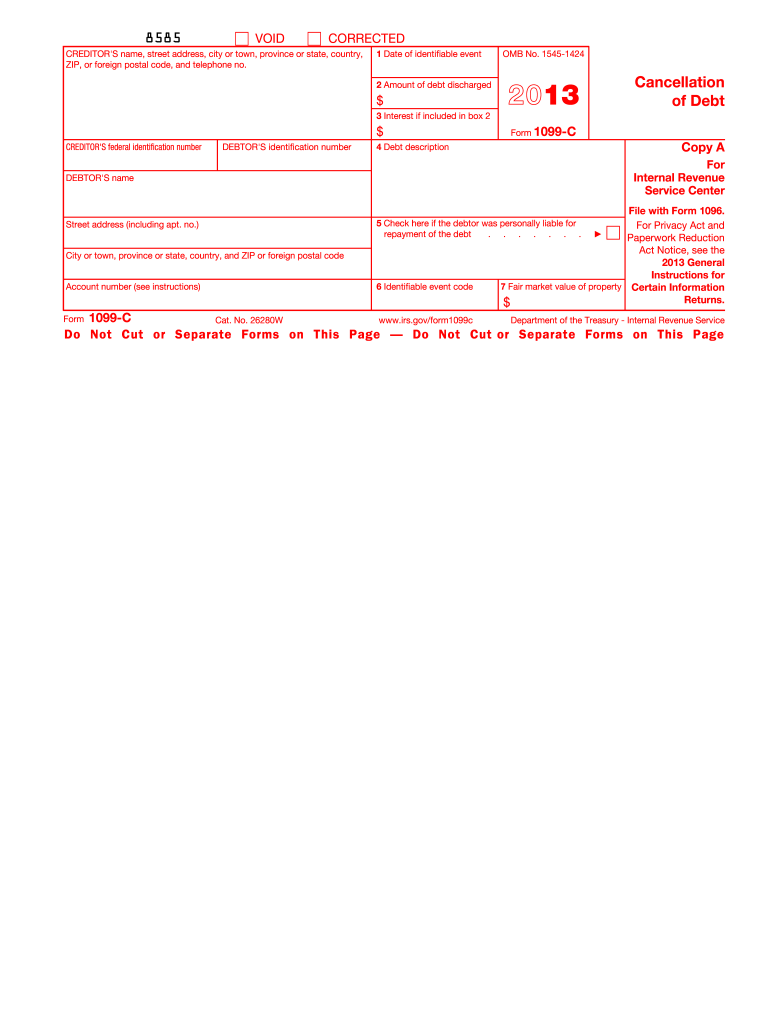

Key Elements of the 1099-C 2013 Form

- Identifying Information: Includes personal and creditor information necessary for reporting.

- Amount of Debt Canceled: The principal amount and any accrued interest canceled.

- Date of Cancelation: Specifies when the debt was forgiven, crucial for accurate reporting.

- Event Codes: Indicate the type of event that led to the cancelation, such as bankruptcy or settlement.

Penalties for Non-Compliance

Non-compliance with the 1099-C form requirements can result in penalties from the IRS. Failure to file, late filing, or inaccuracies on the form may incur fines. It is essential for taxpayers to submit accurate information to avoid these penalties, adhering strictly to form deadlines and guidelines.

Common Taxpayer Scenarios

Several scenarios warrant the use of the 1099-C form, including:

- Self-Employed Individuals: Who may have had business debts forgiven.

- Homeowners: Experiencing mortgage foreclosures or loan modifications.

- Students: Benefiting from canceled student loans under specific programs or agreements.

Software Compatibility

Tax filing software such as TurboTax and QuickBooks supports the 1099-C form, making it easier for taxpayers to include canceled debts in their returns. These programs guide users through the process of reporting forgiven debts, ensuring compliance with IRS rules and reducing filing errors.

Filing Deadlines and Important Dates

The 1099-C form must be mailed to the debtor by January 31 and filed with the IRS by the last day of February for paper submissions, or by March 31 when filing electronically. Meeting these deadlines is critical to avoid penalties and to ensure accurate tax reporting.

Examples of Using the 1099-C 2013 Form in Different Contexts

- Individual Debt Forgiveness: A credit card company forgives a portion of an unpaid balance, and the individual receives Form 1099-C.

- Business Debt Settlement: A small business negotiates a settlement with creditors forgiving part of their business debts, requiring the filing of a 1099-C.

- Mortgage Restructuring: Homeowners who have undergone a mortgage write-down or restructuring receive a 1099-C for the forgiven amount.

State-Specific Rules for the 1099-C 2013 Form

While the 1099-C is federally mandated, some states have additional rules that impact how forgiven debts are processed. For example, different states may have unique tax treatments or exclusions for certain types of debt forgiveness, such as those related to mortgage debts under state-specific relief programs.

By comprehensively understanding these aspects of the 1099-C form, taxpayers and businesses can ensure accurate tax filing, avoid legal pitfalls, and manage the financial implications of canceled debt effectively.