Understanding the Purpose of 2010 Form 1120 Schedule G

The 2010 Form 1120 Schedule G is an essential document required by the IRS for U.S. corporations to report information regarding entities, individuals, and estates that possess significant portions of the corporation's voting stock. This schedule applies to domestic corporations, excluding S corporations, that are required to file Form 1120. It ensures transparency in ownership, helping the IRS monitor and regulate corporate activities efficiently.

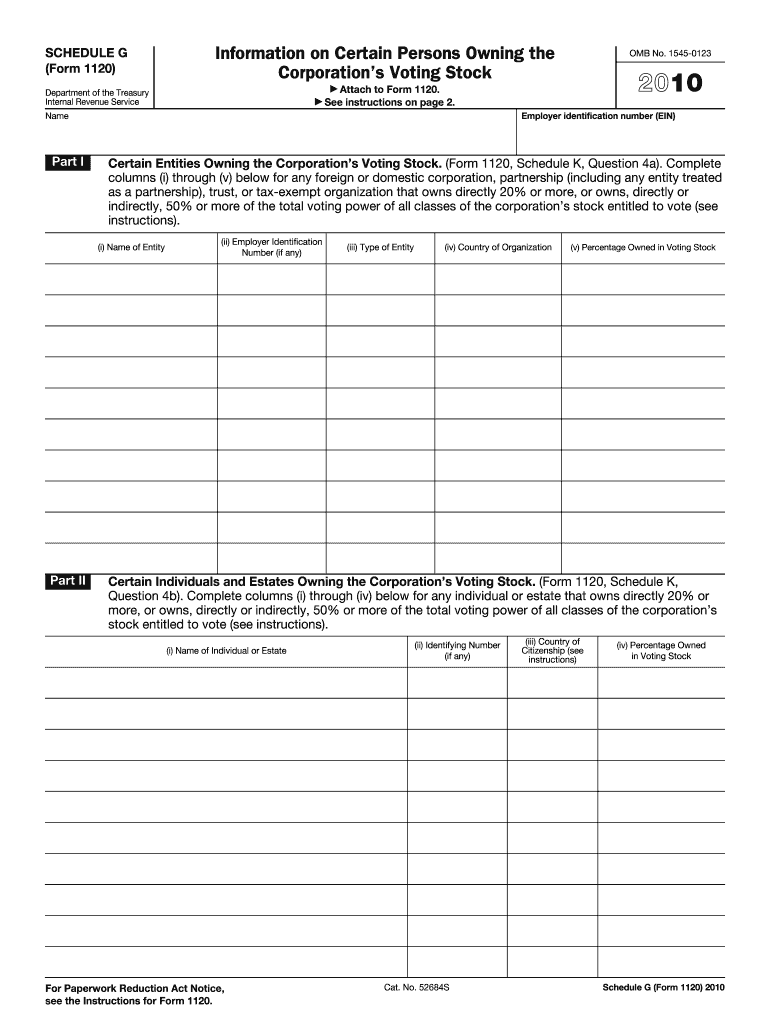

Parts of the Schedule

- Part I: Focuses on entities that own 20% or more of the voting power directly, or 50% or more indirectly.

- Part II: Concentrates on individuals or estates with similar ownership stakes.

Key Elements of 2010 Form 1120 Schedule G

Understanding the critical elements of the 2010 Form 1120 Schedule G can clarify the information required:

- Names and Addresses: Corporations must disclose the names and addresses of substantial stakeholders.

- Identification Numbers: Provides the taxpayer identification numbers for the entities or individuals listed.

- Type of Entity: Classifies if an entity is a corporation, partnership, individual, etc.

- Percentage Owned: Requires reporting the percentage of voting stock owned by the listed party.

- Countries of Organization: Lists the countries where entities or individuals are organized or hold citizenship.

How to Complete the 2010 Form 1120 Schedule G

- Gather the Necessary Information: Collect details about the corporation's significant shareholders, including addresses, identification numbers, and the type of entity.

- Fill Out Part I & II: Enter information on entities and individuals as required based on ownership percentages.

- Review for Accuracy: Ensure all entries are accurate and complete to avoid potential issues.

- Attach to Form 1120: Once completed, attach Schedule G to the corporation's annual return (Form 1120).

Digital vs. Paper Version of Schedule G

Corporations have the option to file Schedule G electronically or via paper:

- Digital Filing: Often preferred due to speed and efficiency. Many tax software programs support electronic filing, ensuring accurate calculations and format compliance.

- Paper Filing: Suitable for those more comfortable with traditional methods, requires mailing or delivering physical copies to the IRS.

Penalties for Non-Compliance

Non-compliance with the Schedule G filing requirements can lead to significant IRS penalties:

- Failure to File: Results in monetary penalties based on each omitted shareholder.

- Incorrect Information: Inaccuracies or omissions can lead to additional scrutiny, audits, and further penalties.

Eligibility Criteria for Filing

U.S. domestic corporations that file a Form 1120 return and have shareholders with substantial voting stock must submit the Schedule G. This excludes S corporations and certain other entities not obligated to file Form 1120.

IRS Guidelines for 2010 Form 1120 Schedule G

The IRS provides detailed instructions for completing the Schedule G, ensuring corporations accurately report pertinent information. Corporations must stay updated with IRS guidelines to avoid mistakes.

Compliance Tips

- Stay Updated: Regularly check for IRS updates or changes in form instructions.

- Use IRS Resources: Consult the IRS website or forms instruction booklets for specific guidance.

Required Documentation for Filing

Corporations must include additional documentation when filing Schedule G:

- Shareholder Documentation: Proof of shareholder percentages and identification numbers.

- Corporate Records: Documents verifying organizational structure and ownership details.

Role of Schedule G in Corporate Transparency

The Schedule G enhances corporate transparency by providing the IRS with detailed ownership information. It helps ensure proper reporting and oversight, deterring fraudulent or deceitful financial activities within corporations.

Examples of Form Use

- Mergers and Acquisitions: Corporations undergoing mergers or acquisitions might exhibit substantial changes in ownership requiring updated Schedule G submissions.

- International Corporations: Entities with foreign stakeholders must accurately report these relationships to comply with U.S. laws.

By meticulously completing and submitting the 2010 Form 1120 Schedule G, corporations can ensure adherence to IRS requirements, minimizing potential risk of penalties or audits.