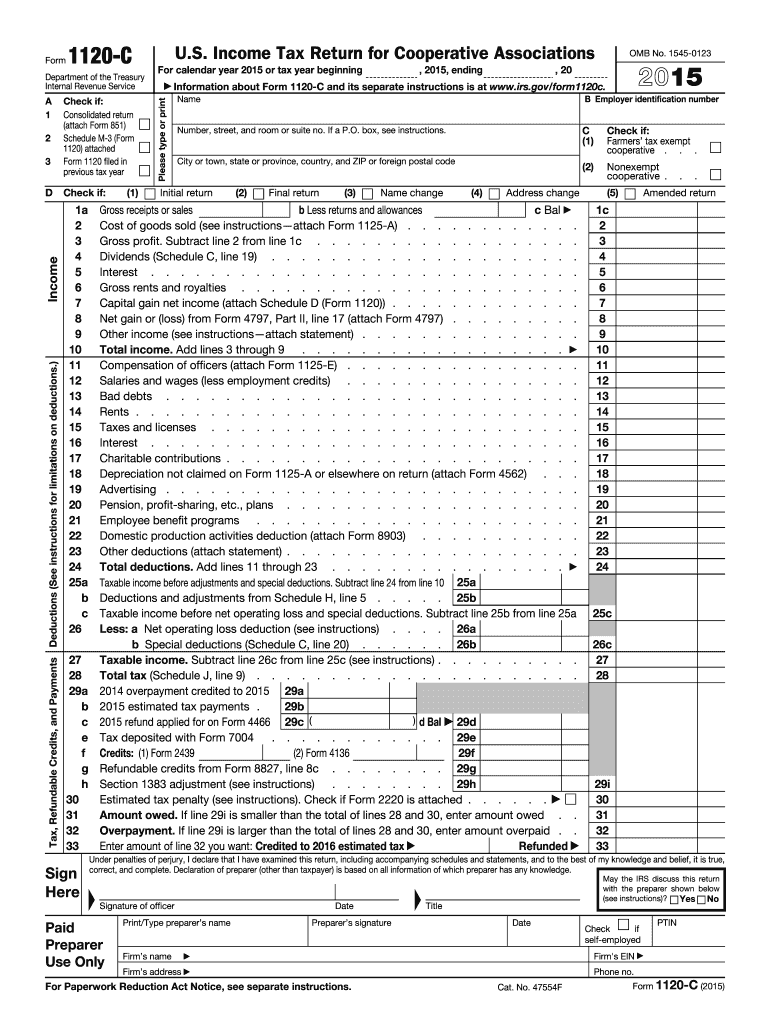

Definition and Purpose of Form 1120-C

Form 1120-C, known as the U.S. Income Tax Return for Cooperative Associations, is specifically designed for cooperative associations to report their annual income, deductions, and credits. The form encompasses a variety of sections, detailing gross receipts, the cost of goods sold, and taxable income calculations. Cooperative associations use this form to declare their financial activities for the tax year 2015, complying with IRS regulations. The completion of Form 1120-C helps ensure accurate reporting and determination of tax obligations, aligning with the cooperative's unique tax structure.

Key Sections of Form 1120-C

- Gross Receipts: Encompasses total income from sales and services.

- Cost of Goods Sold: Details direct costs attributable to the production of goods sold by the cooperative.

- Taxable Income Calculations: Computes the income subject to tax after deductions.

- Schedules for Dividends and Patronage Income: Reports any dividends or income distributed to members.

How to Use the 2015 Form 1120-C

Filing Form 1120-C involves a structured process to ensure all financial aspects of the cooperative are accurately reported. To complete the form, cooperatives must gather precise financial information and address different sections as required. Here’s a breakdown of how to navigate the form:

- Gather Financial Records: Collect all income, expenditure, and capital details.

- Complete Basic Information: Fill in the cooperative's name, address, and employer identification number.

- Calculate Gross Income: Document all financial transactions contributing to gross receipts.

- Determine Deductions: Itemize deductions applicable under IRS regulations.

- Summarize Taxed Income: Compute the taxable income by subtracting deductions from gross receipts.

Detailed Instructions

- Financial Record Preparation: Ensure all receipts and records are accurate and comprehensive.

- Check Deductions: Verify that all claimed deductions are legitimate and supported by documents.

- Review Submission Guidelines: Follow IRS guidelines for accurate and timely filing.

Steps to Complete the 2015 Form 1120-C

The preparation of Form 1120-C requires methodical steps to ensure completeness and accuracy. These steps outline how cooperative associations can correctly file their tax return:

- Pre-Filing Preparation: Assemble all relevant financial documents and ensure records are up-to-date.

- Enter Organizational Details: Start by filling out the cooperative's identifying information.

- Record Financial Transactions: Itemize and sum up income, expenses, and other financial activities.

- Calculate Tax Liability: Use the form's worksheet to determine the amount of tax owed or refundable.

- Review and Validate Entries: Double-check all figures and calculations made on the form.

- Submit the Form to the IRS: File by post or electronically, following IRS submission guidelines.

Common Mistakes and Tips

- Accurate Data Entry: Ensure all dollar amounts and data points are entered accurately.

- Validation: Perform a final review of the form for any unnoticed discrepancies.

- Keep Copies: Retain a copy of the completed form and all supporting documents for future reference.

Eligibility and Usage Criteria for Form 1120-C

The Form 1120-C must be filed by cooperative associations that engage in business in the U.S. and meet specific tax criteria. Eligibility is determined by factors such as the type of business and filing status. Cooperatives owned by members who use its goods or services typically need to file this form. Understanding these parameters helps in determining if a cooperative must comply by utilizing Form 1120-C.

Primary Eligibility Requirements

- Member-Owned Organizations: Must be organized under cooperative principles.

- Income Thresholds: Both federal and state income limits may influence filing requirements.

- Business Activity Type: Engaging in transactions that qualify as cooperative activities.

IRS Guidelines and Compliance for Form 1120-C

The IRS provides guidelines that outline how cooperative associations need to file Form 1120-C. Compliance with these instructions ensures the cooperative is adhering to federal tax laws. The comprehensive guidelines delineate the types of income to report, deductible expenses, and other tax-related obligations specific to cooperatives.

Filing Compliance Measures

- Timely Submission: Must be filed by the 15th day of the 9th month after the end of the cooperative’s tax year.

- Accurate Reporting: All calculations and reported amounts must comply with IRS rules to avoid penalties.

Filing Deadlines and Important 2015 Dates

For the 2015 tax year, it is critical to adhere to the deadline for filing Form 1120-C. Missing these key dates can result in penalties, adding unnecessary financial burden on the cooperative. Knowing the deadlines also ensures that the cooperative can organize and file all necessary paperwork in advance.

Critical Dates

- Filing Deadline: Typically the 15th of September following the end of the fiscal year.

- Extension Requests: If needed, requests for additional time should be submitted before the deadline.

Required Documents for Completing Form 1120-C

When preparing Form 1120-C, specific documents are necessary to ensure the accuracy and compliance of financial reporting. These documents provide the basis for calculations and entries made on the form, serving as proof of financial transactions.

List of Essential Documents

- Financial Statements: Annual income statements and balance sheets.

- Receipts and Invoices: Proof of income and expenditures.

- Membership Records: Details regarding member dividends and distributions.

Penalties for Non-Compliance with Form 1120-C Requirements

Cooperatives that fail to comply with IRS requirements when filing Form 1120-C may face penalties. These can include financial fines for late submissions or inaccuracies in reported information. Understanding these penalties encourages accurate and timely filing by cooperative associations.

Key Penalties

- Late Filing Fees: Charges accrued for missing the stated filing deadline.

- Errors or Omissions: Financial penalties applied for incorrect or missing data on the form.