Definition & Meaning

Taxable income before adjustments and special deductions refers to the amount of a taxpayer's income that is subject to certain federal taxes before applying any deductions or specific financial adjustments. It is a critical figure in tax calculations for individuals and businesses, as it forms the basis upon which applicable taxes are computed. This total is derived from gross income after certain allowable subtractions like health savings account contributions and alimony payments, but before more specific deductions are applied. Understanding this term is crucial for accurate filing and compliance with IRS regulations and entails identifying income sources such as wages, dividends, rental income, and other forms of earnings that qualify for taxation.

Key Components of Taxable Income

- Wages and Salaries: Includes all compensations for services, whether paid hourly or salaried.

- Dividends and Interest: Income earned from investments must be accounted for.

- Business Revenue: Gross income reported by business entities before expenses.

- Rental Income: Proceeds from property rented to others form part of this income.

- Retirement Income: Certain pensions and annuities are included.

How to Use the Taxable Income Before Adjustments and Special Deductions

Properly leveraging taxable income before adjustments and special deductions helps in legally minimizing tax liabilities while ensuring accurate tax reporting. Taxpayers usually start with this figure to understand their tax obligations before seeking applicable deductions and credits. An accurate calculation is mandatory for:

- Filing Federal Tax Returns: Use this figure to determine what taxable income needs to be reported.

- Planning Tax Strategies: Identifying opportunities for deductions helps in reducing the overall tax payable.

- Evaluating Financial Health: Determine potential cash flow by anticipating tax outflows.

Application of Information

- Financial Planning: Use insight to adjust income strategies throughout the fiscal year.

- Tax Accounting: Employ as a baseline for detailed tax computations and future planning.

Steps to Complete the Taxable Income Before Adjustments and Special Deductions

Filing federal tax returns requires an understanding of the steps involved in arriving at your taxable income before adjustments and special deductions:

- Gather Income Documents: Collect W-2s, 1099s, and investment income statements.

- Calculate Gross Income: Sum all income sources including wages, interest, and business profits.

- Identify Adjustments: Look for IRS-sanctioned adjustments such as IRA contributions or student loan interest.

- Determine Preliminary Taxable Income: Subtract adjustments from the total gross income.

- Review for Accuracy: Double-check all figures to ensure that nothing is missing or misstated.

Practical Considerations

- Use Financial Software: Programs like TurboTax facilitate accurate computations by automating many of these steps.

- Consult Tax Professionals: For complex situations, involving experts might mitigate errors.

IRS Guidelines

The IRS provides specific guidance on what constitutes taxable income and the permissible adjustments and deductions. These guidelines are essential in the preparation and submission of accurate tax returns:

- Publication 17: Offers comprehensive advice on income types, adjustments, and credits.

- Form 1040 Instructions: Detailed steps for calculating taxable income.

- Online Resources: The IRS website features online tools for taxpayers to determine allowable adjustments.

Considerations for Compliance

- Stay Updated on Changes: Tax laws evolve frequently; ensure you adhere to the most current guidelines.

- Verify Income Categories: Misclasifying income might lead to penalties or unnecessary audits.

Filing Deadlines / Important Dates

Taxpayers need to be aware of critical deadlines for federal tax returns in the United States, including:

- April 15: Traditional deadline for filing individual tax returns (Form 1040).

- October 15: Extended deadline if you apply for an extension.

- Quarterly Estimated Taxes Due: For certain self-employed or business entities.

Impact of Missing Deadlines

- Late Filing Penalties: Interest and penalties accrue on unpaid taxes from the due date.

- Impact on Credit Ratings: Financial repercussions extend beyond immediate penalties.

Penalties for Non-Compliance

Failing to accurately report taxable income before adjustments and special deductions or missing filing deadlines may result in the following repercussions:

- Accuracy-Related Penalties: Misreporting income can accrue penalties up to 20% of the unpaid amount.

- Failure-to-File Penalty: Charged at 5% of unpaid taxes per month, up to 25%.

- Criminal Charges: Deliberately falsifying returns could lead to serious legal action.

Prevention Strategies

- Automate Reminders: Use calendar tools to keep track of deadlines.

- Regular Consultations: Involve tax consultants periodically to review compliance.

Business Entity Types (LLC, Corp, Partnership)

Different business structures have unique considerations for taxable income before adjustments and special deductions:

- LLCs: Generally pass income through to owners, making personal tax returns vital in accounting.

- Corporations: File on distinct Form 1120, reporting corporate earnings and related deductions.

- Partnerships: Must report income while allowing partners to apply personal deductions.

Specific Filing Needs

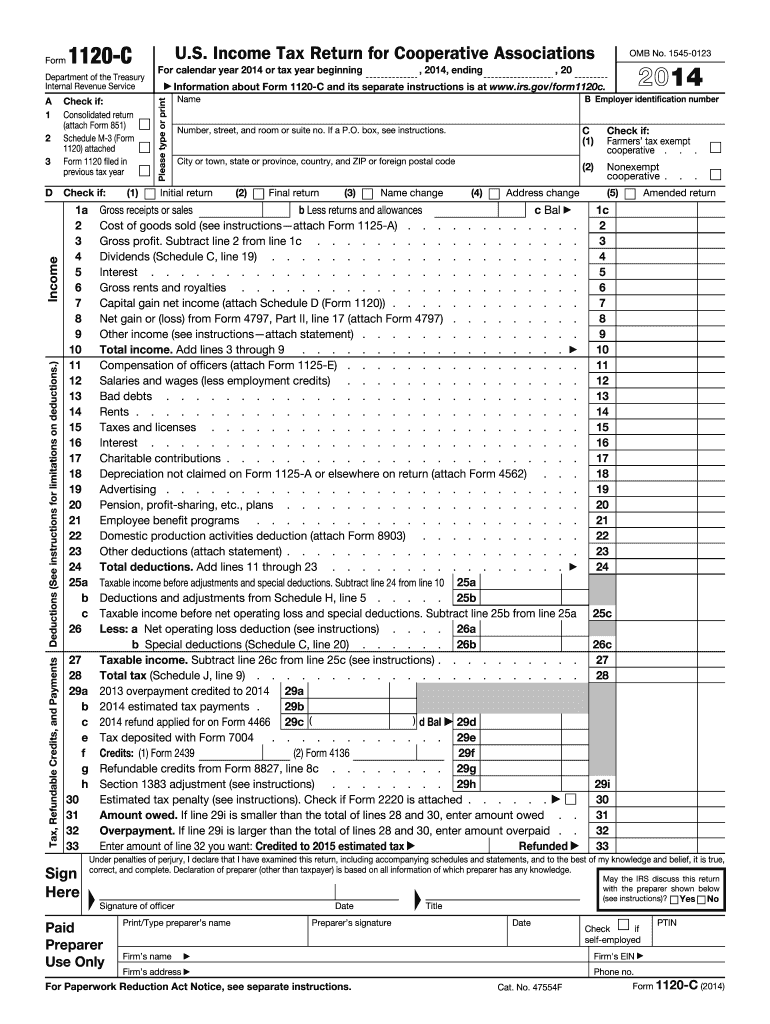

- Separate Forms: Certain entities require specialized forms, like 1120-C, for cooperatives.

- Entity-Specific Deductions: Some business forms allow for unique adjustments to income.

Taxpayer Scenarios (Self-Employed, Retired, Students)

Different taxpayer profiles handle taxable income and deductions in unique ways, depending on their financial situation:

- Self-Employed Individuals: Pay estimated quarterly taxes on income instead of deductions at year-end.

- Retired Persons: Manage supplemental income from pensions while adjusting for retirement-related deductions.

- Students: Utilize education-related credits and deductions, affecting taxable income calculations.

Consideration for Diverse Needs

- Tailored Strategies: Adapting tax approaches based on personal circumstances significantly shifts outcomes.

- Resource Availability: Access IRS tools designed for specific scenarios, promoting informed financial decisions.