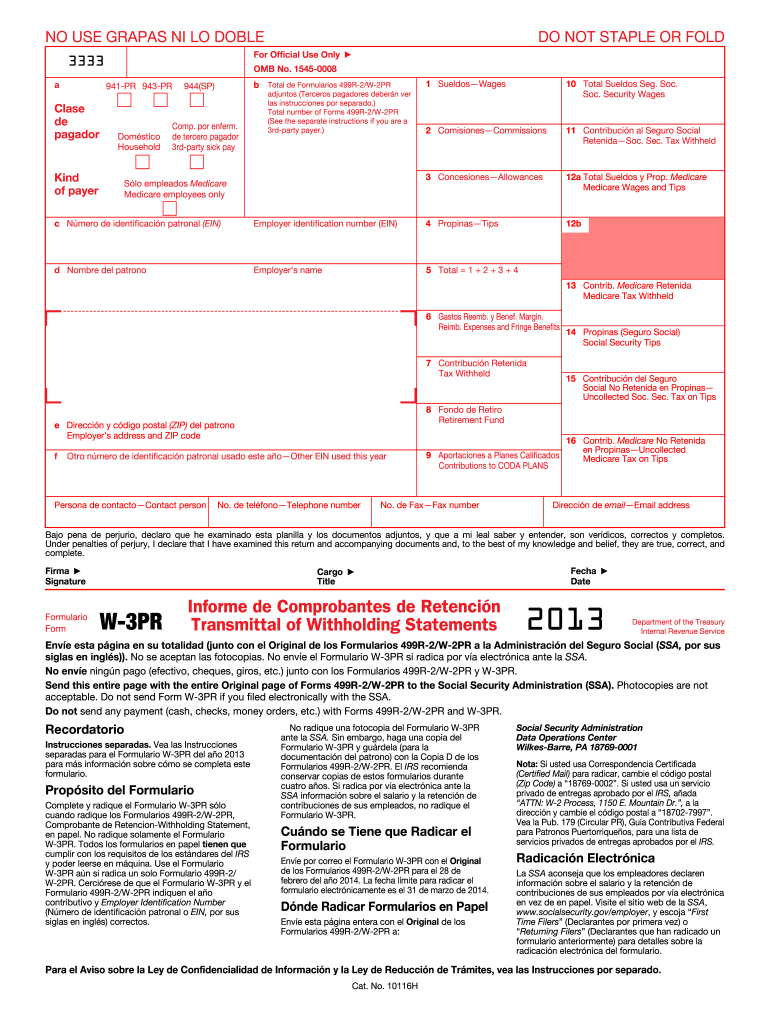

Definition & Meaning

The "8 Fondo de Retiro" is a document related to retirement funds, which is primarily used for documenting financial contributions, benefits, or requirements associated with retirement accounts. This form is essential in managing retirement funds and ensuring compliance with legal and financial regulations. Understanding its purpose and how it functions within retirement planning is crucial for individuals and organizations utilizing retirement funds.

- Retirement Fund Documentation: The form serves to record details about contributions and withdrawals, ensuring transparency and accuracy in managing retirement accounts.

- Compliance and Regulations: It ensures that retirement fund activities comply with relevant financial regulations and legal requirements, safeguarding both contributors and recipients.

Key Elements of the 8 Fondo de Retiro

The form consists of several critical components that must be understood in detail to complete it accurately. Each section of the form provides specific information required for processing and managing retirement funds.

- Contributor Information: This section requires personal details of the individual contributing to the fund, including name, identification number, and contact details.

- Financial Details: Detailed inputs regarding the financial transactions associated with retirement contributions, such as amounts, dates, and types of contributions, are necessary.

- Beneficiary Information: This involves specifying the beneficiaries who are entitled to receive benefits from the retirement fund, ensuring clarity in fund allocation.

How to Obtain the 8 Fondo de Retiro

Obtaining the "8 Fondo de Retiro" form can involve several steps, depending on your circumstances and the specific regulations governing retirement funds in your jurisdiction.

- Contacting Financial Institutions: Reach out to banks or financial institutions that manage retirement plans to request the form.

- Online Accessibility: Some organizations may offer the form for download from their website, providing easy access for users.

- Employment Sources: Employers may distribute the form directly to their employees, especially if they manage retirement funds as part of employment benefits.

How to Use the 8 Fondo de Retiro

Once you have the "8 Fondo de Retiro" form, understanding how to complete and use it effectively is essential. The form requires careful attention to detail in several areas.

- Accurate Information Entry: Ensure that all data entered, especially regarding financial contributions and beneficiary information, is accurate and up-to-date.

- Regular Updates: Maintain and regularly update the form to reflect any changes in contributions or beneficiary information.

- Document Submission: Know the correct procedure for submitting the form, whether through electronic means or postal services, depending on institutional requirements.

Steps to Complete the 8 Fondo de Retiro

Filling out the "8 Fondo de Retiro" form involves a structured approach to ensure completeness and compliance with applicable standards.

- Gather Required Information: Collect all necessary personal, financial, and beneficiary details before starting the form.

- Fill Out Sections Sequentially: Start with personal information, then proceed to financial contribution details, and finalize with beneficiary information.

- Review and Verify Entries: Cross-check all entries for accuracy to prevent errors that could affect fund management.

- Submit the Form: Follow institutional guidelines to submit the form, keeping a copy for your records.

Who Typically Uses the 8 Fondo de Retiro

The form is commonly utilized by various individuals and entities involved in retirement planning and fund management.

- Individuals Planning for Retirement: Those contributing to retirement accounts need to use this form to document their savings and plans.

- Financial Advisors: Professionals who assist clients in managing and optimizing their retirement funds rely on this form to ensure alignment with financial goals.

- Employers with Retirement Benefits: Companies offering retirement plans as part of employee benefits use this form to facilitate contributions and manage employee benefits efficiently.

Legal Use of the 8 Fondo de Retiro

Understanding the legal implications and requirements associated with the "8 Fondo de Retiro" is crucial for ensuring compliance and proper management of retirement funds.

- Compliance with Financial Regulations: The form must be completed in adherence to relevant financial laws and regulations to ensure legal protection for both the contributor and the beneficiary.

- Documenting Legal Entitlements: Proper use of the form documents the legal rights of beneficiaries, preventing disputes over fund distribution.

Eligibility Criteria

Certain criteria determine who can utilize the "8 Fondo de Retiro" effectively, ensuring that only qualified individuals and entities engage with retirement fund processes.

- Age and Employment Status: Often, individuals nearing retirement age or those actively employed are the primary users of this form.

- Contributing Parties: Eligibility may also depend on being part of a financial plan or institution that offers retirement fund management services.

Important Terms Related to 8 Fondo de Retiro

Familiarizing oneself with terms associated with the "8 Fondo de Retiro" enhances understanding and ensures accurate form completion.

- Principal Amount: The initial amount of money invested or contributed to the retirement fund.

- Beneficiary Designation: The process of naming individuals who will receive benefits from the fund.

- Contribution Limit: The maximum amount that can be contributed to a retirement fund annually, as stipulated by financial regulations.