Definition and Meaning

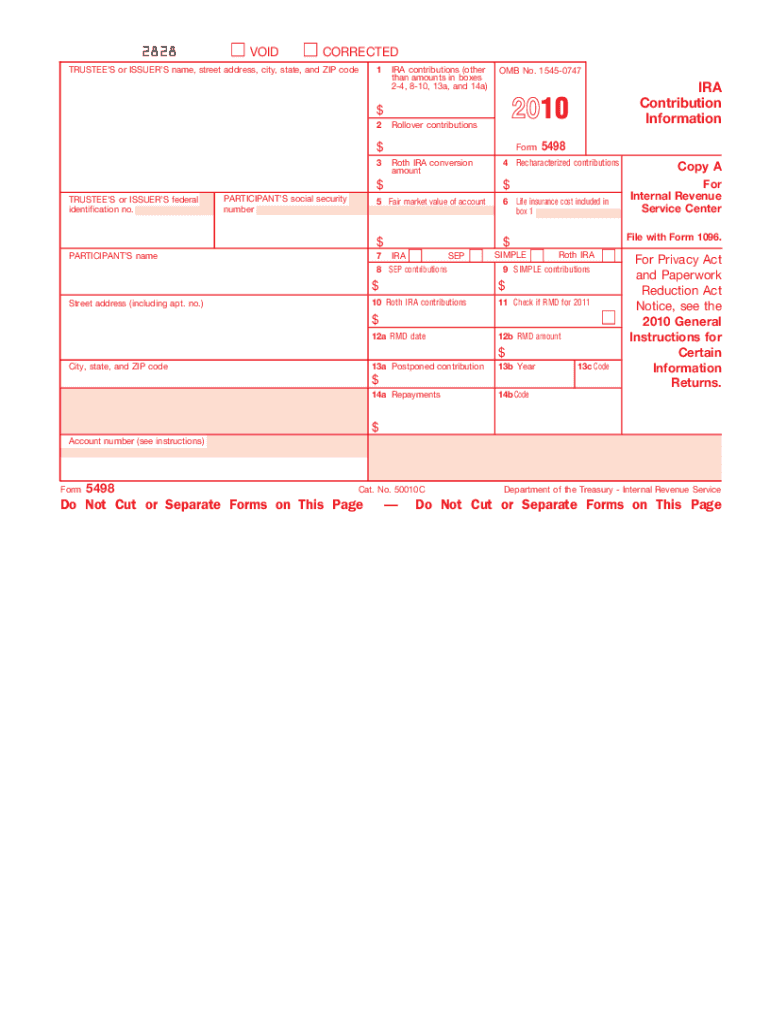

Form 5498, specifically the 2010 version, is a tax document used by the Internal Revenue Service (IRS) to report contributions made to individual retirement arrangements (IRAs) throughout the tax year. This form plays a critical role in ensuring that taxpayers accurately report their retirement account activities, including contributions, rollovers, and fair market value, to the IRS. It is primarily used by financial institutions to notify the IRS of the contributions made to an individual's IRA, thus aiding in tax compliance and transparency.

How to Use the 2 Form

Understanding how to use the 2 Form is essential for both taxpayers and trustees who are involved in managing IRAs. The form is not filed by individuals directly but is furnished by the trustee or custodian of the IRA. Taxpayers should use the information provided on the form to confirm their contributions to traditional, SEP, or SIMPLE IRAs and ensure these align with their own records. It's also used to verify the amounts reported on your federal tax return regarding IRA contributions, rollovers, and conversions from other types of retirement plans.

Steps to Complete the 2 Form

-

Information Verification:

- Ensure that the personal information, such as your name and Social Security number, is correct.

-

Contribution Reporting:

- Confirm that the amounts listed for various contribution types, including regular, rollover, and conversion amounts, are accurate.

-

Fair Market Value:

- Check the fair market value of the account, listed in Box 5, which gives an overview of the account's performance and balance at the end of the year.

-

Minimum Distribution:

- If applicable, review the Required Minimum Distribution (RMD) information indicated on the form.

-

Submission:

- Trustees and custodians submit the form to the IRS and a copy to the taxpayer. Taxpayers use the form for record-keeping and tax return filing purposes.

Important Terms Related to 2 Form

-

Traditional IRA: An individual retirement account allowing pre-tax contributions. Taxes are paid on withdrawals in retirement.

-

SEP IRA: A Simplified Employee Pension plan allowing employers to contribute to traditional IRAs set up for employees.

-

SIMPLE IRA: Savings Incentive Match Plan for Employees, often chosen by small businesses for simpler and lesser-cost retirement plans.

-

Rollover: The process of transferring funds from one retirement account to another without taxes or penalties.

-

Fair Market Value: Refers to the market value of the IRA at the end of the calendar year.

Legal Use of the 2 Form

The 2 Form is legally mandated for IRA trustees and custodians to furnish both to the IRS and the individual holding the IRA. This form is in compliance with U.S. tax laws requiring complete and accurate reporting of retirement contributions for tax assessment purposes. Failing to submit or provide accurate information on this form can lead to penalties both for the financial institution and the account holder.

Who Typically Uses the 2 Form

Form 5498 is predominantly used by financial institutions responsible for managing IRAs to report specific retirement-related contributions and transactions to the IRS. It is also used by individual taxpayers who have IRAs, to ensure that their annual contributions and the fair market value of their accounts are accurately reflected and reported for tax purposes.

IRS Guidelines for the 2 Form

The IRS outlines strict guidelines for the completion and submission of the 2 Form. Financial institutions must ensure the form is issued to the individual taxpayer by the May 31 deadline following the reporting year. The IRS requires accuracy in the amounts reported, including annual contributions and the fair market value, to ensure proper tax regulation compliance.

Penalties for Non-Compliance

Failure to comply with the IRS requirements for the 5498 Form can result in penalties. Institutions that do not provide this form in a timely manner or do not report accurate information may face fines. For individuals, erroneous reporting can lead to discrepancies in tax returns, potential audits, and subsequent fines if contributions are not reported accurately. Proper filing is crucial to avoid these repercussions.