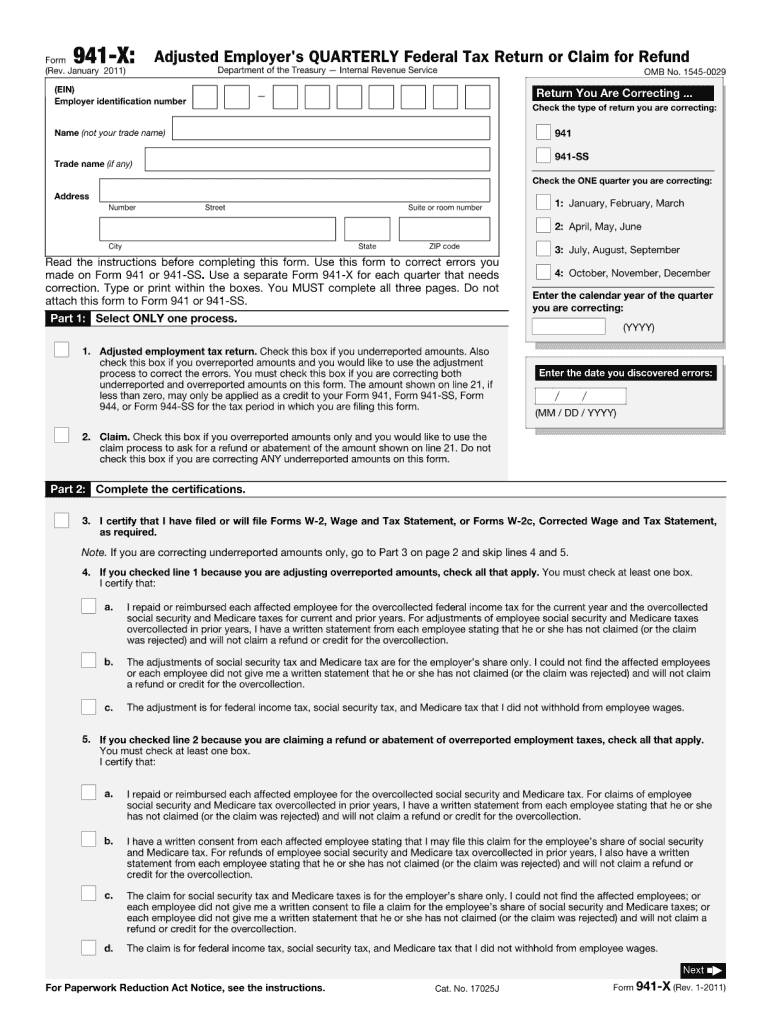

Definition and Purpose of the 2011 941-X Form

The 2011 941-X form is used by employers to correct errors on previously filed Forms 941, the employer's quarterly federal tax return. This form allows businesses to report adjustments for underreported or overreported federal payroll taxes from a specific quarter in the year 2011. The form is crucial for ensuring that an employer's tax filings are accurate and up-to-date, which can help avoid potential penalties and interest due to discrepancies.

Reasons for Using Form 941-X

Employers primarily use Form 941-X to adjust errors related to wages, tips, taxes withheld, and other tax credits reported on the original 941 form. Common corrections include amending miscalculations in Social Security, Medicare taxes, and tax deposits. Utilizing this form can ensure compliance with IRS regulations by rectifying discrepancies in payroll tax reporting.

How to Obtain the 2011 941-X Form

The 2011 941-X form can be obtained directly from the IRS website. Employers may also order a copy through the mail by contacting the IRS. However, since this form relates to a specific tax year, it might be necessary to check for any updates or changes that could influence how you report adjustments. Always ensure that you are using the correct version of the form by verifying the year at the top of the document.

Online Availability

- The form is available for download in PDF format.

- Instructions for the form can be downloaded as a separate document to ensure accurate completion.

Steps to Complete the 2011 941-X Form

-

Gather Necessary Information: Before starting, collect the original Form 941 and any backup documentation that substantiates the corrections you intend to make.

-

Complete Part 1: Indicate the quarter of the 941 form you are correcting, and provide the year and the employer’s EIN (Employer Identification Number).

-

Revise Tax Information in Part 2: Calculate the corrected amounts for every line item that requires adjustment. This section includes detailed line-by-line adjustments.

-

Justify Corrections in Part 3: Provide a detailed explanation of each correction, including the nature of the error and the reason for the revision.

-

Sign and Date the Form: The person responsible for the correction must provide their signature and the date.

-

Submit the Form: Mail the completed form to the IRS at the address designated for your location as specified in the form’s instructions.

Key Elements of the 2011 941-X Form

The form is structured to capture specific details required for corrections:

- Page Layout and Sections: Divided into multiple parts, each targeting different corrective actions.

- Parts and Lines: Detailed areas for illustrating correct figures and adjustments.

Who Typically Uses the 2011 941-X Form

This form is used by employers and business entities that have realized errors in payroll reporting for the year 2011. Employers across various sectors, including corporations, partnerships, and sole proprietorships, utilize this form to amend their federal tax returns.

Business Entity Types

- Corporations (C Corporations, S Corporations)

- Partnerships

- Limited Liability Companies (LLCs)

- Sole Proprietors

IRS Guidelines and Compliance

The IRS provides specific guidelines on how to file this form correctly. It's essential to adhere to these instructions to prevent any issues with processing. The IRS expects:

- Timely Corrections: Immediate submission once an error is discovered.

- Supporting Documentation: Provide sufficient evidence to justify corrections.

Filing Deadlines and Important Dates

While there is no hard filing deadline for Form 941-X, employers should file as soon as an error is detected. The form must be filed within three years of the original return date or within two years of the date the tax was paid, whichever is later, to claim a refund or an abatement.

Important Considerations

- Avoid Delays: Submissions beyond the timeframe may not be processed for a refund.

- Compliance Dates: Awareness of filing periods remains critical.

Penalties for Non-Compliance

Failure to file Form 941-X in a timely manner can lead to penalties. The IRS may impose penalties for underpayment of taxes if discrepancies are not rectified. Ensuring timely and accurate submission mitigates the risk of financial penalties and interest.