Definition and Meaning

The "Request for Extension of Time To File Information Returns" is an official IRS form, specifically known as Form 8809. This form allows businesses and individuals to request an additional 30 days to file certain information returns with the IRS. These information returns can include various forms like the W-2, 1099, and others. The extension is not automatically granted; the filer must meet specific eligibility criteria and properly submit the form to be considered for an extension.

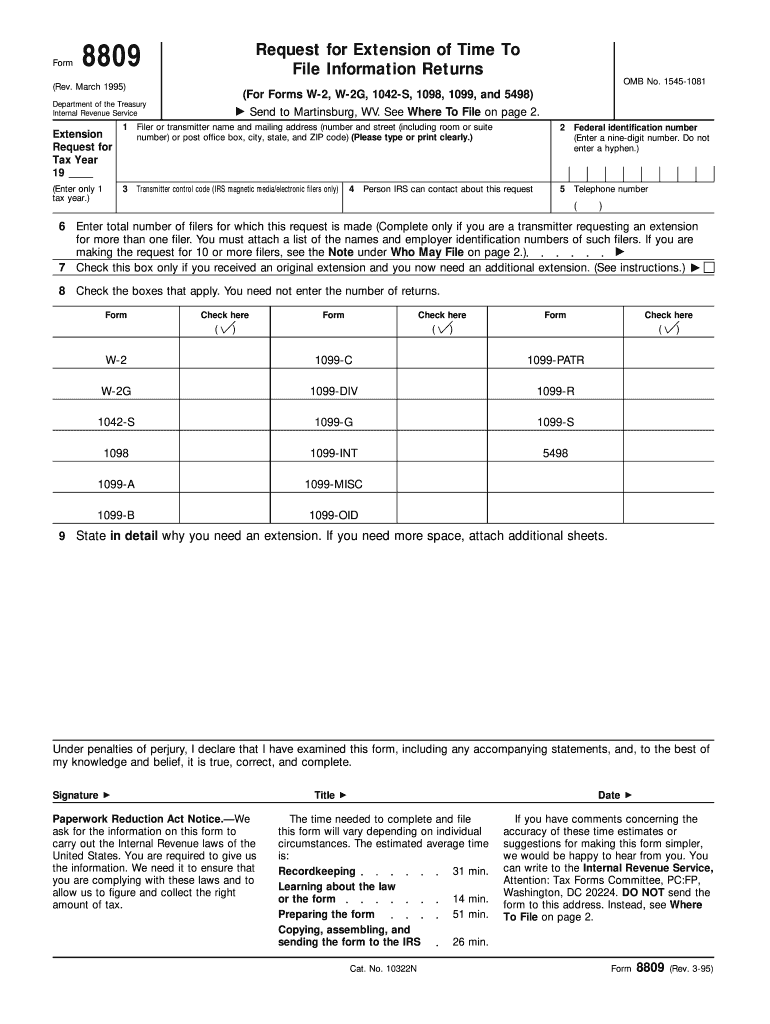

How to Use the Request for Extension of Time To File Information Returns

To effectively use Form 8809, filers need to follow a structured process. Initially, assess which information returns require an extension. The form should detail each return type for which an extension is sought. It is essential to provide accurate and complete information, including the type of filer, whether it is a business or individual, and specify the forms subjected to the extension request. Timeliness is crucial; hence, submit the form before the original due date of the returns that need extensions.

Steps to Complete Form 8809

- Gather Necessary Information: Know which returns you need an extension for, the taxpayer identification number, and other relevant details.

- Complete Part I: Fill in basic information, including the filer’s name, TIN, and address.

- Fill in Details on Part II: List the specific returns for which the extension is requested.

- Sign and Date the Form: This essential step validates the request.

- Submit via Preferred Method: Choose whether to file the form electronically or via mail, ensuring it's submitted before the filing deadline.

Filing Deadlines and Important Dates

The Form 8809 must be submitted before the deadline of the respective information return for which an extension is being requested. For returns like the W-2 and various 1099 forms, this typically aligns with January 31st. Failure to file the extension request before the deadline can result in penalties and the inability to receive the desired extension.

Eligibility Criteria

Eligibility for utilizing Form 8809 extends to any business or individual required to file information returns with the IRS. The request is suitable for both original filers and those needing an extension for corrections. However, only one extension per return type is allowable per tax year. In some instances, particularly for large employers or certain types of returns, additional documentation may be needed to justify the need for an extension.

Methods to Obtain Form 8809

Form 8809 can be accessed in several ways. It's readily available for download on the IRS website, ensuring secure and direct access to the latest form version. Additionally, various tax preparation software might integrate the capability to create and submit Form 8809 directly. Tax practitioners may also provide physical copies or assistance with the electronic submission process.

Penalties for Non-Compliance

Failing to file information returns or seek necessary extensions can lead to significant IRS-imposed penalties. These penalties vary based on how late the return is filed, ranging from $50 to $550 per return, based on compliance timelines and organization size. Accurate and timely filing, including the submission of Form 8809 when applicable, is vital to avoid these financial repercussions.

Examples of Using the Request for Extension of Time To File Information Returns

Consider a mid-size corporation needing additional time to gather complete data for its 1099 forms. By submitting Form 8809, the corporation can secure an extra 30 days to compile accurate information, ensuring compliance and reducing the risk of penalties. Similarly, a small business owner awaiting documentation from independent contractors can benefit from requesting an extension, allowing for more precise reporting.

Summary of the Application Process and Approval Time

Upon identifying the need for an extension and completing Form 8809, submit the form electronically for the fastest processing time. Approval may be immediate via electronic submission, though mailed submissions can be processed within a few weeks. It is important to note that the IRS does not require filers to await acknowledgment as the extension is generally granted unless notified otherwise.