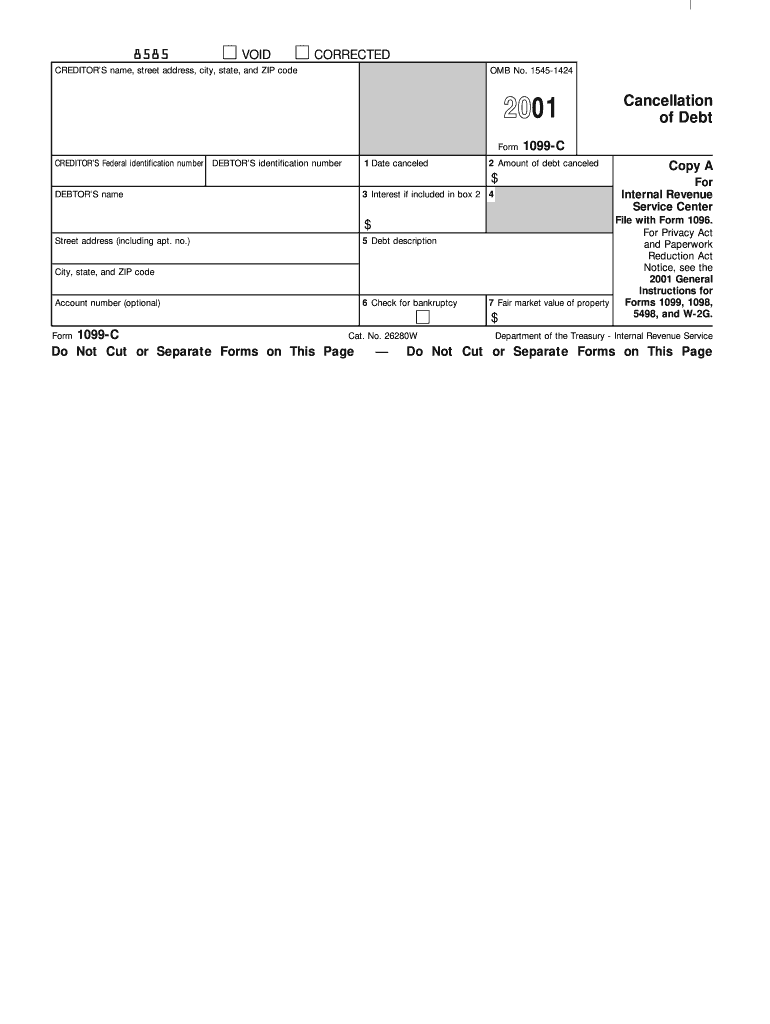

Definition & Purpose of Form 1099-C

The 2001 Form 1099-C is a critical document used for reporting the cancellation of a debt to the IRS. This form is essential for creditors who cancel debts of $600 or more, as it helps both the IRS and the debtor track potentially taxable income. When a debt is forgiven, reduced, or canceled, it can result in what is known as "cancellation of debt" (COD) income. Understanding the implications of this form is vital because COD income is typically taxable, although there are specific exceptions, such as bankruptcy or insolvency, where it might not be considered taxable.

- Reporting Canceled Debt: Creditors must accurately detail the debtor, the amount forgiven, and the date of cancellation.

- Legal Requirement: Law mandates that creditors provide this form to both the debtor and the IRS to ensure transparency and compliance.

How to Use Form 1099-C

Using Form 1099-C involves understanding both the reporting process for creditors and the tax implications for debtors.

-

For Creditors:

- Collect debtor details including name, address, and Taxpayer Identification Number (TIN).

- Specify the exact amount of debt canceled and provide the date of cancellation.

- Ensure all completed forms are sent to both the IRS and the debtors by the due date.

-

For Debtors:

- Review the form for accuracy.

- Attach the form to your tax return if required, depending on whether the cancellation leads to taxable income.

Steps to Complete the Form

Completing the 2001 Form 1099-C correctly ensures compliance and avoids potential IRS issues.

- Obtain the Form: Available on the IRS website or through tax preparation software.

- Fill Out Part I: Enter the creditor's details, including name, address, and TIN.

- Fill Out Part II: Provide the debtor’s information and details of the debt including description and amount.

- Review and Submit: Proofread for errors and submit to the IRS and the debtor.

Important Terms Related to Form 1099-C

Understanding the terminology associated with Form 1099-C aids in its accurate completion and comprehension.

- Cancellation of Debt (COD): The forgiveness or cancellation of a debt obligation.

- Insolvency: A condition where a debtor's liabilities exceed their assets, potentially exempting them from reporting canceled debt as income.

- 1099-C Income: The income reported due to debt cancellation, which might be taxable.

Who Typically Uses Form 1099-C

Form 1099-C is used by various entities under specific circumstances:

- Creditors: Including banks, loan agencies, and credit card companies, are common issuers of this form when they write off debts.

- Debtors: Individuals and businesses that have had a debt forgiven must consider the impact of the form for tax purposes.

Legal Use of Form 1099-C

The legal implications of Form 1099-C are significant, particularly in ensuring compliance with IRS tax laws.

- Tax Reporting: Ensures accurate reporting of potential taxable income resulting from canceled debts.

- Exemptions: Situations like bankruptcy or insolvency, when properly documented, may exempt debtors from taxation on canceled debt.

IRS Guidelines

The IRS provides specific guidelines on the use, submission, and reporting of Form 1099-C:

- Submission Deadline: Usually due by January 31st to the debtor and February 28th or March 31st (if filing electronically) to the IRS.

- Filing Methods: Forms can be submitted electronically or via traditional mail, depending on the number of filings.

Penalties for Non-Compliance

Failure to correctly file Form 1099-C can result in significant penalties:

- Creditor Penalties: Incurred for failing to file the form or providing erroneous details, including penalty fees per form.

- Debtor Consequences: Incorrect reporting of debt forgiveness on tax returns can lead to additional taxes or audits.

Filing Deadlines & Important Dates

Ensure compliance by adhering to key deadlines:

- January 31st: Deadline for providing forms to debtors.

- February 28th/March 31st: Due dates for paper/electronic submissions to the IRS.

- Report Adjustments: Respond promptly to any IRS notices of discrepancy to avoid penalties.