Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out pr application internal revenue code with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the pr application internal revenue code in the editor.

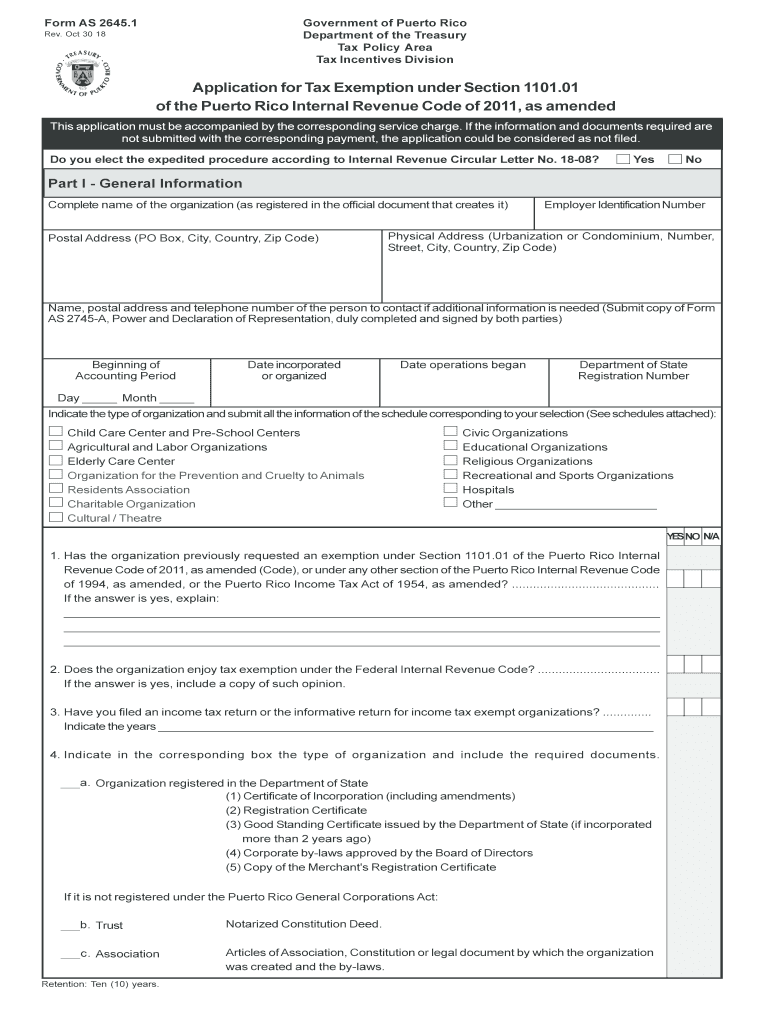

Begin by filling out Part I - General Information. Enter the complete name of your organization as registered, along with the postal and physical addresses. Ensure you include your Employer Identification Number.

Indicate whether you elect the expedited procedure according to Internal Revenue Circular Letter No. 18-08 by selecting 'Yes' or 'No'.

Provide details about your organization’s type and submit any required documents based on your selection from the attached schedules.

In Part II - Information Regarding Activities and Operations, describe your organization's past, current, and planned activities in detail. Include sources of income and fundraising programs.

Complete all additional questions relevant to your organization type, ensuring that all necessary documentation is attached for a smooth submission process.

Start using our platform today to streamline your form completion process for free!

Fill out pr application internal revenue code online It's free

See more pr application internal revenue code versions

We've got more versions of the pr application internal revenue code form. Select the right pr application internal revenue code version from the list and start editing it straight away!

Tax Return Information: Under the Internal Revenue Code, the IRS can withhold tax [r]eturns and return information. Protected information includesRead more

For purposes of the preceding sentence, an individual shall not be treated as a lawful permanent resident for any taxable year if such individual is treated asRead more

About Form 8802, Application for U.S. Residency Certification

Mar 30, 2026 Use Form 8802 to request Form 6166, a letter of U.S. residency certification for purposes of claiming benefits under an income tax treaty orRead more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.