Definition and Meaning of Repossession Motor Vehicle

Repossession of a motor vehicle refers to the legal process by which a lender or lessor takes back possession of a vehicle from the borrower or lessee due to the latter's failure to meet the financial obligations outlined in a conditional sales contract, chattel mortgage, or security agreement. This process is typically triggered by missed payments or breach of contract terms, and it enables the creditor to recover the collateral used to secure the loan.

Key aspects of repossession include:

- Contractual Basis: Repossession is defined by the specific terms detailed in the financing agreement. The agreement must clearly outline the conditions that allow for repossession, including payment schedules and default terms.

- Legal Framework: Laws governing repossession vary by state, making familiarity with local regulations essential. This includes understanding consumers' rights and the procedures that must be followed by lenders.

- Types of Repossession: Repossession can be voluntary, where the borrower willingly returns the vehicle, or involuntary, where the lender takes the vehicle without the borrower's consent (often with a tow truck).

Understanding the definition and implications of repossession is crucial for both lenders and borrowers to navigate their rights and responsibilities effectively.

Steps to Complete the Repossession Process for a Motor Vehicle

Completing a repossession involves several critical steps that align with legal requirements and contractual obligations:

- Review Contractual Terms: Before initiating repossession, the lender must review the terms of the loan agreement to confirm that the borrower is in default. This involves checking payment history and compliance with all terms.

- Send Notice to Borrower: Typically, a formal notice must be provided to the borrower, informing them of the default. This may involve a specific "notice of vehicle repossession" letter that states the amount due and a final opportunity to avoid repossession by making payment.

- Locate the Vehicle: The lender must determine the vehicle's location. This may involve contacting the borrower or using tracking devices, provided these practices comply with state and federal privacy laws.

- Secure Repossession: If the borrower does not remedy the default, the lender can arrange for a professional repossession agent to take possession of the vehicle. This process should be approached with caution to avoid potential confrontations with the borrower.

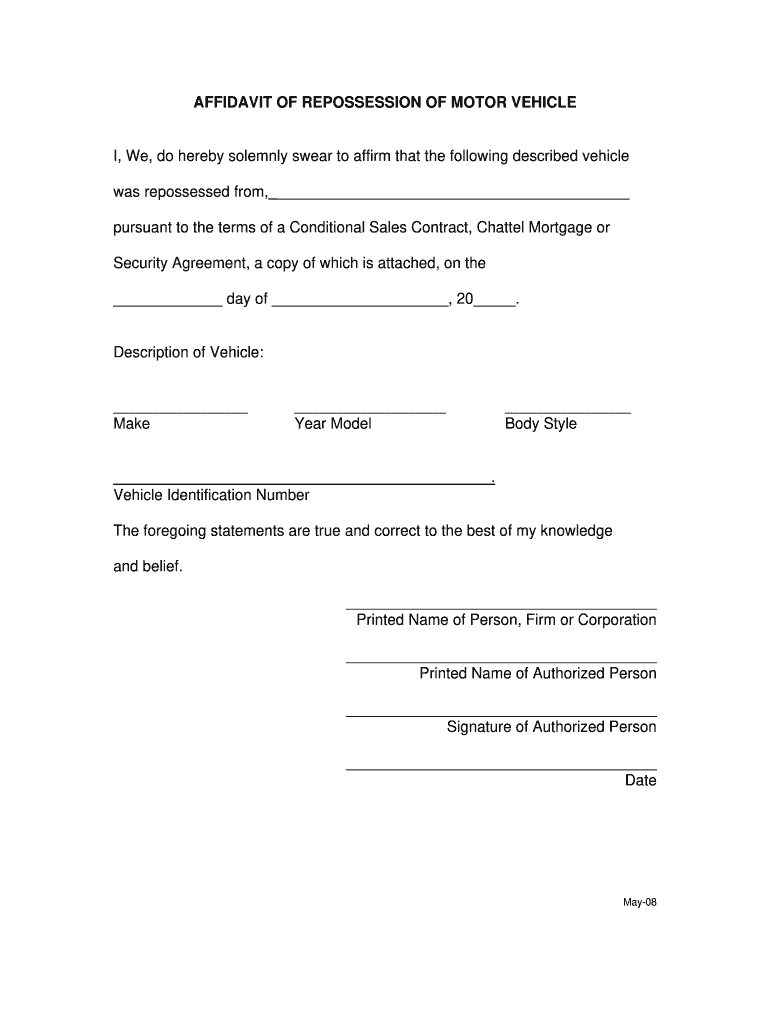

- Document the Repossession: Completing an affidavit of repossession is vital. This document confirms the taking of possession and should include details about the vehicle, the contractual basis for repossession, and signatures from the repossession agent and lender.

Following these steps systematically helps ensure that the repossession process adheres to legal standards and minimizes potential disputes.

Legal Use of Repossession Motor Vehicle

Legal repossession is governed by federal and state laws, which provide a framework for how lenders can reclaim a vehicle. Understanding these laws is pivotal for maintaining compliance and protecting consumer rights:

- Uniform Commercial Code (UCC): Most repossession activities fall under the UCC, which sets the guidelines for secured transactions and repossession processes. Lenders must follow these rules to avoid legal repercussions.

- State Regulations: Different states have specific laws regarding notice requirements before repossession and the methods by which a vehicle can be repossessed. Familiarity with state-specific rules helps lenders avoid lawsuits or claims of wrongful repossession.

- Consumer Rights: Borrowers have rights during the repossession process, including the right to receive notice and to reclaim their vehicle under certain conditions. Understanding these rights is crucial for both parties involved.

Navigating the legal landscape surrounding repossession ensures compliance and protects the interests of both lenders and borrowers.

Important Terms Related to Repossession Motor Vehicle

Familiarity with key terminology associated with vehicle repossession can clarify the process for both lenders and borrowers. Here are some critical terms:

- Repossession Affidavit: A legal document that the lender uses to affirm the repossession of the vehicle, detailing the circumstances and evidence supporting the action.

- Default: The failure to fulfill the obligations outlined in the loan agreement, typically involving missed payments.

- Voluntary Repossession: A process where the borrower willingly returns the vehicle to the lender, often to avoid additional fees or costs.

- Involuntary Repossession: Repossession initiated by the lender without the borrower's consent, usually requiring the use of a repossession agent or tow truck.

- Conditional Sales Contract: A legal agreement between the borrower and lender outlining the terms of the loan used to purchase the vehicle.

Understanding these terms is essential for managing and navigating the repossession process effectively.

State-Specific Rules for Repossession Motor Vehicle

Each state in the U.S. has its own set of rules governing motor vehicle repossession, impacting both the lender's approach and the borrower's rights. Key considerations include:

- Notice Requirements: Some states require lenders to provide written notice to borrowers before repossession occurs. The notice must include details about the default and the opportunity to rectify it.

- Repossession Methods: States regulate whether repossession can occur without breach of peace. For example, some states mandate that repossession agents must have proper credentials or licenses.

- Redemption Periods: After repossession, many states allow borrowers a specific time frame during which they can redeem their vehicle by paying the outstanding debt, including applicable fees.

- Auction and Sale of Repossessed Vehicles: Laws dictate how repossessed vehicles must be sold, including the requirement for public auctions or specific disclosures during the sales process.

Navigating these state-specific regulations is vital for compliance and protecting all parties involved in a repossession scenario.

Examples of Repossession Motor Vehicle Scenarios

Understanding practical scenarios can clarify how repossession functions in real-world contexts:

- Missed Payments: A borrower misses three consecutive monthly payments on their car loan. The lender sends a notice of vehicle repossession and, after not receiving a response, engages a repossession agent to reclaim the vehicle.

- Voluntary Repossession: Facing financial hardship, a borrower decides to return a vehicle to the lender before additional fees accrue. They contact the lender to arrange a voluntary repossession, clearly documenting the return of the vehicle.

- Disputed Default: A borrower contests the lender's claim of default, arguing that they sent the payment on time. This scenario can lead to a legal dispute where the borrower challenges the repossession legally.

These examples highlight various complexities surrounding the repossession process, offering insights into how to navigate potential challenges successfully.