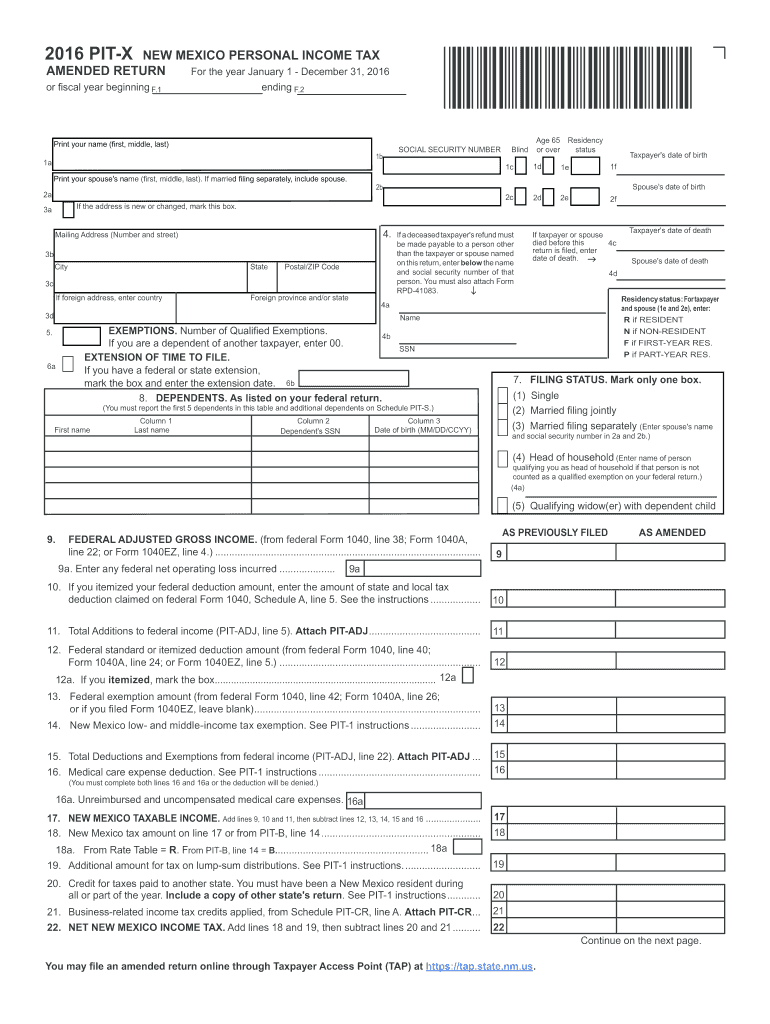

Definition & Meaning

The term "or fiscal year beginning F" refers to a specific identification used within financial contexts, often related to tax forms or documentation that requires the specification of a fiscal year start. It typically serves as a placeholder or indicator for when an organization's fiscal calendar begins. Unlike the calendar year, which follows January through December, a fiscal year can begin in any month and extends for 12 consecutive months. This is crucial for businesses and accounting departments as it defines the period for financial reporting and tax obligations, affecting annual budget planning and evaluation.

Significance of the Fiscal Year

- Financial Planning: It forms the basis for creating budgets, forecasts, and financial analysis, ensuring that all accounting aligns with the company's operations.

- Comparative Analysis: Allows for consistent year-over-year comparison in financial statements, which is critical for strategic planning and performance assessment.

How to Use the or Fiscal Year Beginning F

Using the "or fiscal year beginning F" requires identifying the accurate start month of your fiscal year when dealing with forms or reports needing this specification. For example, if a company adopts a fiscal year starting in July, this detail must be clearly marked on any relevant tax or financial document.

Practical Example

- Non-Calendar Fiscal Year: A retailer might choose a fiscal year beginning in February to coincide with seasonal sales cycles, thereby reflecting business operations more accurately in financial reports.

Steps to Complete the or Fiscal Year Beginning F

Filling out any form indicating "or fiscal year beginning F" involves specific steps to ensure accuracy:

- Identify Fiscal Year Start: Determine the initial month of your fiscal year. This is pivotal for accurately aligning financial activities.

- Record Specific Dates: Clearly specify the starting month and year on the form.

- Check for Consistency: Ensure the start date aligns with existing company records and past filings.

Verifying Information

- Consult Internal Records: Review official documents or accounting software to verify the fiscal year's start, ensuring no discrepancies.

Required Documents

To effectively engage with the "or fiscal year beginning F," certain documents are often necessary:

- Financial Statements: These include balance sheets and income statements that align with the fiscal year.

- Previous Tax Filings: Past submissions help verify consistency and accuracy in annual reporting.

- Internal Records: Business documents that denote the established fiscal year period.

Important Terms Related to or Fiscal Year Beginning F

Understanding related terminology enhances clarity:

- Fiscal Year (FY): The 12-month period used for accounting purposes.

- Accounting Period: Specifies the time frame for reporting income and costs.

Examples of Related Terms

- Calendar Year: Traditionally spans January 1 to December 31.

- Quarterly Reports: Subdivisions within a fiscal year, affecting reporting frequencies.

Filing Deadlines / Important Dates

Different organizations may face various deadlines based on their fiscal-year starts:

- IRS Deadlines: Typically require filing by the 15th day of the fourth month following your fiscal year's end.

Examples

- April 15th Filing for Calendar Year: For fiscal years starting on January 1.

- Different Filing Dates: Adjustments for non-calendar fiscal years, depending on the IRS requirements.

Legal Use of the or Fiscal Year Beginning F

Compliance with legal standards is vital when indicating "or fiscal year beginning F." Proper documentation is necessary for tax law adherence, and deviations may result in penalties.

Legal Guidelines

- Consistency with Company Policy: Reflects accurate financial conditions as understood under U.S. tax law.

- IRS Conformance: Ensuring alignment with federal requirements for fiscal year declaration.

Who Issues the Form

Understanding the source and authority issuing forms associated with "or fiscal year beginning F" is important for compliance:

- IRS Issuance: The IRS mandates many of these forms for federal tax purposes in the United States.

Official Entities

- State Tax Authorities: May issue analogous forms, necessitating state-specific compliance.

Each of these sections should be explored in depth to provide comprehensive guidance to individuals or businesses dealing with the "or fiscal year beginning F."