Definition & Meaning

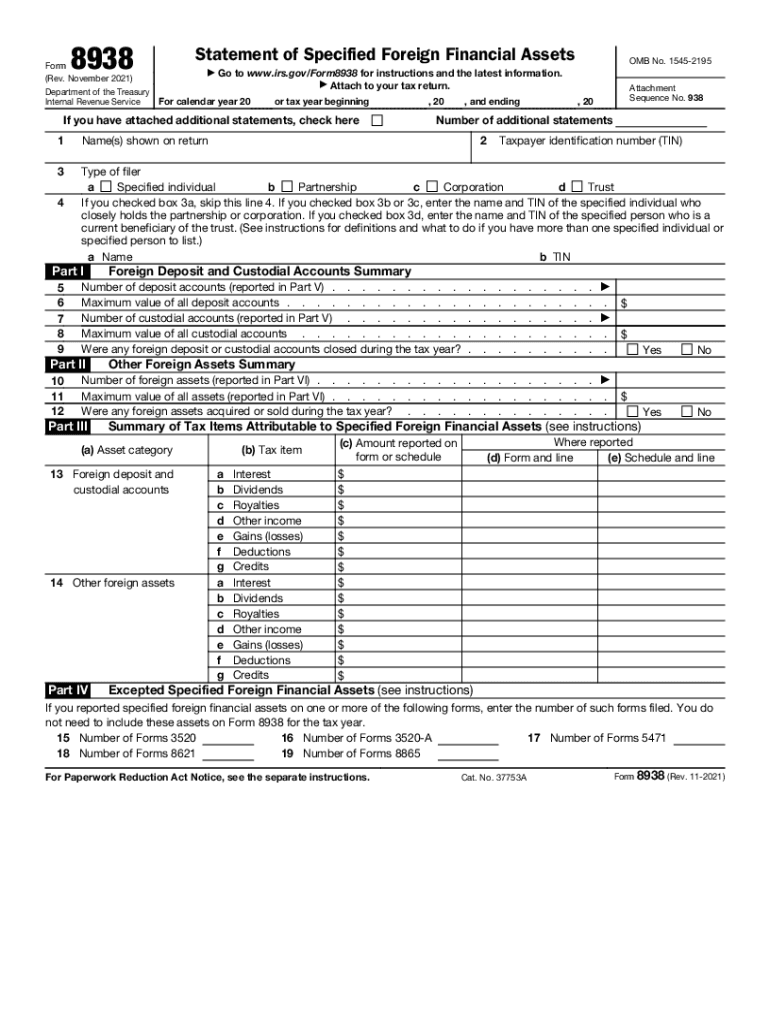

Form 8938, known as the "Statement of Specified Foreign Financial Assets," is required by the IRS for certain individuals, corporations, partnerships, and trusts to report their foreign financial assets. Only specified individuals, meaning U.S. citizens, resident aliens, and certain non-resident aliens who hold substantial foreign assets, are required to file this form. The purpose is to prevent tax evasion and ensure that all financial activities with foreign entities are disclosed.

Form 8938 demands comprehensive details about foreign deposit accounts, investment accounts, and any other foreign assets that meet particular thresholds. The form must be attached to the annual tax return of the filer.

Key Elements of the Form 8938

Asset Reporting Requirements

Form 8938 mandates detailed reporting on a wide range of foreign financial assets. This includes foreign bank accounts, foreign investment accounts, and interests in foreign entities. Each reported asset must include specific details:

- Maximum value during the tax year

- Information on income generated by each asset

- Date of acquisition or disposition

- Description of the asset

Filing Thresholds

The filing thresholds for Form 8938 vary based on several factors, including filing status and place of residence (inside or outside the U.S.). These thresholds determine whether one needs to file:

- For singles or married filing separately within the U.S., the threshold is $50,000 on the last day of the tax year or $75,000 at any time during the year.

- For those living outside the U.S., the threshold increases to $200,000 on the last day or $300,000 at any time for singles, and higher for joint filers.

Steps to Complete the Form 8938

-

Gather Financial Information: Collect all necessary details about your foreign financial assets, including account numbers, maximum values, and any related income.

-

Determine Filing Requirement: Check the asset thresholds and determine if you meet the requirement for filing the form.

-

Enter Asset Information: Provide all requested information on Form 8938, ensuring accuracy in the details reported.

-

Attach to Tax Return: Form 8938 must be attached to your annual federal income tax return.

-

Submit by Tax Deadline: Ensure that the form is submitted by the due date of your tax return, typically April 15, unless an extension has been granted.

Common Mistakes

- Failing to include all required assets

- Misreporting maximum asset values

- Omitting asset income details

Penalties for Non-Compliance

Failure to file Form 8938 can lead to substantial penalties. The initial penalty for not filing the form is $10,000, with additional penalties up to $50,000 if non-compliance continues after IRS notice. Furthermore, a 40% penalty may apply to any understatement of tax attributable to non-disclosed foreign financial assets.

Serious Consequences

- Additional penalties may arise if fraud is detected.

- Criminal penalties apply if willful evasion is established.

Who Typically Uses the Form 8938

Primarily used by U.S. taxpayers who have foreign financial interests or assets meeting specific thresholds, including:

- U.S. citizens living abroad

- Residents with foreign assets

- Corporations, partnerships, or trusts with specified foreign assets

Exemptions

Certain entities, such as certain trusts or retirement plans, may be exempt from filing depending on their foreign asset exposure and structure.

IRS Guidelines

The IRS provides specific instructions and guidance on how to accurately complete Form 8938. This includes:

- Detailed asset reporting instructions

- Information regarding asset valuation methods

- Guidance on income and gains reporting from foreign assets

Adhering strictly to these guidelines reduces errors and helps prevent potential penalties.

How to Obtain the Form 8938

Form 8938 can be downloaded directly from the IRS website. Taxpayers can also acquire the form through tax software programs that integrate IRS forms, ensuring the most current version is used.

Access Methods

- IRS website: Available in PDF format for download and print.

- Tax software: Often included in major tax preparation software packages like TurboTax and H&R Block.

Disclosure Requirements

All specified foreign financial assets must be disclosed. This means providing comprehensive documentation for each account or asset:

- Ownership details

- Income or dividends generated

- Changes in value over the tax year

Documentation Needed

- Bank statements for foreign accounts

- Ownership certificates

- Documentation of income from foreign sources

Filing Deadlines / Important Dates

For most taxpayers, Form 8938 is due with their federal tax return on April 15. If an extension for the tax return is granted, the deadline for Form 8938 extends accordingly.

Considerations for Expats

- Automatic extension to June 15 for American citizens living abroad.

- Additional extension possible to October 15 if requested.

Software Compatibility

Many tax preparation software packages support Form 8938, aiding in accurate completion and timely filing. Compatible software includes:

- TurboTax: Offers step-by-step guidance on completing Form 8938.

- QuickBooks: While primarily for business use, it can help assemble necessary financial data.

- H&R Block: Provides form filling capabilities alongside tax filing services.