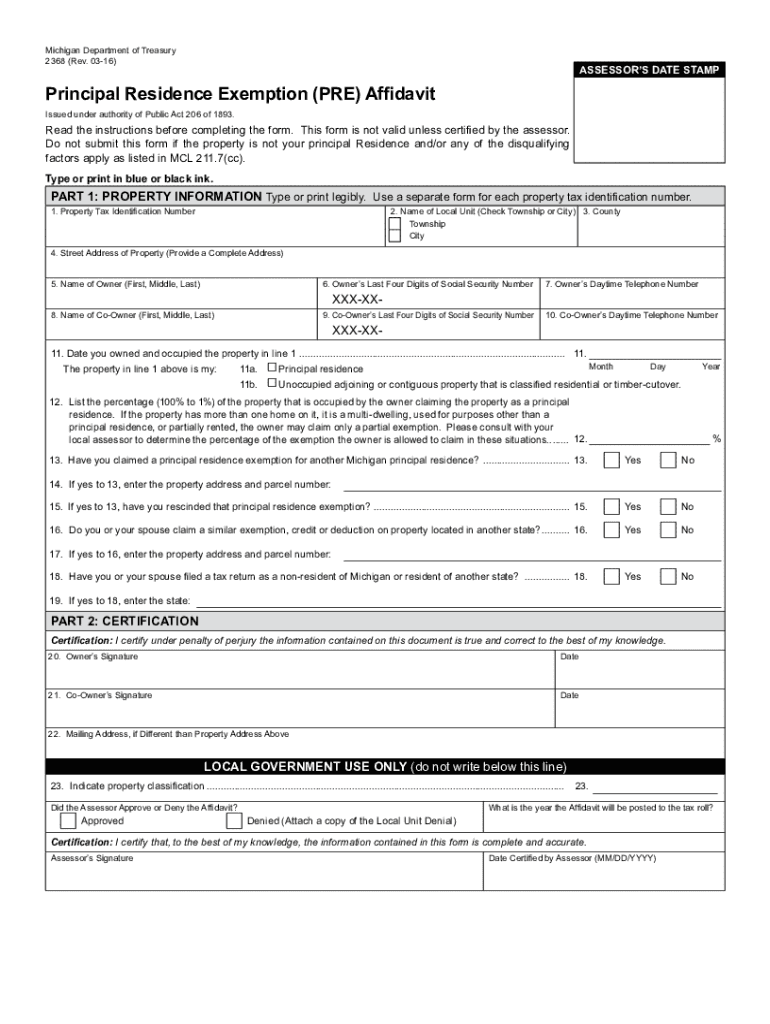

We've got more versions of the principal exemption form. Select the right principal exemption version from the list and start editing it straight away!

Principal exemption formPrincipal exemption for property taxPrincipal residence Exemption Frequently asked questionsPrincipal Residence Exemption MichiganPrincipal residence Exemption (PRE) AffidavitConditional rescission of Principal Residence ExemptionWhat is a principal residence exemptionRequest to Rescind principal residence Exemption

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

In these circuits, agencies whose primary function is not law enforcement may still rely on Exemption 7. principal function of law enforcementRead more

The various exemption applications provide instruction for the required documents that must accompany the application to aid in the review for approval.

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.