Definition & Meaning

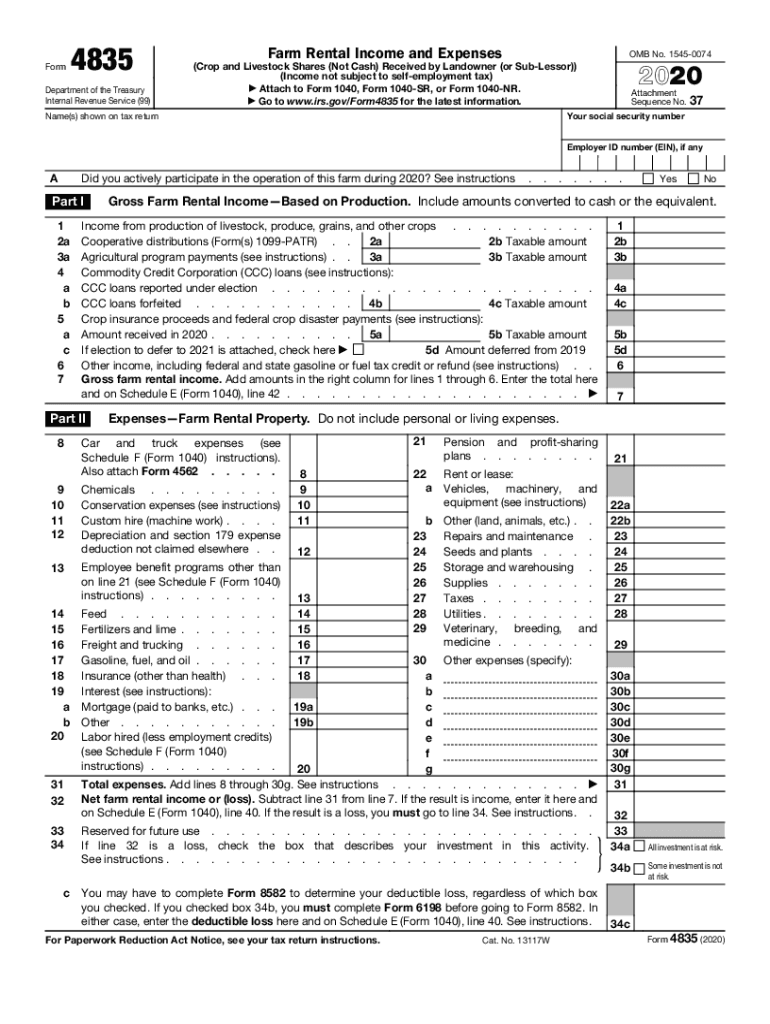

Form 4835, officially titled "Farm Rental Income and Expenses," is a document used by landowners or sub-lessors who receive rental income based on crop or livestock production but do not materially participate in the farming operations. This form is essential for detailing income and expenses related to rental agreements, ensuring proper tax reporting and compliance. It is particularly relevant for individuals who lease out their farmland to tenants and wish to report the resulting financial activities without being actively involved in the operational aspects of farming.

Distinction from Active Farm Operations

Form 4835 specifically applies to scenarios where the landowner is not actively engaged in the management or day-to-day operations of the farm. Unlike those who materially participate and fill out Schedule F, this form caters to passive income arrangements. Understanding this distinction is crucial for accurate tax filing and avoiding potential IRS penalties.

Key Elements of the Form 4835

The core components of Form 4835 include sections to report gross farm rental income and itemized expenses associated with the farm property. These elements are critical for calculating the net income or loss from farm rental activities.

Specific Sections

- Gross Farm Rental Income: This section requires documentation of income received from tenants, typically outlined according to the production yield, such as a share of crops or livestock sold.

- Expenses: Includes various deductible costs such as repairs, property taxes, and insurance. Accurate reporting of these expenses is essential to determine taxable income correctly.

Additional Attachments

Supporting documentation, such as lease agreements or receipts for expenses, may be necessary to substantiate the information provided on Form 4835. It helps in auditing processes and reinforces the accuracy of the reported figures.

Steps to Complete the Form 4835

Filling out Form 4835 requires careful attention to detail to ensure compliance with IRS standards. Below is a step-by-step guide to assist in the accurate completion of the form.

Step-by-Step Instructions

- Input Personal Information: Begin with your name and Social Security Number, establishing the document's authenticity.

- Document Income: Enter the total farm rental income received, ensuring it reflects any contractual agreements with tenants.

- Calculate Expenses: List all relevant expenses associated with the farm's operation but not including costs for any personal or non-rental purposes.

- Determine Net Income or Loss: Subtract total expenses from income to assess the net figure, crucial for personal tax filings.

- Review and Confirm Accuracy: Double-check all entries and computations to ensure correctness before submission.

Common Pitfalls

Errors in this form often stem from improper expense categorization or inaccurate income reporting. Landowners should maintain detailed records and seek professional advice if needed to mitigate these issues.

Important Terms Related to Form 4835

Understanding specific terminology associated with Form 4835 is vital for accurate completion and comprehension of its requirements.

Key Definitions

- Material Participation: Involvement in the farm’s decision-making or daily operations, disqualifying the use of Form 4835 for those engaged.

- Passive Income: Earnings received from rental activities without active involvement.

- Gross Income: Total income before expenses, which can affect the overall tax bracket positioning.

Usage in Context

Familiarity with these terms aids in recognizing applicable conditions for Form 4835. It ensures that taxpayers appropriately classify their income, aligning with the IRS’s definitions and criteria.

IRS Guidelines

The IRS provides detailed instructions for completing Form 4835, specifying how rental income and expenses should be treated under tax regulations. These guidelines are pivotal for avoiding errors that could result in discrepancies or audit triggers.

Critical IRS Directions

- Documentation: Emphasis on maintaining thorough records to justify income and deductions.

- Deadlines: Timely submission of Form 4835 as part of annual tax filings to prevent penalties.

- Amendments: Procedure for correcting previously submitted forms in case of errors or omissions.

Reliance on Professional Assistance

For complex scenarios, the IRS advises consulting with a tax professional to navigate intricate tax laws and ensure compliance.

Examples of Using the Form 4835

Exploring real-world examples provides clarity on how Form 4835 is utilized by different stakeholders in the agricultural industry.

Case Study Scenarios

- Non-Participating Landowner: An individual owning farmland who enters into a lease agreement with a farming cooperative. The tenant manages operations, and the landowner files Form 4835 to report income based on crop production rather than participation.

- Family Heirs: Siblings inheriting farmland and leasing it to a third party. They use Form 4835 to accurately declare rental profits distributed among them under non-material participation clauses.

Filing Deadlines / Important Dates

Adhering to tax deadlines is crucial to avoid penalties and maintain good standing with the IRS. Form 4835 is typically included with the annual tax return submissions.

Important Dates

- Annual Tax Filing Deadline: Form 4835 should be filed with IRS Form 1040 by April 15 each year unless extensions are granted.

- Extension Conditions: Filers can apply for a filing extension using IRS Form 4868 if additional time is required.

Planning for Timely Submission

Advance preparation and organizing all necessary documents can ease the process, helping meet deadlines swiftly.

Penalties for Non-Compliance

Failing to comply with the filing requirements of Form 4835 can result in financial penalties and other legal implications from the IRS.

Potential Repercussions

- Monetary Fines: Late or incorrect submissions may incur additional charges.

- Legal Scrutiny: Non-compliance increases the risk of audits and subsequent investigations, potentially resulting in larger penalties.

Mitigation Strategies

Timely tax planning and thorough record-keeping are effective strategies to minimize risks associated with non-compliance. Additionally, regular consultations with tax professionals can provide preemptive guidance.