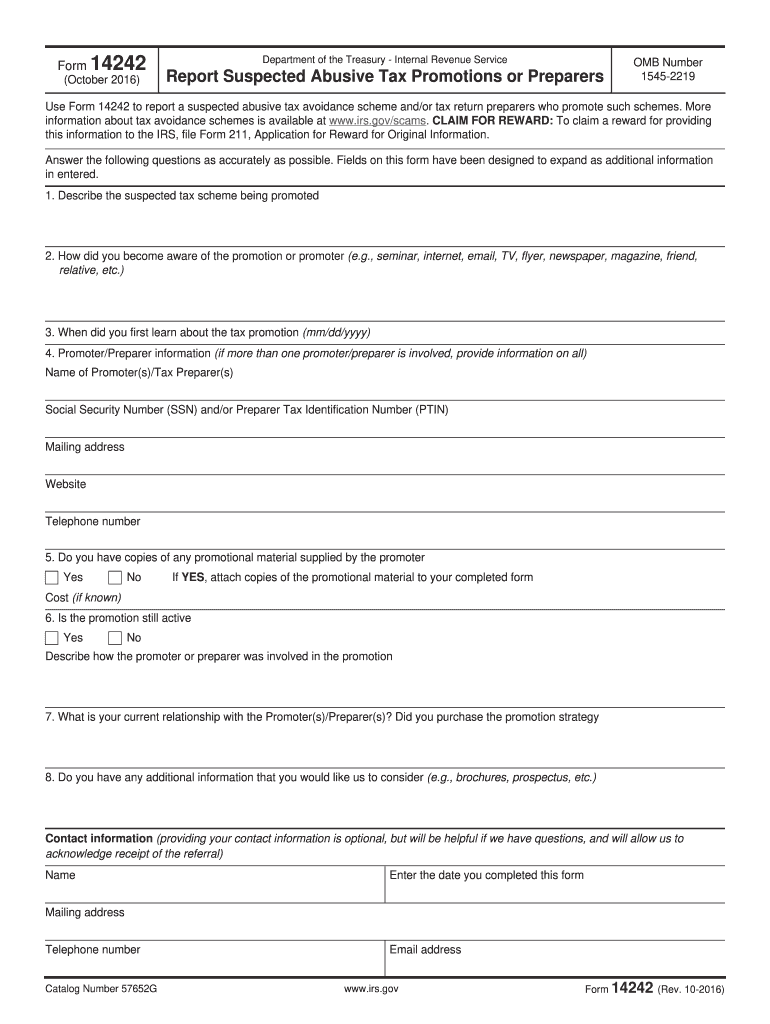

Definition and Meaning of IRS Form 14242

IRS Form 14242 is an official document used to report potentially abusive tax avoidance schemes and the tax return preparers who promote these schemes to the Internal Revenue Service (IRS). This form is designed to gather detailed information about the suspected scheme, including details about the promoter and any related promotional materials. Accurate and thorough reporting is emphasized to ensure the IRS has the necessary information to investigate potential abuses effectively.

Steps to Complete IRS Form 14242

To fill out IRS Form 14242, you need to follow several key steps to ensure all required information is accurately provided:

- Gather Information: Before beginning, collect all relevant details about the suspected tax avoidance scheme, including promotional materials, dates, and involved parties.

- Complete Section I: Enter your own contact information. This is important for any follow-up questions from the IRS.

- Describe the Scheme: Clearly outline how the scheme operates, including how it is marketed and any claims made about tax benefits.

- Enter Promoter Details: Fill in information about the person or entity promoting the scheme, such as their name, contact details, and any known associates.

- Attach Supporting Documents: Include copies of promotional materials or other documents that support your claims.

- Review and Submit: Double-check all entries for accuracy and completeness before submitting the form to the IRS.

How to Obtain IRS Form 14242

IRS Form 14242 can be obtained from multiple sources to ensure accessibility:

- Download from the IRS Website: The most straightforward method is to download the form directly from the IRS official website. Search for "Form 14242" in their forms section.

- Local IRS Offices: Visit a local IRS office where you can request a printed copy of the form.

- Request By Mail: You can contact the IRS to have the form sent to you by mail if downloading is not an option.

Importance of IRS Form 14242

Form 14242 plays a crucial role in the IRS’s efforts to combat tax fraud and abusive tax avoidance schemes. It enables individuals to report suspicious activities that might otherwise go unnoticed. This form is essential for maintaining the integrity of the tax system by ensuring that all tax filers pay their fair share according to the law.

- Deterring Fraud: By allowing individuals to report schemes, it helps deter both promoters and potential taxpayers from engaging in fraudulent activities.

- Public Trust: Enhances public trust in the fairness of the tax system by demonstrating the IRS’s commitment to addressing abuse.

- Informed Decisions: Help potential participants of schemes make informed decisions by understanding the risks involved through reported experiences.

Who Typically Uses IRS Form 14242

IRS Form 14242 is generally utilized by taxpayers or professionals who come across a suspect tax scheme. The following groups are most likely to submit this form:

- Tax Professionals: Accountants or tax preparers who identify a scheme may submit this form to alert the IRS.

- Concerned Individuals: Taxpayers who are targeted by or become aware of dubious tax strategies that seem designed to evade taxes.

- Whistleblowers: Employees or insiders with knowledge of corporate tax strategies that may cross the line into avoidance or evasion.

Legal Use of the IRS Form 14242

Using IRS Form 14242 requires adherence to certain legal guidelines to protect the integrity of its use:

- Truthful Reporting: It is mandatory that all information provided in Form 14242 is truthful and accurate to the best of the reporter's knowledge.

- Confidentiality: The IRS is committed to maintaining the confidentiality of the information provided, protecting the reporter's identity when possible.

- Potential Rewards: There are legal protocols for claiming rewards based on the information submitted. If the reported scheme leads to the recovery of taxes, fines, or penalties, the submitter may be eligible for a reward.

Examples of Using IRS Form 14242

To understand the real-world application of IRS Form 14242, consider these scenarios:

- Multi-Level Marketing Scheme: An employee discovers that the company’s tax saving strategies are based on pyramid schemes. The employee submits Form 14242 after collecting promotional materials.

- Fictitious Deductions: A tax professional notices a trend among some preparers who encourage clients to claim non-existent deductions. The preparer reports these suspicious practices to the IRS using the form.

- Misleading Investment Groups: An investor realizes that a financial advisor is persuading clients to invest in a strategy that offers illegitimate tax credits. The investor can utilize Form 14242 to alert the IRS.

Required Documents for IRS Form 14242 Submission

When submitting IRS Form 14242, it is important to accompany the form with supporting documents that substantiate the suspected tax scheme:

- Promotional Materials: Copies of brochures, emails, or advertisements used to promote the scheme.

- Correspondence: Written communication from the promoter explaining how the scheme works.

- Financial Statements or Tax Returns: Any documents that show the implementation of the scheme in practice.

Key Elements of IRS Form 14242

Understanding the essential components of IRS Form 14242 ensures effective and accurate completion:

- Reporter Information: Includes name, contact information, and details of the reporting party to facilitate follow-up.

- Scheme Description: Comprehensive detailing of how the scheme operates, including any assumptions and promises made by the promoter.

- Promoter Identification: Information about the individuals or entities involved in the dissemination of the tax avoidance scheme.

- Supporting Evidence: Attachments that corroborate the claims made in the submission, enhancing credibility.

Penalties for Non-Compliance

Failing to comply with tax reporting regulations after identifying a tax avoidance scheme can lead to several consequences:

- Legal Action: Potential legal action against those involved in the promotion or participation of the scheme.

- Fines and Penalties: Imposition of substantial fines and financial penalties for negligent or intentional non-reporting.

- Reputation Damage: Significant harm to both personal and business reputations as a result of involvement in unethical tax practices.