Definition and Purpose of Schedule M-3

Schedule M-3 (Form 1065) is used by partnerships to reconcile financial statement net income with taxable income as reported to the IRS. It offers a clearer view of income discrepancies attributed to different accounting methods, ensuring accurate reporting. Created to increase transparency, this form is mandatory for partnerships with substantial assets or receipts, promoting compliance and reducing audit risks. Through Schedule M-3, these entities can align financial statement figures with tax return items, providing detailed insights into income and expense reporting.

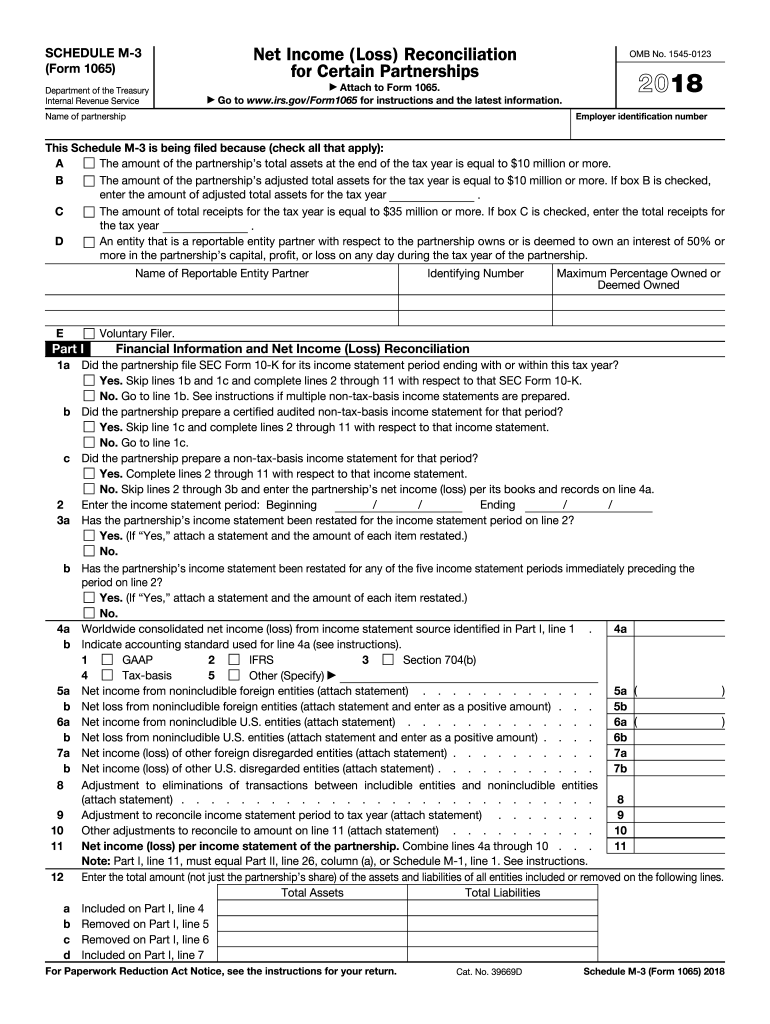

How to Use Schedule M-3

Using Schedule M-3 involves several steps designed to provide clarity and accuracy in tax filings. It requires detailed entries and comparisons between book and tax data. Start by gathering financial statements and tax records. Review each section carefully; the form is divided into parts that address income, adjustments, and reconciliations. Utilize the adjustment section for income or deductions discrepancies. Ensure all figures align with supporting documentation prior to submission, and maintain meticulous records for future reference. Proper usage facilitates transparent tax reporting and compliance.

Steps to Complete Schedule M-3

- Collect Necessary Documentation: Gather financial statements, tax returns, and relevant documentation that highlight business income and expenses.

- Complete Part I: Financial Information: Enter the net income as per the financial statements and the book income.

- Account for Adjustments in Part II: Record tax adjustments for book differences, ensuring that all income is properly reported and justified.

- Reconciliation in Part III: Calculate and reconcile differences between book income and tax returns through comprehensive entries and adjustments.

- Review and Verify: Before submission, conduct a thorough review of the form with all figures and corresponding documentation checked for accuracy.

- Submission: Once the form is complete and verified, submit it along with the Form 1065, following IRS guidelines.

Legal Use of Schedule M-3

The Schedule M-3 must be used in compliance with U.S. tax regulations. It provides a standardized method for reporting and reconciling income, highlighting areas where tax and book accounting differ. Proper legal use mandates accurate reporting and justifications for adjustments, aligning tax filing with IRS requirements. Key legal purposes include the accurate bridging of accounting methods and the avoidance of punitive actions from inaccuracies or omissions during filing.

Key Elements of Schedule M-3

- Reconciliation of Financial and Tax Accounting: Aligns book net income to taxable income.

- Comprehensive Adjustment Details: Provides a breakdown of temporary and permanent adjustments.

- Income Statement Presentation: Requires detailed presentation of financial information.

- Adjustment Categories: Segregates different types of financial adjustments ensuring detailed reporting.

- Supporting Documents: Ensures each figure has corresponding documentation.

IRS Guidelines for Schedule M-3

The IRS provides specific instructions for Schedule M-3, outlining completion, submission, and consistent application. These guidelines ensure that partnerships adhere to regulations governing income reporting. It's crucial to follow these to mitigate audit risks and penalties. The IRS emphasizes transparency and accuracy in reporting, requiring entities to provide a full account of financial and taxable income likenesses and differences.

Filing Deadlines and Important Dates

Schedule M-3, as part of Form 1065, follows the annual partnership tax filing deadlines. Generally due March 15, extensions may be available to September 15. Timely filing is crucial to avoid penalties, emphasizing the importance of maintaining an updated calendar. Monitor IRS announcements for possible changes affecting submission dates.

Penalties for Non-Compliance

Non-compliance with Schedule M-3 reporting can result in penalties, including fines and an increased likelihood of IRS audits. Penalties vary based on the degree of non-compliance, from failure to file to inaccuracies in reporting. Engaging a tax professional or using compliant software can help partnerships meet IRS regulations and avoid financial repercussions.

Digital vs. Paper Version of Schedule M-3

Filing Schedule M-3 can be done digitally or on paper, with e-filing as the preferred method due to its efficiency and error reduction. Digital filing offers quicker processing and acknowledgment from the IRS, while paper filing requires precise mailing procedures. Regardless of the method, maintaining a back-up of the submitted forms is advisable for organizational records and potential audits.

Business Types That Benefit Most from Schedule M-3

Businesses engaging in complex transactions or those with substantial income variations benefit most from Schedule M-3. Partnerships and large corporations who face significant discrepancies between reportable book and tax income find it essential for revealing and justifying these differences. Utilizing Schedule M-3 enhances transparency and supports accurate tax compliance for entities dealing with assorted income and adjustment structures.