Definition and Purpose of the 2011 763 Form

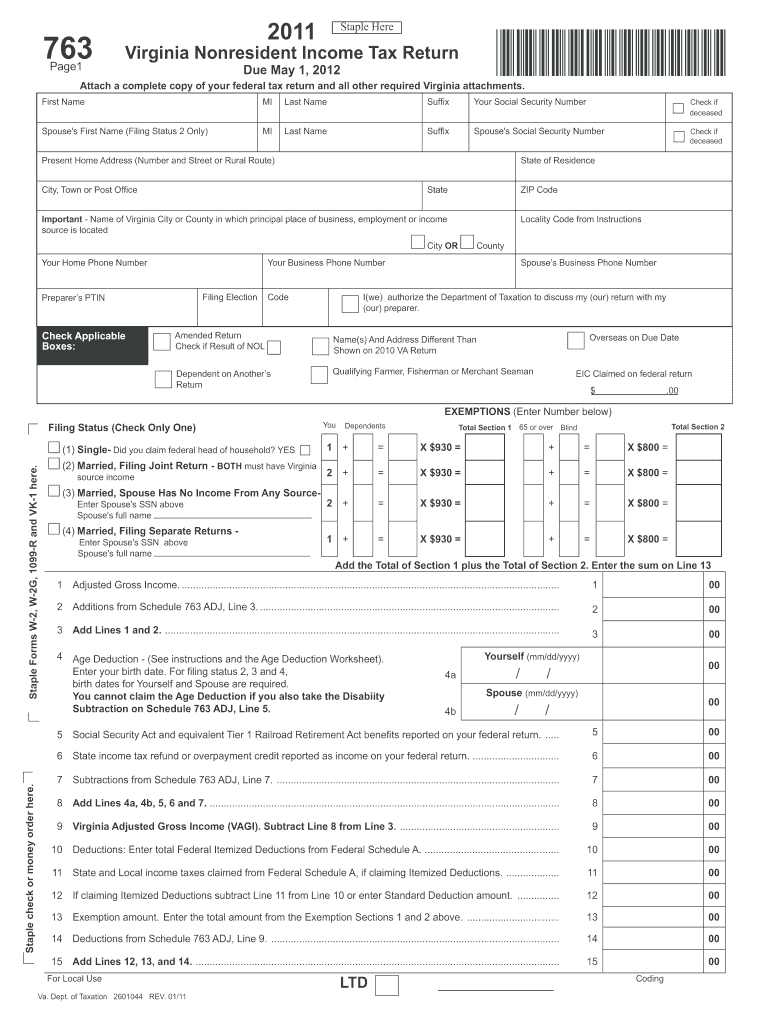

The 2011 763 form is a specific tax document used by nonresidents of Virginia to file income taxes for the 2011 tax year. This form is essential for individuals who have income from Virginia sources but reside outside the state. It primarily helps in determining the correct amount of Virginia income tax owed, ensuring compliance with state tax laws.

- Nonresident Status: The form applies to individuals who do not live in Virginia but have earned income within the state.

- Income Sources: Typically includes wages, rentals, business proceeds, or any other income generated from Virginia-based activities.

Understanding the purpose and appropriate use of the 2011 763 form can significantly impact your tax compliance process and ensure you meet state obligations efficiently.

How to Obtain the 2011 763 Form

Acquiring the 2011 763 form involves several accessible methods, ensuring taxpayers can obtain the necessary documents without undue inconvenience. Here are some common ways to obtain this specific form:

- Virginia Department of Taxation Website: The form is available for download on Virginia’s official tax website. This is the most straightforward method.

- Local Tax Offices: Taxpayers can visit local offices in Virginia, where paper copies are often available.

- Tax Preparation Software: Many software packages, like TurboTax or QuickBooks, provide direct access to state-specific tax forms, including the 2011 763 form.

These methods ensure that taxpayers have various options based on their preferences, whether they prefer digital downloads or physical copies.

Steps to Complete the 2011 763 Form

Accurately completing the 2011 763 form requires attention to detail across several sections. The process generally encompasses the following steps:

- Personal Information: Enter your full legal name, address, and Social Security Number.

- Income Declaration: Report all Virginia-source income, such as wages and business earnings.

- Deductions and Credits: List any eligible deductions or tax credits, keeping in mind those specific to Virginia tax statutes.

- Tax Calculation: Compute your Virginia Adjusted Gross Income, then determine the tax owed or refund due.

- Attachments: Include any necessary schedules, statements, or copies of your federal tax return to support your state tax filing.

Each step is critical for ensuring that your tax liability is calculated correctly, and all required fields on the form are completed correctly.

Required Documents

Filing the 2011 763 form necessitates several supporting documents to verify income and deductions, which are integral to the process:

- Federal Income Tax Return: A copy of the federal return is typically required to validate income and ensure accurate state tax calculation.

- W-2 Forms: Necessary to document wages earned from Virginia sources.

- 1099 Forms: Needed for reporting miscellaneous income such as dividends or self-employment income.

- Other Backup Documentation: Includes receipts for claimed deductions or credits, ensuring they meet state-specific tax code requirements.

These documents provide the substantiation necessary for income and deduction claims and support the accurate completion of the form.

Filing Deadlines and Important Dates

Timely submission of the 2011 763 form is crucial to avoid penalties and interest. Important dates to consider include:

- Filing Deadline: Typically, the tax form for the 2011 fiscal year should be filed by May 1, 2012.

- Extension Requests: Should taxpayers require additional time, they might file for an extension. However, this still requires payment of any owed taxes by the original due date.

Understanding these timelines is essential to maintain compliance and ensure any tax payments are made promptly, avoiding additional penalties.

Legal Use of the 2011 763 Form

The legal framework governing the 2011 763 form ensures it is used correctly for tax reporting purposes among nonresidents of Virginia:

- State Compliance: Ensures proper tax calculation and submission in alignment with Commonwealth of Virginia requirements.

- Legal Consequences: Misuse or incorrect filing can result in penalties, audits, or additional interest on unpaid taxes.

Taxpayers are encouraged to be comprehensive in their submissions, given the significant legal implications of incorrect or incomplete filings.

Software Compatibility for the 2011 763 Form

Digital tools ease preparation of the 2011 763 form. Compatibility with software applications makes tax filing more efficient:

- Tax Preparation Software: Commonly used platforms like TurboTax support this form, offering guided filing processes.

- Financial Software: Applications like QuickBooks enable efficient tracking and recording, streamlining the data entry process.

These resources simplify the filing process and help ensure accuracy, providing taxpayers with user-friendly methods to organize and submit their tax recordings.

Penalties for Non-Compliance

Non-compliance with filing requirements of the 2011 763 form can attract penalties, impacting nonresident taxpayers financially:

- Late Filing Penalties: Fees applied for not submitting on time. This increases the longer the delay.

- Underpayment Penalties: Levied if taxes owed are not paid by the due date, including any applicable interest charges.

Understanding the penalties can motivate timely and accurate submission, ensuring taxpayers avoid unintended financial liabilities.