Definition and Purpose of Form 1040

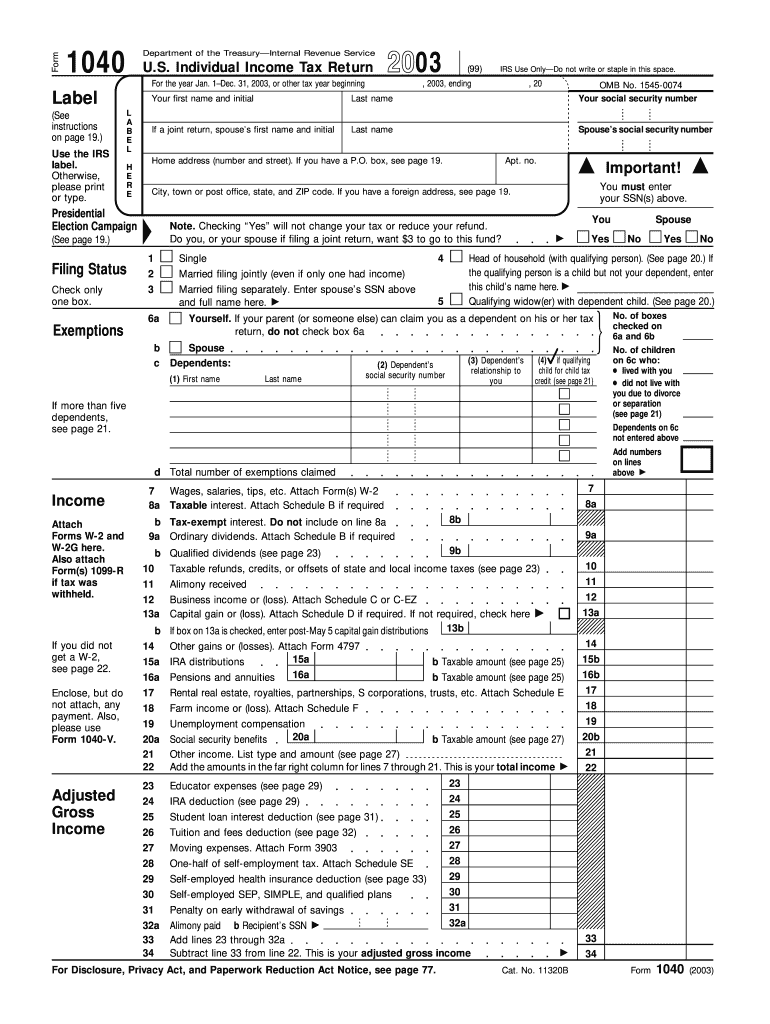

The 2003 U.S. Individual Income Tax Return, known as Form 1040, is a document issued by the Internal Revenue Service (IRS) to help individuals report income, claim deductions and credits, and calculate tax liability for the year ending December 31, 2003. Form 1040 serves as the primary tool for individuals to communicate their annual financial activity to the IRS. It includes sections for personal details, filing status, exemptions, multiple sources of income, adjustments, tax calculations, and payment guidelines, ensuring comprehensive analysis for accurate tax assessments.

How to Use the 2003 Tax Form

Form 1040 is a detailed document comprising various sections to report annual income and adjustments. Begin with personal information such as name, social security number, and address. Proceed to declare your filing status and exemptions, which influence tax obligations. The form's next sections require reporting of different income types, including wages, dividends, and business income. Adjustments to income, such as IRA contributions and student loan interest deductions, come next, followed by tax computation details. Final sections handle refunds or payments due. Diligence in each section guarantees an accurate representation of financial activities over the tax year.

Steps to Complete the 2003 Tax Form

-

Collect Personal Information

- Ensure accuracy in name, address, and social security numbers.

-

Determine Filing Status

- Select the appropriate status, such as single, married filing jointly, or head of household.

-

List Exemptions

- Record the number of dependents and corresponding details.

-

Report Income

- Include wages, dividends, and any other income sources.

-

Adjust Income

- Enter eligible deductions like student loan interest and tuition fees.

-

Calculate Tax

- Use tax tables or software to compute obligations.

-

Finalize with Refunds or Payments

- Determine if you're owed a refund or need to make a payment.

Important Terms Related to the 2003 Tax Form

- Adjusted Gross Income (AGI): Total gross income minus specific deductions; a key figure for determining tax liability.

- Exemptions: Deductions allowed for the taxpayer and dependents, reducing taxable income.

- Tax Credit: Reductions to tax obligations, allowing a dollar-for-dollar decrease in owed taxes.

Key Elements and Sections of the Form 1040

Form 1040 is structured into specific parts that include:

- Personal Information: Captures the taxpayer's fundamental identity details.

- Filing Status and Exemptions: Determines tax rates and credits applicable.

- Income Reporting: Covers wide income categories, ensuring all earnings are declared.

- Tax Computation and Credits: Includes tax calculations and applicable credits.

- Payments and Refunds: Deals with tax payments and instructions for claiming refunds.

Who Should Use the 2003 Tax Form

Typically, any U.S. individual with a taxable income for 2003 should use Form 1040. Whether employed, self-employed, retired, or running a business, this form suits various taxpayer categories. Individuals with complex financial situations, like multiple income sources, detailed deductions, and credits, will benefit from this comprehensive form. Conversely, simpler versions like Form 1040-EZ exist for simpler tax conditions.

Filing Deadlines and Important Dates

The standard deadline for submitting the 2003 Form 1040 was April 15, 2004. Filing extensions, if approved, allowed filers additional time without penalties for late submission. It's crucial for taxpayers to meet this deadline to avoid interest and potential fines. Timely submissions also ensure smooth processing and prompt refund disbursements.

Required Documents to Accompany the 2003 Tax Form

Prepare by gathering:

- W-2 Forms: For employment income verification.

- 1099 Forms: For supplementary income details.

- Receipts and Records: Document expenses eligible for deductions, such as medical expenses or education costs.

- Previous Year's Tax Returns: Helpful for consistency and reference.

Penalties for Non-Compliance

Failure to file or incorrect submission of the 2003 Form 1040 can incur several penalties, including:

- Failure-to-File Penalty: A charge assessed on late submissions.

- Failure-to-Pay Penalty: Applied when taxes are not paid by the due date.

- Interest Penalties: Calculated on unpaid taxes from the original deadline until cleared.

Staying informed and compliant minimizes risks of financial penalties and encourages good fiscal practice.