Definition & Meaning

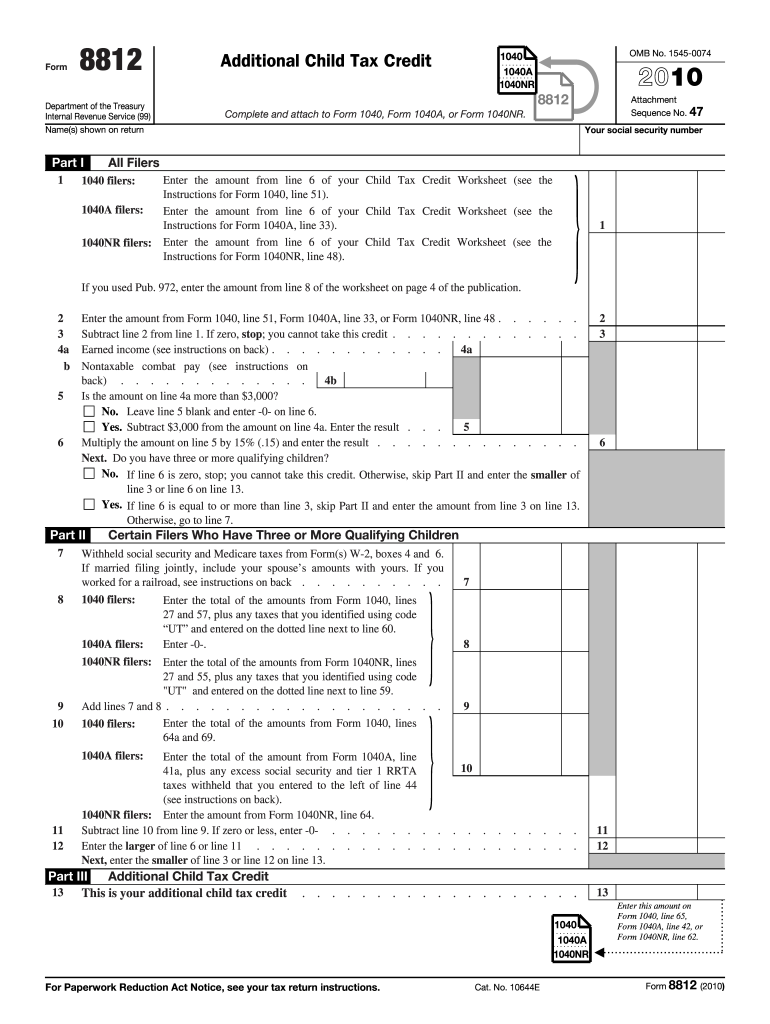

Form 8812, also known as the Additional Child Tax Credit form, is a vital document used to calculate the refundable portion of the Child Tax Credit. For eligible filers, this form may provide a refund even if no federal income tax is owed. The 2010 version of Form 8812 serves the same purpose, ensuring that taxpayers with qualifying children can maximize their potential refund based on specific eligibility criteria such as income thresholds and family size.

Key Features of the 2010 Form 8812

- Refundability: Unlike the standard Child Tax Credit, the Additional Child Tax Credit is refundable, meaning you can receive a refund if the credit exceeds your tax liability.

- Eligibility Criteria: The form includes sections to determine eligibility based on factors like earned income and family size.

- Worksheet Inclusion: The form provides a detailed worksheet to guide taxpayers in calculating the exact amount of the credit they qualify for.

How to Use the 2010 Form 8812

Using the 2010 Form 8812 involves several key steps to ensure accuracy in calculating potential refunds.

Step-by-Step Instructions

- Review Eligibility: Begin by confirming that you and your children meet the eligibility criteria, such as age and dependent status.

- Complete the Child Tax Credit Worksheet: This section requires information regarding your income and number of qualifying children.

- Calculate the Credit: Based on the worksheet, fill in the required sections to determine your Additional Child Tax Credit.

- Include on Tax Return: The completed form needs to be attached to your main tax return, typically Form 1040, to claim the credit.

Steps to Complete the 2010 Form 8812

Completing the 2010 Form 8812 accurately requires careful attention to detail and adherence to guidelines.

- Personal Information: Begin with entering your personal information accurately, including your name and Social Security number.

- Children's Information: List all qualifying children along with their Social Security numbers and relationship to you.

- Income Details: Provide details about your income, especially any earned income, which is crucial for calculating the credit.

- Calculate Credit Amount: Follow the step-by-step guidance on the form to compute the potential Additional Child Tax Credit amount you are eligible for.

- Transfer Amounts: Once completed, ensure the calculated credit amount is transferred correctly to your overall tax return.

Important Terms Related to 2010 Form 8812

Understanding specific terms related to Form 8812 can help taxpayers accurately fill out the form.

Glossary of Terms

- Child Tax Credit: A nonrefundable federal tax credit for parents with qualifying children, reducing tax liability.

- Additional Child Tax Credit: The refundable portion of the Child Tax Credit which can result in a tax refund.

- Earned Income: Income received from working, crucial for determining credit eligibility and amount.

- Qualifying Child: Typically, a dependent under 17 years of age during the tax year.

Eligibility Criteria

Eligibility for the 2010 Form 8812 is contingent on meeting several conditions which impact the potential for receiving a refund.

Core Eligibility Requirements

- Age of Child: The child must be under 17 years of age at the end of the tax year.

- Relationship: The child must be your dependent, typically your biological child, stepchild, or eligible foster child.

- Residency: The child must have lived with you for over half of the tax year.

- Income Thresholds: Your income must align with the specified thresholds detailed in the form's instructions.

Who Typically Uses the 2010 Form 8812

Form 8812 is primarily utilized by parents and guardians who qualify for the Additional Child Tax Credit.

Typical Users Include

- Families with Children: Especially those with multiple dependents under the age of 17.

- Low-to-Moderate Income Households: As the credit can provide substantial refunds even with minimal tax liabilities.

- Taxpayers with Earned Income: Individuals whose earned income aligns with the form's eligibility criteria benefit the most.

Filing Deadlines / Important Dates

Adhering to filing deadlines for the 2010 Form 8812 is critical to ensure timely processing of your tax refund.

Key Deadlines

- Tax Day: Typically April 15th of the following year. However, adjustments may occur if the date falls on a weekend or holiday.

- Filing Extensions: Extensions can be filed, providing additional time if necessary, but must be submitted by the original deadline.

- Amended Returns: If an error is discovered post-filing, an amended return using Form 1040X must be submitted promptly.

Examples of Using the 2010 Form 8812

Practical scenarios can illuminate the benefits and applications of Form 8812.

Example 1: Family with Two Children

- Scenario: A family with two children under 17, with the primary earner receiving a modest salary.

- Outcome: By completing the Form 8812 accurately, they can receive refunds that substantially aid their financial situation.

Example 2: Low-Income Household

- Scenario: A single parent with limited income due to part-time work.

- Outcome: The refundable nature of the Additional Child Tax Credit ensures that the parent receives a refund despite low tax liabilities.

By following these guidelines and descriptions, users can effectively navigate the 2010 Form 8812, maximizing their potential refunds and ensuring compliance with IRS regulations.